| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.344 | 3.325 | 0.019 |

| Australian 10-year bond (%) | 4.261 | 4.271 | -0.01 |

| Australian 30-year bond (%) | 4.98 | 4.98 | 0 |

| United States 2-year bond (%) | 3.877 | 3.957 | -0.08 |

| United States 10-year bond (%) | 4.365 | 4.46 | -0.095 |

| United States 30-year bond (%) | 4.888 | 4.983 | -0.095 |

Overview of the Australian Bond Market

Australia’s 10-year government bond yield declined circa 6 bps 4.26%, as investors digested the latest meeting minutes from the RBA. The minutes revealed that the RBA had considered an outsized 50 bps cut as insurance against slowing global growth, particularly amid rising trade policy uncertainty. However, the board ultimately opted for a smaller, more measured 25 bps cut to 3.85%, citing continued resilience in the domestic economy, a tight labor market, and the limited impact of US trade policies on Australia so far. Still, policymakers noted that if downside risks materialize, rates could fall below the neutral level of around 3%. Markets currently price in a 70% chance of another rate cut in July. GDP data is out later this week – backward looking and pre-tariffs as it is.

On RBA speak, according to RBA Assistant Governor Sarah Hunter it expects global trade uncertainty will weigh on the domestic economy and employment, helping explain policymakers’ surprise switch to a dovish stance last month. “The baseline forecast is for recent global developments to contribute to slower economic growth in Australia and a slightly weaker labor market,”. Sarah Hunter added that the RBA expects the price of tradable goods will be “slightly dampened” too. The comments underscore the RBA’s shift in focus to downside risks to growth from the Trump administration’s tariff regime after it wrapped up a three-year campaign to rein in inflation. Money markets are now pricing in three more RBA cuts this year.

Bonds in Australia are getting a lift as questions about the appeal of US Treasuries send investors toward top-rated alternatives. Strategists and portfolio managers are re-examining whether Treasuries offer enough compensation, a rare challenge to the world’s largest bond market after a recent ratings downgrade and fears that a proposed tax bill may hit foreign investors. And that is just the fiscal risk.

Taiwanese insurers recently got crushed on FX moves. They are making plans to back away from dollar assets, while Hong Kong pension funds have been told to draw up contingency plans for a further downgrade of the US. One large Taiwanese insurer has already begun building a small position in top-rated Australian and UK corporate bonds to diversify from US dollar-denominated assets. And that is just a sliver of what Asia is thinking of when it comes to somewhat stepping away from US assets – they are heavily exposed.

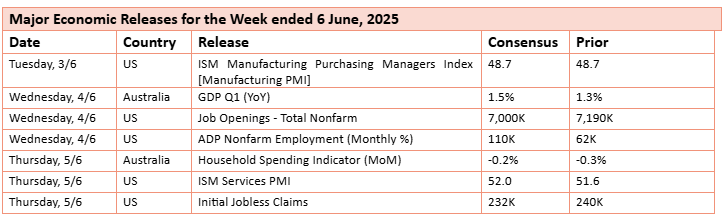

All of the recent ructions in the US are adding to the appeal of the world’s dwindling supply of AAA rated bonds. The spread between Australian 30-year bonds and equivalent US Treasuries is around its narrowest level in a year, a sign that investors are putting more of their money into the Australian debt. The gap between the same maturity bonds from Singapore and the US is near a record discount. And, by the way, should we add the trajectory of easing – it will be well ahead in Australia vs. the US. In Figure 1 below this is evident by the spread moving into the positive. In Figure 2, evident in the negative.

The technicals in Australian bonds were robust already, and leading to tight spreads. Foreign investors in Australia’s government bond market are set to face competition from local pension funds, whose demand for Aussie notes may outpace issuance. Only Singapore offers a comparable option in the SE Asian market. This is a bigger topic we have been noting – how the private markets are leading to shrinkage in the public markets and how (passive) ETF and Super flows are compressing valuations in bonds and equities alike. On that basis taken in isolation, tight spreads are likely to persist.

