| Close | Previous Close | Change | |

|---|---|---|---|

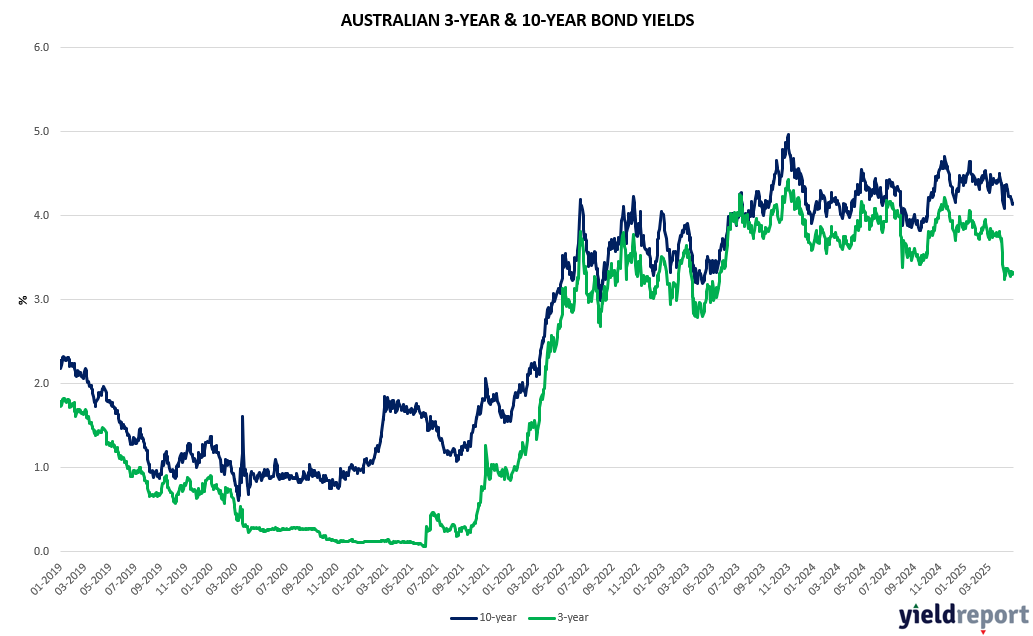

| Australian 3-year bond (%) | 3.335 | 3.324 | 0.011 |

| Australian 10-year bond (%) | 4.131 | 4.148 | -0.017 |

| Australian 30-year bond (%) | 4.827 | 4.875 | -0.048 |

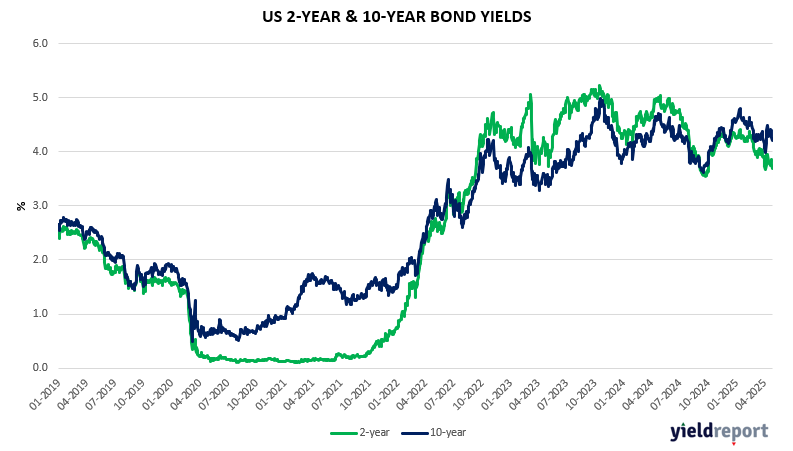

| United States 2-year bond (%) | 3.621 | 3.658 | -0.037 |

| United States 10-year bond (%) | 4.174 | 4.216 | -0.042 |

| United States 30-year bond (%) | 4.648 | 4.693 | -0.045 |

LOCAL BOND MARKETS

Headline and trimmed mean core inflation are both finally back inside the RBA’s target band of 2-3%, albeit at the very upper end. Core inflation, the RBA’s more closely watched underlying measure of inflation, rose 0.7% for the quarter, 2.9% annualised. Headline inflation rose 0.9% for the quarter, 2.4% annualised.

