Summary: 3-month BBSW down 16bps, 6-month BBSW down 17bps; swap rates fall significantly at front, belly of curve, steady or higher for longer tenors; swap spreads tighten at front of curve, widen elsewhere.

3-month BBSW shed 16bps to 2.88% while 6-month BBSW lost 17bps to 3.38% this week.

BBSW

| TERM TO MATURITY | CLOSING RATE | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 1 month | 2.64 | -0.04 | 0.50 |

| 3 months | 2.88 | -0.16 | 0.39 |

| 6 months | 3.38 | -0.17 | 0.32 |

Swap rates fell significantly at the front and belly of the curve but remained steady or rose for longer tenors, unlike the yields of their Commonwealth Government counterparts which all fell. By the end of the week, the 1-year rate had shed 27bps to 3.59%, the 3-year rate had lost 14bps to 3.86%, the 5-year rate had fallen by 6bps to at 4.15%, the 10-year rate had returned to its starting point at 4.38% while the 15-year rate finished 5bps higher at 4.46%.

SWAP RATES

| TERM TO MATURITY | CLOSING RATE | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 1 year | 3.59 | -0.27 | 0.17 |

| 3 years | 3.86 | -0.14 | 0.25 |

| 5 years | 4.15 | -0.06 | 0.32 |

| 10 years | 4.38 | 0.00 | 0.31 |

| 15 years | 4.46 | 0.05 | 0.31 |

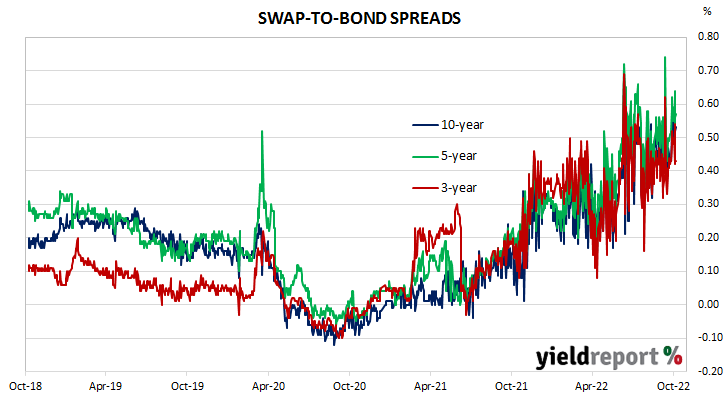

As a result, swap spreads tightened at the front of the curve but increased modestly elsewhere. By the end of the week, the 3-year spread had lost 5bps to 43bps, the 5-year spread had gained 2bps to 57bps while the 10-year spread finished 4bps higher at 53bps.

NB. Spreads are calculated with respect to “spot” Australian Commonwealth Government bond yields.