Summary: 3-month BBSW up 2bps, 6-month BBSW up 3bps; swap rates rise; swap spreads widen except at long end.

3-month BBSW added 2bps to 0.17% while 6-month BBSW finished the week 3bps higher at 0.54%.

Swap rates rose along the curve but not quite as much as their Commonwealth Government benchmarks at the front and by more at the long end. By the end of the week, the 1-year rate had added 5bps to 0.93%, the 3-year rate had risen by 12bps to 2.14%, the 5-year had gained 14bps to and 2.53% while 10-year and 15-year rates both finished 12bps higher at 2.76% and 2.84% respectively.

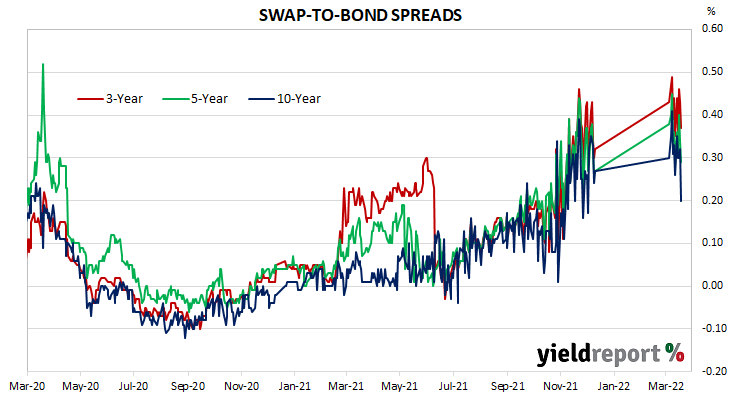

As a result, swap spreads tightened. By the end of the week, the 3-year spread had shed 8bps to 0.35%, the 5-year spreAs a result, swap spreads widened at the short end and the belly but tightened at the long end. By the end of the week, the 3-year spread had added 2bps to 0.37%, the 5-year spread had gained 1bp to 29bps while the 10-year spread finished 6bps lower at 20bps.

NB. Spreads are calculated with respect to “spot” Australian Commonwealth Government bond yields.

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 0.01 | -0.02 | -0.01 |

| 90 Day | 0.17 | 0.02 | 0.09 |

| 180 Day | 0.54 | 0.03 | 0.25 |

| 1 Year | 0.93 | 0.05 | 0.26 |

| 3 Year | 2.14 | 0.12 | 0.28 |

| 5 Year | 2.53 | 0.14 | 0.29 |

| 10 Year | 2.76 | 0.12 | 0.28 |

| 15 Year | 2.84 | 0.12 | 0.29 |