Overview of the US Bond Market

The yield on the US 10-year Treasury note hovered around 4.46% on Tuesday, as investors weighed the global and domestic economic outlook and awaited further developments on the trade front. The 30-year was largely unchanged but moved below 5.0%, only just to 4.99%. The OECD downgraded its global growth forecast for the second time this year, citing rising trade barriers, tighter financial conditions, weakening business confidence, and heightened policy uncertainty. On trade, President Trump and President Xi are expected to hold talks later this week amid intensifying US-China tensions.

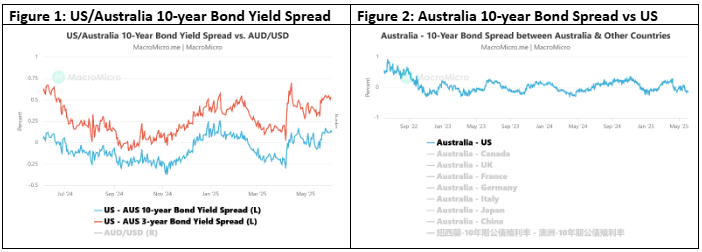

In terms of data, the JOLTS report showed a surprise increase in job openings for April, indicating continued strength in labour demand. US job openings rose in April to 7.39 million, driven by private-sector industries such as professional and business services and health care and social assistance. The advance in openings was accompanied by a pickup in hiring, which reached the highest level in nearly a year, despite a decline in openings in manufacturing and the leisure and hospitality sector. However, factory orders declined slightly more than expected. The JOLTS report tracks nonfarm job openings, voluntary quits, hiring, and layoffs. It is a key indicator often used by former Federal Reserve Chair Janet Yellen to assess the state of the U.S. job market.

In relation to Figure 2 below, the Jobs-Workers Gap (JWG) is calculated with the following formula:

(Household Survey Employment + JOLTS Job Openings – Household Survey Labor Force Participation) / Household Survey Labor Force Participation. Household Survey Employment and JOLTS Job Openings represent labour demand, while Household Survey Labor Force Participation represents labour supply. A high JWG ratio suggests strong demand in the labour market and a shortage of supply. While a lower JWG ratio indicates weak demand and oversupply in the labour market.

Meanwhile, Atlanta Fed President reiterated a cautious stance on interest rates, stating he’s in no rush to cut and wants to see “a lot” more progress on inflation. The Fed is expected to keep the fed funds rate steady once again this month. The rise in job openings helped reinforce the Federal Reserve’s assertion that the labour market is in a good place. While some economists fear a more notable weakening in coming months under the weight of tariffs, that hasn’t shown up in the data yet, supporting officials’ posture to keep rates steady.

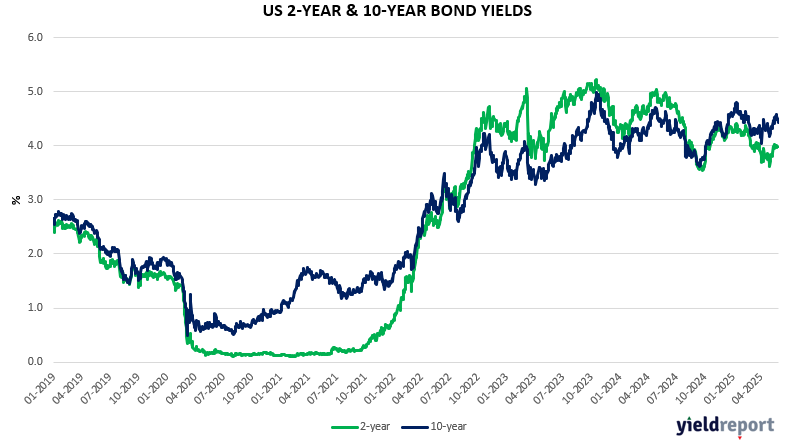

As we noted yesterday, investment firms are avoiding or shorting 30-year US Treasuries due to concerns about America’s growing federal budget gap and debt burden. Wary of America’s swelling federal budget gap and growing debt burden investment firms are steering away from the longest-dated US government bonds in favour of shorter maturities that carry less interest-rate risk but still offer a decent yield.

