Summary:

Australian interest rate swap yields rose steadily across the curve over the past month, reflecting a broad-based repricing of monetary policy expectations as markets adjust to the prospect of more persistent inflation and a later rate-cutting cycle. Short-end swap rates were unchanged over the week, with the 1-month, 3-month and 6-month tenors flat, though all have drifted higher over the month by 4–11 bps, signaling modest upward pressure in front-end funding costs.

The movement was far more pronounced in medium- and long-dated swaps. The 1-year rate rose 10 bps over the week and 19 bps over the month, while the 3-year and 5-year tenors increased by 20–21 bps over the week and around 30 bps monthly. These shifts reflect greater uncertainty around the RBA’s willingness to ease policy, with markets pushing out expectations for the first rate cut.

Long-term swap rates also climbed noticeably. The 10-year swap rose 20 bps over the week and 27 bps over the month to 4.52%, while the 15-year tenor increased 19 bps weekly and 26 bps monthly. The overall pattern highlights rising term premia and a reassessment of structural inflation risks, driving yields higher across the curve.

Bank Bill Swaps

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 month 3.55 0 0.04 3 months 3.64 0 0.07 6 months 3.88 0 0.11 SWAP RATES

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 year 3.64 0.1 0.19 3 years 3.78 0.2 0.3 5 years 4.16 0.21 0.3 10 years 4.52 0.2 0.27 15 years 4.72 0.19 0.26 - Exhibit 1: Australian 3Y/10Y Bond Yield

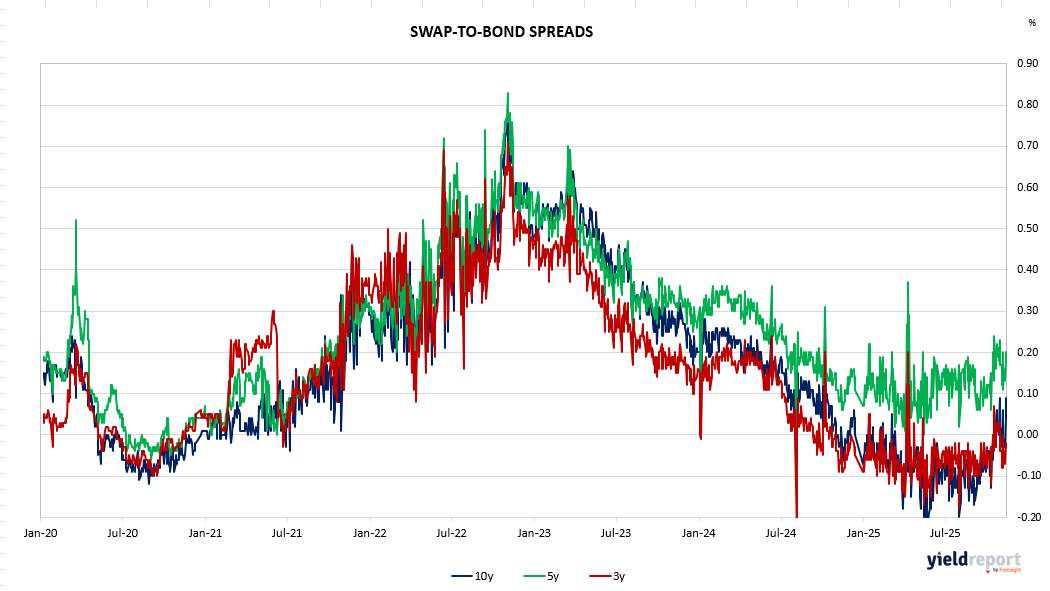

Swap-to-bond spread trends for 3-year, 5-year, and 10-year maturities, January 2020 to November 2025, with detail on periods of volatility and trend toward zero