| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.618 | 3.578 | 0.04 |

| Australian 10-year bond (%) | 4.308 | 4.235 | 0.073 |

| Australian 30-year bond (%) | 4.94 | 4.893 | 0.047 |

| United States 2-year bond (%) | 3.604 | 3.504 | 0.1 |

| United States 10-year bond (%) | 4.085 | 3.989 | 0.096 |

| United States 30-year bond (%) | 4.6367 | 4.5512 | 0.0855 |

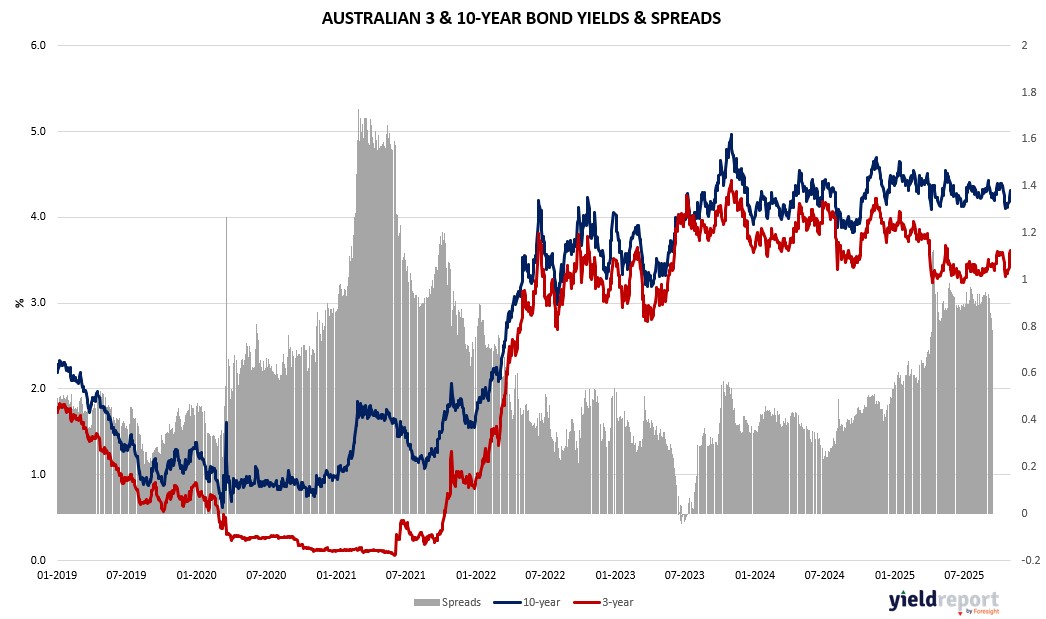

Overview of the Australian Bond Market

Australian government bond yields edged lower as markets digested hot inflation prints and a hawkish global tone, with limited data flows amid US shutdown parallels. The 10-year yield dipped 1 basis point to 4.29%, the 2-year fell 2 to 3.55%, and the 15-year held at 4.60%. The curve showed minimal shift, reflecting steady policy bets.

Third-quarter CPI exceeded polls at 1.3% quarterly and 3.2% annually, trimmed mean at 3.0% yearly, pushing back easing and aligning with Fed hawks like Logan seeing neutral rates. China’s APEC 2026 in Shenzhen highlights tech prowess, potentially stabilizing trade post-truce, but gold tax scrap may strain revenues if growth lags, capping yield downside.

The Aussie dollar dipped below its 100-day average, pressured by yuan and copper ahead of PPI. Bond positioning anticipates caution, with inflation resilience and AI integration in non-resources echoing US trends, strengthening higher-for-longer if fundamentals hold amid tariff clarity.

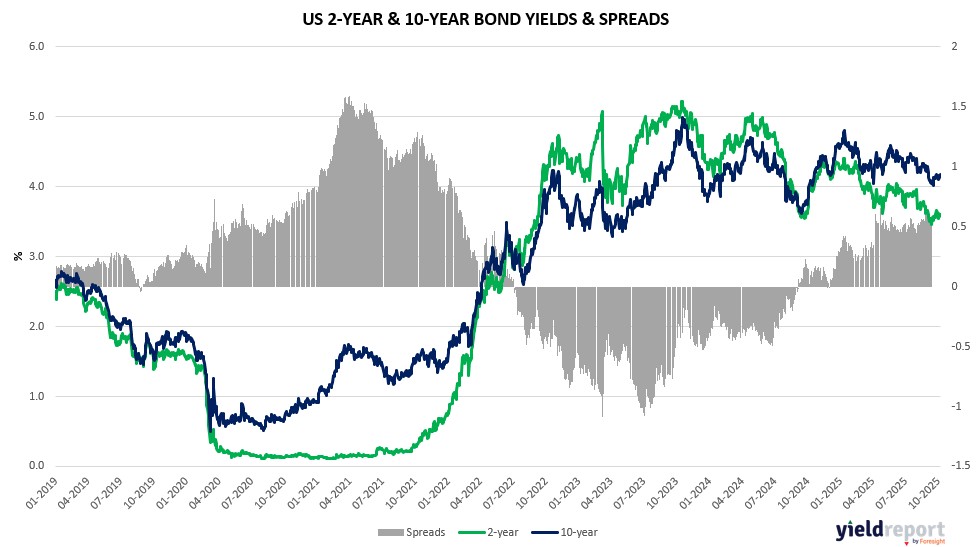

Overview of the US Bond Market

Bond traders steadied positions after a post-Fed rout, with Treasury yields little changed as markets weighed hawkish dissents and resilient data against labor risks. The 10-year yield held at 4.09%, the 2-year dipped 1 basis point to 3.60%, and the 30-year rose 1 to 4.67%, steepening the 2s-10s curve to +49.1 basis points. The dollar’s third straight gain hit a three-month high, pressuring EUR/USD to a similar low.

The calm followed Powell’s signal that December easing is no sure thing, amid internal divides where hawks like Logan see policy near neutral and inflation risks from services prices, while Waller prioritizes labor softening. Treasury Secretary Scott Bessent’s critique of China’s rare earth threats, in a truce easing global uncertainties, may cap upside for yields if supply chains stabilize. Third-quarter GDP approached 4%, per White House adviser Kevin Hassett, signaling momentum that bolsters higher-for-longer views, though shutdown fog limits visibility, with Logan relying on private surveys showing stable jobs.

September PCE inflation met expectations at 0.3% monthly and 2.8% yearly, core at 0.2% monthly and 2.9% yearly, reinforcing gradual progress toward 2%. Durable goods rose 0.2%, missing polls, while consumer confidence beat at 94.6. Industrial production and housing starts aligned with forecasts, new home sales topped estimates, but shutdown delays like nonfarm payrolls elevate alternative data.

JPMorgan’s client survey likely showed trimmed longs amid vol decline, with swaps pricing under half a point of easing by year-end. Asset managers pared net longs in futures per recent CFTC, concentrated in shorter tenors, as leveraged funds reduced shorts in longs. Dealers anticipate steady auction sizes for November-January, with 5- and 10-year up $1 billion, supporting issuance amid AI-driven growth but potential tariff bites if deals falter.