The US 30-year bond has been a stark underperformer in 2025. Yields on the maturity have risen, while those on 2-, 5- and 10-year notes have fallen. This sort of divergence is rare — the last time it happened over a full year was in 2001 — underscoring the pressure on the long bond as investors demand added compensation to lend to the US government for such a long period. So bad has been the rout that speculation has even begun to swirl that the Treasury might scale back or halt auctions of its longest tenor.

If you can outright short it, you go in the steepener, the bet that anticipates that long-dated rates will rise relative to those on shorter maturities. But in other strategies where it’s purely long only, you just basically doing a buyers’ strike and move to invest more in that middle part of the curve. The Fed won’t be happy with this, but it forces them to issue at the intermediate term. Now, that’s the insto market. But, . . . .

Want to be the one to stand in front of the steamroller?? Well, Retail Investors keep Piling in to US Long-end Treasuries ETFs to take that Yield & Convexity. The iShares 20+ Year Treasury Bond ETF (TLT) is one of the most popular options for investors seeking to establish exposure to long-dated Treasuries, an asset class that is light on credit risk but may offer attractive yields thanks to an extended duration and therefore material interest rate risk. For those looking to extend the duration of their portfolio and potentially enhance the current return offered, TLT can be a useful product.

The retail trade has been clashing with the institutional trade pretty much all of 2025 and particularly since early April. While insto investors have shunned the US treasuries long-end, TLT has taken in billions of dollars over the past couple of weeks. And for some this has been a widow maker trade. It feels like yields, long end yields in particular have just been on a roller coaster. So how do you explain just this off the charts demand still for long end bonds in particular, and from retail investors?

In short, there seems to be an insatiable demand when long bonds and the 10-year bond hits 5% and retail investors just keep hoovering them up. It’s actually served to limit the 30-year moving meaningly above 5.0%, or at least sustainably so.

But how can you explain this concept of buying TLT, yielding 5%, when you can get almost the same yield in a money market fund or the short end of the curve, specifically circa as high as 4.7%. Why bother with the duration risk? Or is this a bet on the Fed? Yes, it’s the latter. The long-end gives you convexity, the short-end doesn’t. And at some point the Fed will begin cutting rates.

And furthermore, while the Insto market is focusing on the belly of the curve, 3- to 7-year, the retail investors are not. The attitude appears to be ‘if I’m going to take risk, I want to take more risk’. Anyway, so far this year it has been a one-zero scoreline of retail investors (the ‘dumb money’) over institutional investors (the ‘smart money’). We can see the merit in the trade. To our mind, the probability of the 30-year yield being below 5% is higher than being above. You get a higher yield, and you get an extra kicker from the convexity when the Fed inevitably starts cutting again.

But the negative is the fiscal picture and which cautions towards 30-year Treasuries. And on that basis, if there is a bond-market rally, it will likely be led by the 5- to 10-year and less by the long end. Shock, horror, (and the story of last week) auctions last week offered endorsement for this. Sales of 2-, 5- and 7-year notes all saw solid demand. And we know what happened at the long-end – the US and Japan.

Looking Ahead: Major Economic Releases for the Week Ended 6 June

US payrolls on Friday, what is everyone is waiting for. Economists are predicting no change in unemployment. But look at the ISM that came in on Monday. Friday’s report may be the last of the good news. Companies were bitten by Covid in terms of letting go of employees. So, companies are probably holding off. In Australia, the household spending indicator is worth watching.