| Close | Previous Close | Change | |

|---|---|---|---|

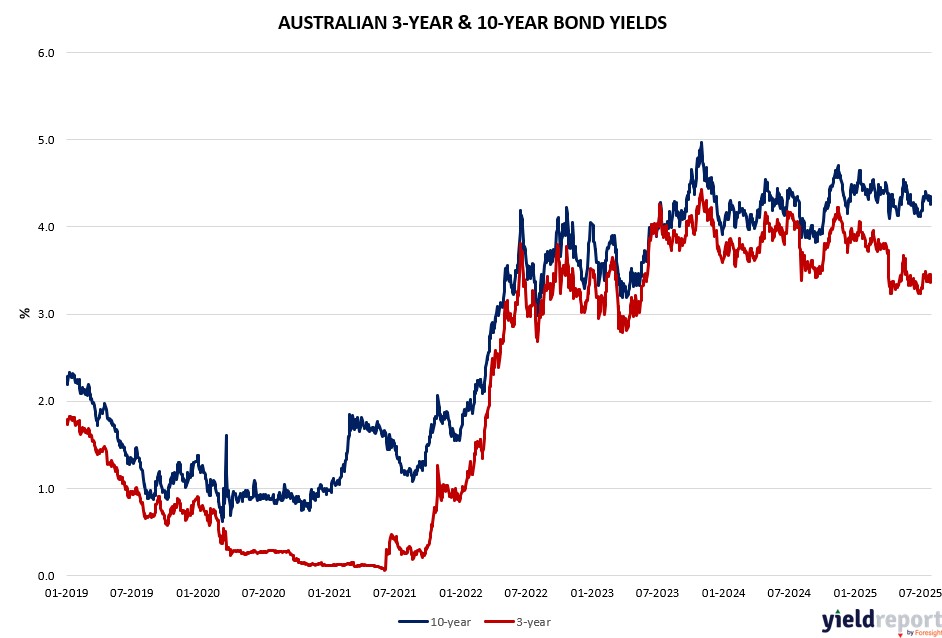

| Australian 3-year bond (%) | 3.392 | 3.362 | 0.03 |

| Australian 10-year bond (%) | 4.274 | 4.262 | 0.012 |

| Australian 30-year bond (%) | 4.972 | 4.975 | -0.003 |

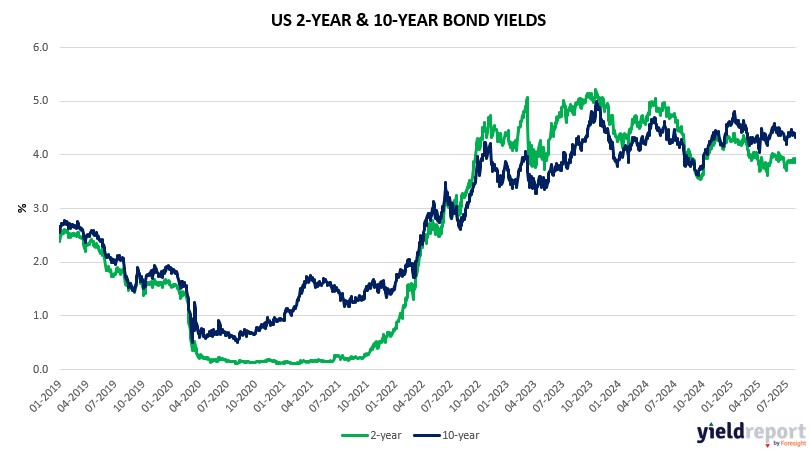

| United States 2-year bond (%) | 3.932 | 3.867 | 0.065 |

| United States 10-year bond (%) | 4.358 | 4.322 | 0.036 |

| United States 30-year bond (%) | 4.8847 | 4.8624 | 0.0223 |

Overview of the Australian Bond Market

Australian government bond yields edged higher on July 31, 2025, as robust economic data tempered expectations for immediate RBA rate cuts. The Australia 2-Year Bond Yield rose 7 basis points to 3.39%, the 5-Year Yield increased 6 basis points to 3.71%, and the 10-Year Yield climbed 5 basis points to 4.30%. The 15-Year Yield saw a modest 4 basis-point rise to 4.66%.

The uptick in yields followed stronger-than-expected Australian economic indicators, including June Building Approvals surging 11.9% (vs. 2% forecast) and Retail Sales rising 1.2% month-on-month (vs. 0.4% expected). These figures suggested economic strength, reducing the urgency for aggressive RBA easing despite Wednesday’s benign inflation data (Q2 CPI at 2.1%). Markets still price in a high likelihood of an August rate cut, but swap contracts now reflect a more gradual easing path, with some analysts revising expectations to three cuts by mid-2026.

Global macro dynamics also influenced bond markets. The US Federal Reserve’s decision to hold rates at 4.375% and stronger US GDP growth (3% vs. 2.4% expected) underscored global economic resilience, supporting a bearish tilt in bond prices. Ongoing US-China trade talks and Trump’s tariff threats against India and Russia added inflationary risks, capping bond demand. Locally, bond traders increased net long positions in 10-year and 15-year tenors, anticipating yields may stabilize if RBA policy remains data-dependent.

The Australian Treasury is expected to maintain steady auction sizes for the August-to-October period, aligning with prior guidance. Investors are closely watching the RBA’s August meeting for signals on the pace of monetary easing, with strategists from HSBC and UBS noting that Australia’s economic resilience could keep yields elevated in the near term.

Overview of the US Bond Market

The yield on 10-year Treasuries was little changed at 4.36%. The dollar rose for a sixth straight day. The yen slid as comments from Bank of Japan Governor Kazuo Ueda were seen as less hawkish than expected.

In the run-up to jobs data, the Fed’s preferred measure of underlying inflation accelerated in June to one of the fastest paces this year while consumer spending barely rose, underscoring the dueling forces dividing policymakers over the path of rates.

The core personal consumption expenditures price index rose 0.3% from May. It advanced 2.8% on an annual basis, a pickup from June 2024 that underscores limited progress on taming inflation in the past year. The data also showed inflation-adjusted consumer spending edged up last month.

Separate data Thursday showed initial applications for unemployment insurance were little changed last week. Another report showed labor cost growth rose 3.6% from a year ago, matching the lowest since 2021, reassuring Fed officials that the job market isn’t a source of inflationary pressure.

President Donald Trump will sign an executive order on Thursday imposing new tariff rates on trading partners that take effect Friday, the White House said.

The signing will take place “at some point this afternoon or later this evening,” White House Press Secretary Karoline Leavitt told reporters during a news briefing, adding that “Aug. 1, the reciprocal rates will be going into effect.”

Trump has struck deals with major trading partners, such as the European Union, the UK, Japan and South Korea, and unilaterally set rates on others, including India and Brazil. The president initially announced tariffs on almost every country in April, but paused them twice to allow more time for negotiations.

The president earlier Thursday continued Mexico’s current tariff rates for another 90 days to allow more time for trade negotiations, even after saying a day earlier that the Aug. 1 deadline “WILL NOT BE EXTENDED.” Levies on Mexican exports were due to rise from 25% to 30% starting Friday.