| Close | Previous Close | Change | |

|---|---|---|---|

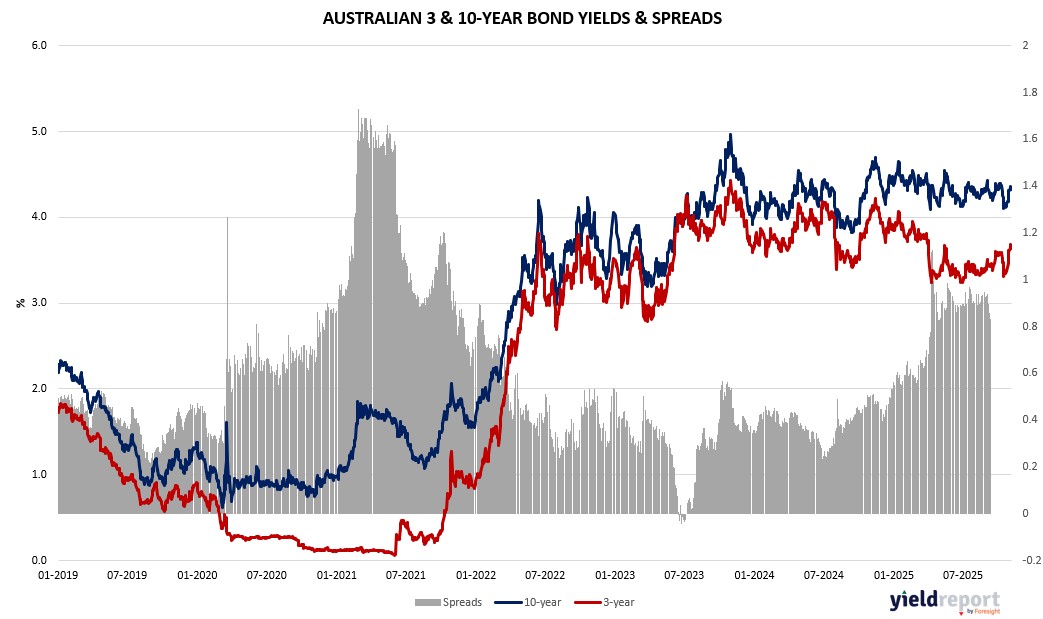

| Australian 3-year bond (%) | 3.631 | 3.678 | -0.047 |

| Australian 10-year bond (%) | 4.322 | 4.358 | -0.036 |

| Australian 30-year bond (%) | 4.967 | 5.006 | -0.039 |

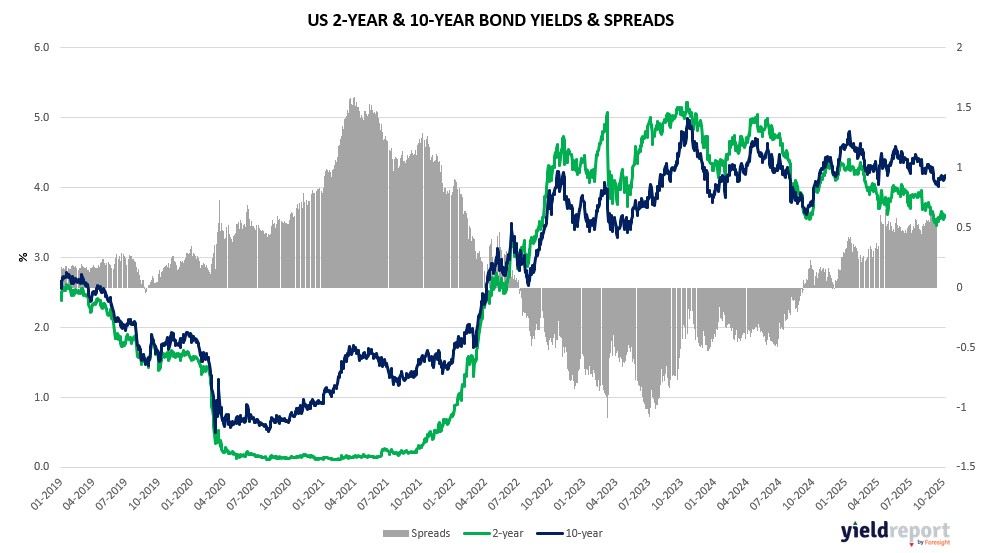

| United States 2-year bond (%) | 3.57 | 3.584 | -0.014 |

| United States 10-year bond (%) | 4.083 | 4.089 | -0.006 |

| United States 30-year bond (%) | 4.6705 | 4.6734 | -0.0029 |

Overview of the Australian Bond Market

Australian government bond yields edged higher on November 5 as global risk rebound and US services strength reduced safe-haven demand, aligning with Treasury climbs amid trade surplus miss and commodity softness pressuring AUD/USD up 0.14% to 0.6499. The 10-year yield rose one basis point to 4.36%, the 2-year dipped two to 3.59%, the 5-year slipped one to 3.82%, and the 15-year added one to 4.67%. The move reflected growth signals but tempered by shutdown’s drag, potentially delaying US cuts and spilling into Aussie policy.

September trade data showed A$1.825 billion surplus versus A$4 billion forecast, with exports plunging 7.8%, highlighting China demand risks ahead of durable goods and retail sales. RBA’s hawkish hold echoes in forecasts, with EY’s Murphy seeing no more cuts possible. Yields may face pressure if tariffs survive Supreme Court scrutiny or AI momentum sustains, but defensive flows and bitcoin slide underscore caution amid geopolitical uncertainties.

Overview of the US Bond Market

Bond traders sold Treasuries on November 5 as robust ISM services data and earnings resilience fueled risk-on moves, pushing yields higher amid Fed rate path reassessment and Treasury’s deficit financing plans signaling preliminary future auction increases despite steady sizes for now. The 10-year yield climbed seven basis points to 4.16%, its highest in a month, the 2-year advanced six to 3.63%, and the 30-year rose seven to 4.74%. The curve steepened slightly, reflecting growth optimism but tempered by shutdown uncertainties, with swaps holding December cut odds at 60%.

Treasury officials anticipate no note or bond size changes for several quarters but flagged potential hikes later, as deficit swells amid tariff fights and shutdown. Supreme Court skepticism on Trump’s IEEPA tariffs could ease importer burdens if ruled unlawful, potentially impacting revenue. On the economic front, S&P Global services PMI finalized at 54.8 and composite at 54.6, underscoring expansion, while upcoming GDP advance on November 6, polled at 3%, and PCE on November 7 could reinforce higher-for-longer if inflation sticks.

JPMorgan’s client survey likely reflected positioning shifts post-pullback, with asset managers trimming longs per recent CFTC as reserves hover at lows pressuring money markets. Dealers expect unchanged coupons for August-October, but AI capex warnings from Apollo’s Zelter and circular financing concerns could strain if bond taps fund investments, bolstering bearish views amid geopolitical risks.