| Close | Previous Close | Change | |

|---|---|---|---|

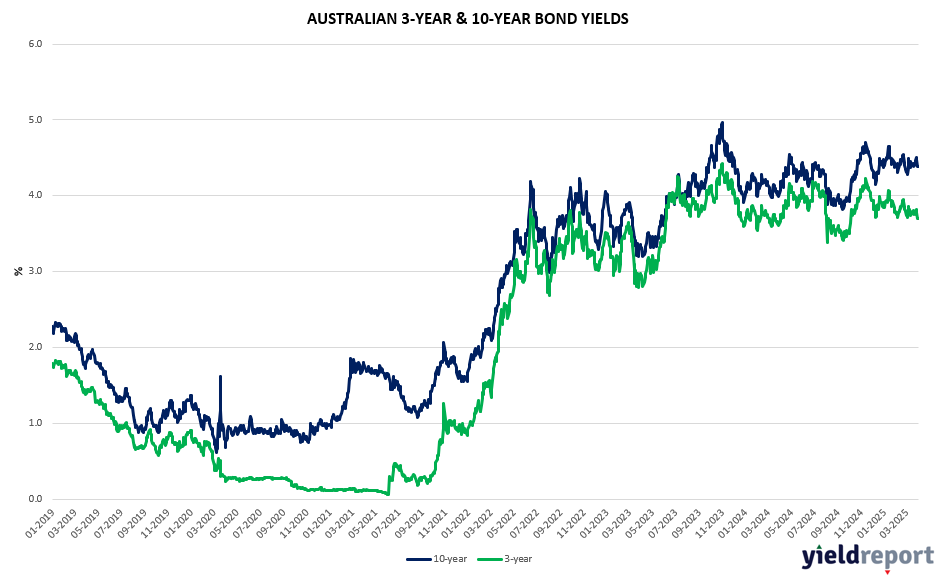

| Australian 3-year bond (%) | 3.567 | 3.729 | -0.162 |

| Australian 10-year bond (%) | 4.235 | 4.384 | -0.149 |

| Australian 30-year bond (%) | 4.831 | 4.94 | -0.109 |

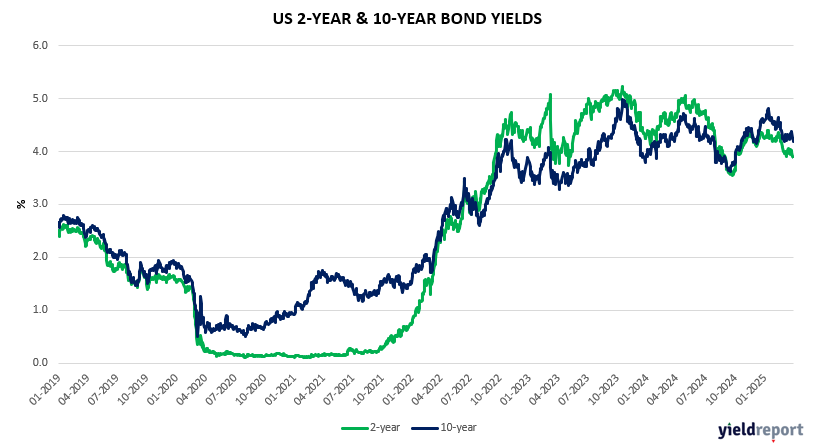

| United States 2-year bond (%) | 3.725 | 3.904 | -0.179 |

| United States 10-year bond (%) | 4.055 | 4.195 | -0.14 |

| United States 30-year bond (%) | 4.484 | 4.551 | -0.067 |

LOCAL BOND MARKETS

Australia’s 10-year government bond yield fell 13 bps to around 4.27%, its lowest level in a month, as investors sought safe-haven assets after U.S. President Donald Trump unveiled massive increases in tariffs, deepening a global trade war that could hurt economic growth.

The broad expectation amongst economists, and indeed the market, is the Trump announcement will lead to a more dovish monetary policy stance in the near term from the RBA. The RBA could be more concerned about the indirect impacts to confidence, particularly ongoing uncertainty that affects global business investment and funding flows. The transmission channel for the RBA would be through potentially tighter financial conditions and less domestic business investment on the part of firms. The RBA would also potentially be on the lookout for lower household spending and higher precautionary savings.

Indeed, Traders have turbocharged bets for an interest rate cut next month on worries about a global economic recession. Money markets are fully priced for the Reserve Bank to reduce policy by a quarter of a point in May, taking the cash rate to 3.85 per cent. They had ascribed a chance of about 70 per cent before the announcement. Traders now expect a total of 90 basis points of easing over the next 12 months, equivalent to between three and four rate reductions. They had previously anticipated between two and three rate cuts. The market is pricing a global recession risk.

By sheer coincidence, the RBA released its Financial Stability Review yesterday. While the document was written prior to the tariff release, the RBA warns that US trade policies and nations’ responses could have a “chilling effect” on global business investment and household spending. But here’s the point – the actual tariff levels were higher than expected by the market and particularly hard on important Australian Asian export markets.

Economic data wise, fresh data showed Australian industrial activity contracted further in March, weighed down by uncertainties surrounding US tariffs and domestic politics.

US BOND MARKETS

In short, bond markets were the big winner, but the reactions show that growth concerns trumped (excuse the pun) any inflationary concerns. That is, the reaction is one of recession risk rather than stagflation risk. Still, US inflation risks arising from tariffs have led Morgan Stanley’s economists to push back their call for the next Fed rate cut from June to early 2026. They see a terminal rate of 2.50% to 2.75%.

The yield on benchmark Treasuries fell briefly below 4% for the first time since October as Wall Street fretted that the US economy will end up worse off from President Donald Trump’s trade war. Ten-year yields declined as much as 13 basis points on Thursday to dip below 4%, the lowest level since before Trump was elected last year. Meanwhile, money markets priced in a 50% chance of the Fed delivering four quarter-point rate reductions this year, a scenario that wasn’t even contemplated on Wednesday.

Similarly, the concerns on economic growth drove a fierce rally in global bond markets, with yields on European and UK bonds also plunging. Similarly, traders ramped up wagers on monetary easing from the European Central Bank and the Bank of England, increasing the chances that both deliver three more cuts.

On the economic front, the Institute for Supply Management index showed that US service providers expanded in March at the slowest pace in nine months. Additionally, services employment sank by 7.7 points, the most in nearly five years, to 46.2, with the decline attributed to reductions related to reduced business rather than layoffs.

On Friday, there will be 2 things the market will focus on. There will be a speech on the economic outlook by Federal Reserve chairman Jerome Powell and the US March payroll data will be released at 11.30pm on Friday.