Summary: 3-month BBSW steady, 6-month BBSW down 1bp; swap rates increase at short end, belly, fall further out; swap spreads wider except at belly.

3-month BBSW remained steady at 0.07% while 6-month BBSW slipped 1bp to 0.23%.

Swap rates increased at the short end and at the belly but fell further out along the curve, somewhat like their Commonwealth Government benchmarks. By the end of the week, the 1-year rate had added 4bps to 0.48%, the 3-year rate had gained 6bps to 1.39% and the 5-year rate had increased by 3bps to 1.78% while the 10-year rate had shed 2bps to 2.11% and the 15-year rate had lost 3bps at 2.24%.

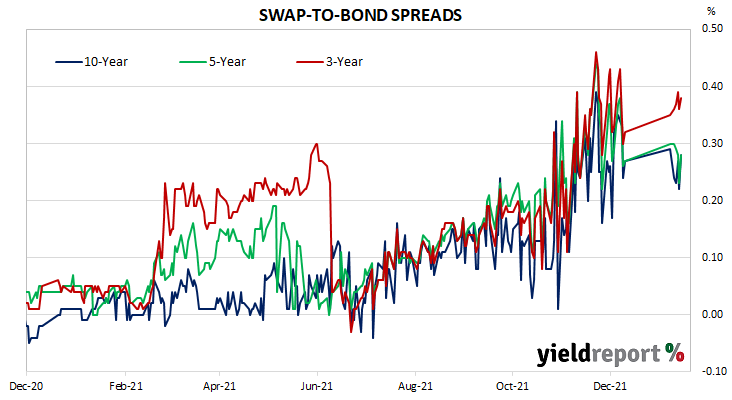

As a result, swap spreads widened along the curve except at the belly where they narrowed. By the end of the week, the 3-year spread had gained 2bps to 38bps, the 5-year spread had narrowed by 2bps to 28bps while the 10-year spread finished 4bps higher at 28bps.

NB. Spreads are calculated with respect to “spot” Australian Commonwealth Government bond yields.

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 0.02 | 0.00 | 0.00 |

| 90 Day | 0.07 | 0.00 | 0.01 |

| 180 Day | 0.23 | -0.01 | 0.05 |

| 1 Year | 0.48 | 0.04 | 0.14 |

| 3 Year | 1.39 | 0.06 | 0.15 |

| 5 Year | 1.78 | 0.03 | 0.18 |

| 10 Year | 2.11 | -0.02 | 0.20 |

| 15 Year | 2.24 | -0.03 | 0.20 |