Summary:

The Bank Bill Swap Rate (BBSW) market moves reflected the RBA’s decision to cut the cash rate by 0.25% to 3.6% on the back of an improving inflation picture and weakening GDP growth prospects.

For the week ending 15th August 2025, the 1-month BBSW held at 3.56% (down 7 bps), while the 3-month BBSW closed at 3.61% (down 8bps), based on daily data trends. The 6-month BBSW dropped 10 basis points to 3.72%, reflecting an easing short-end yield curve amid an RBA rate cut by 0.25% and possibly a further accommodative RBA stance in the coming months.

The longer end of the swap rate curve steepened during the week, with the 1-year swap rate down 5 basis points to 3.29%. The 3-year swap rate dropped 4 basis points to end the week at 3.26%. The 5-year swap rate dropped 4 basis points to 3.66%, reflecting investor expectations of a revised cash rate path for Australia following the RBA’s highly anticipated rate cut amid slowing domestic growth and uncertainties around US tariffs.

Bank Bill Swap Rates

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 month 3.5624 -0.0701 -0.2226 3 months 3.612 -0.0786 -0.1048 6 months 3.7281 -0.095 -0.0618 SWAP RATES

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 year 3.296 -0.0478 -0.1114 3 years 3.2688 -0.0456 -0.1195 5 years 3.6678 -0.0385 -0.1205 10 years 4.1298 -0.0182 -0.127 15 years 4.3825 -0.0042 -0.1187

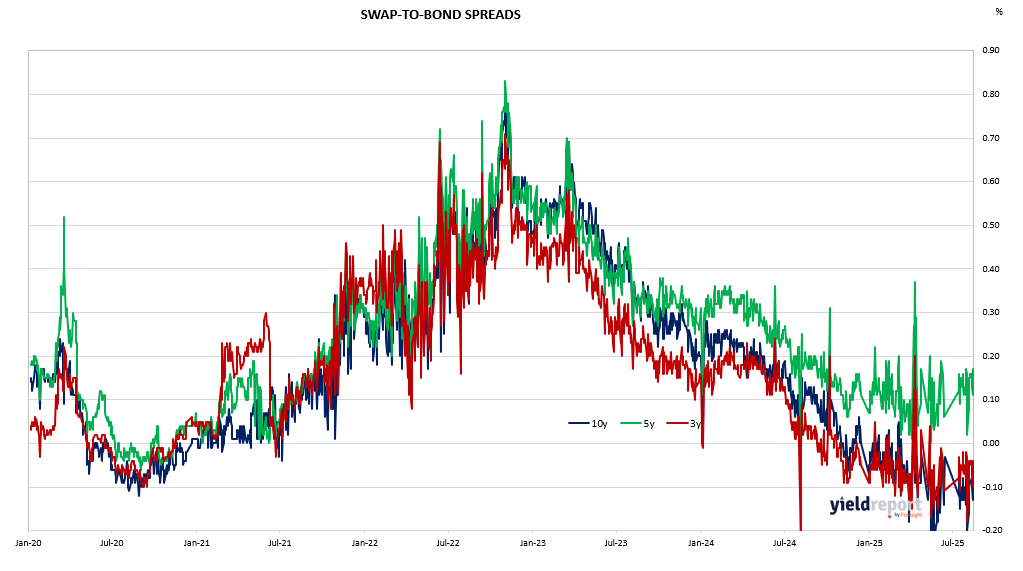

Exhibit 1: Australian 3Y/10Y Bond Yield