Core inflation was broadly in line with RBA forecasts, but slightly above the expectation of market economists for underlying inflation of 0.6% for the quarter and 2.8% in annual terms. Headline CPI was expected to come in at 2.3%. So let’s just call it in-line. In response, Australia’s 10-year government bond yield held steady at 4.15%.

The market is 100% priced in for a May 20 25 bps cut and 56% probability of a jumbo 56 bps cut. Economists are also all in for May, but very few expect a jumbo cut. Economists, being more circumspect, state it is exceptionally likely but not a certainty.

Meanwhile, for the remainder of 2025, the market is price in a tad over four 25 bps cuts to 3.0% by year end and a terminal rate of 2.85 in 12-months by May 2026 – five 25 bps cuts. For economists, a May rate cut followed by two or three more this year is forming as the consensus view.

As noted in the AFR, “State Street Global Markets’ head of APAC macro strategy Dwyfor Evans, whose firm runs its own price monitoring data, says Australia hasn’t toppled its inflation issue, thinks the RBA has been deliberately noncommittal about cutting rates and think markets will have to wind back its pricing – that is, this spate of rate cuts isn’t coming in the forseeable future. “The disinflation story, it is not really there,” Evans says.” We couldn’t agree more.

A 2.85% can only justifiably be posited on an economic shock and which can only perceivably come from a persistence of Trump tariffs at circa current levels. And currently Trump is trying to reverse as quick as possible without losing face. But if we get an economic shock, then equities are looking risk and bond yields at current levels an attractive entry point.

US BOND MARKETS

The yield on the 10-year US Treasury note hovered around 4.16% on Wednesday, the lowest in three weeks, after rising earlier in the session, as pessimistic economic data drove wagers of Fed rate cuts to offset gauges of rising term premiums on Treasuries.

It was a big day on the macro and sentiment survey front, with the release of Q1 GDP, consumer spending for March and the Fed’s preferred inflation measure, core PCE for both Q1 and the month of March.

The US economy contracted in Q1 for the first time since 2022 on a monumental pre-tariffs import surge and more moderate consumer spending, a first snapshot of the ripple effects from President Donald Trump’s trade policy. GDP decreased an annualized 0.3% Q1, well below average growth of about 3% in the prior two years. The data highlight the scramble by companies to secure merchandise ahead of expansive tariffs, with net exports subtracting nearly 5 percentage points from GDP, the most on record. A decline in federal spending also weighed on the figure. The GDP result, or at least the direction, was not unexpected – it has been well noted that businesses and consumers (auto sales, etc) were front running the tariffs. However, looking further out, forecasters contend that the higher duties will cause a supply shock, challenging businesses and leading to a pullback in demand.

Meanwhile, consumer spending climbed 0.7% last month. That was the most since the start of 2023 and suggested households spent aggressively to get ahead of new tariffs.

Meanwhile Federal Reserve’s preferred, core PCE inflation, was released for Q1 and the month of March. The gauge showed core PCE inflation was up for Q1 but was flat for the month of March YoY. The former, at 3.5%, accelerated month than expected. However, the latter means we had no inflation YoY. However, April will be a different situation. We note reports of some very large price increases now being reported towards the latter part of April.

Tomorrow on Thursday, we get the ISM manufacturing report and while that is considered soft data, it could be very important to the markets because if the report shows the same kind of nationwide response that has been reported in some of the regional numbers, it will show a large drop in manufacturing activity, new orders, etc. And that is not going to play well with Wall Street.

The monthly jobs report is due Friday and is projected to show some cooling is underway. A report out Wednesday showed employment at private companies rose a disappointing 62,000 in April, the smallest gain since July.