Summary: BBSW increases; swap rates up at short end, belly but down at long end; swap spreads widen.

Bank bill swap rates increased again this week.

BBSW

| TERM TO MATURITY | CLOSING RATE | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 1 month | 2.93 | 0.05 | 0.17 |

| 3 months | 3.11 | 0.06 | 0.08 |

| 6 months | 3.59 | 0.06 | -0.01 |

Swap rates increased at the short end and the belly but fell for longer-term yields, somewhat following the pattern of their Commonwealth Government counterparts.

SWAP RATES

| TERM TO MATURITY | CLOSING RATE | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 1 year | 3.69 | 0.10 | -0.28 |

| 3 years | 3.81 | 0.11 | -0.5 |

| 5 years | 3.98 | 0.06 | -0.62 |

| 10 years | 4.19 | -0.01 | -0.66 |

| 15 years | 4.28 | -0.05 | -0.64 |

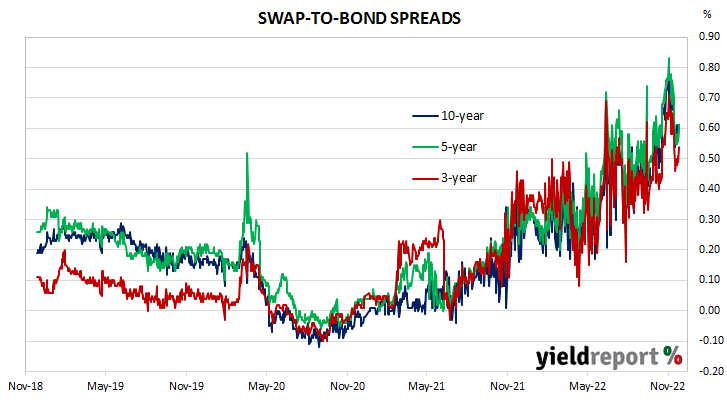

As a result, swap spreads widened moderately. By the end of the week, the 3-year spread had added 5bps to 54bps, the 5-year spread had gained 5bps to 61bps while the 10-year spread finished 3bps higher at 61bps.

NB. Spreads are calculated with respect to “spot” Australian Commonwealth Government bond yields.