Both the physical bank bill rate and 3 month BBSW remained unchanged at 1.97%.

Swap rates increased all along the curve but they lagged their Commonwealth benchmarks. The 1 year rate rebounded 4bps to 2.03%, the 3 year rate increased by 3bps to 2.19%, 5 year rates gained 4bps to 2.53% while 10 year rates jumped 6bps to 2.89% and the 15 year rate added 5bps to 3.05%.

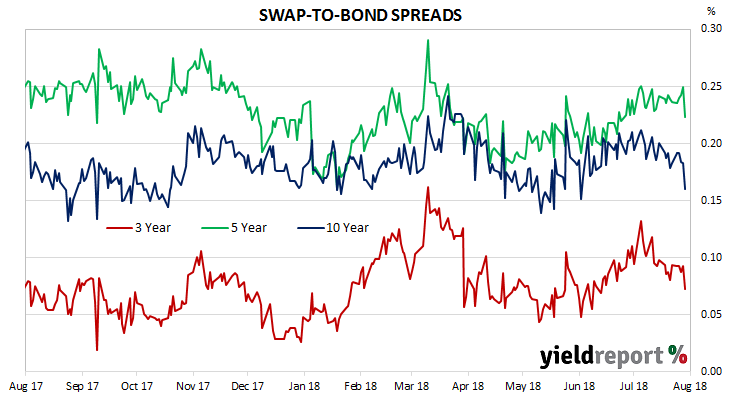

As a result, swap-to-bond spreads tightened across the curve; 3 year spreads, 5 year spreads and 10 year spreads all lost 2bps to 7bps, 22bps and 16bps respectively.

AFMA BBSW - SWAP RATES

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 1.88 | 0.01 | -0.12 |

| 90 Day | 1.97 | 0.00 | -0.14 |

| 180 Day | 2.15 | 0.00 | -0.07 |

| 1 Year | 2.03 | 0.04 | 0.00 |

| 3 Year | 2.19 | 0.03 | 0.01 |

| 5 Year | 2.53 | 0.04 | 0.01 |

| 10 Year | 2.89 | 0.06 | 0.04 |

| 15 Year | 3.05 | 0.05 | 0.03 |