Summary: Cash rate expectations slightly higher; cash rate now expected to average 3.87% in August 2023; 3-month BBSW up 8bps; three increases to surveyed ADI cash rates.

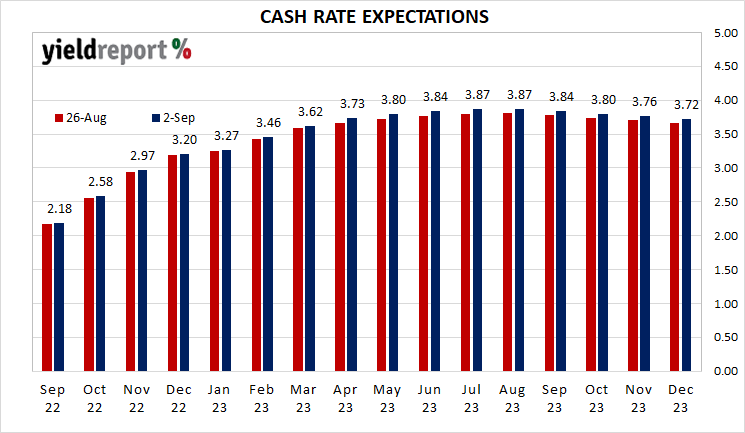

Expectations for the path of actual cash rate through the remainder of 2022 and most of 2023 moved slightly higher in comparison to its expected path at the end of the previous week. At the end of the week, contracts implied the cash rate would rise from the current rate of 1.81% to 2.18% in September, increase to 2.58% in October and then to 2.97% in November. August 2023 contracts implied 3.87%, up from 3.805% a week ago.

Since March 2020, the RBA has not enforced its cash rate target by draining liquidity from the banking system. As a result, the actual cash rate has been noticeably below the target rate. As such, contract prices only reflect expectations of the average actual cash rate in a given month and not the implied likelihood of the RBA changing its target.

Notable data or events which have the potential to affect domestic interest rate expectations came thick and fast through the week.

July’s preliminary retail sales report came out at the start of the week and it indicated retail spending had increased by 1.3% over the month, more than market expectations. Sales increased by 16.5% over the year, up from 12.0% in June.

Figures for approvals for the building of new homes were released the next day. Approval numbers plunged in July , driven by a drop in the high-rise segment.

Midweek, July’s private credit report indicated total lending had increased by 0.7% over the month, in line with expectations.

The June quarter report on construction work done was released at the same time. Work done fell by 3.8%, in contrast with expectations of a 2.5% increase.

The next day, July home loan approval numbers fell by more than expected, with more falls to come according to one senior economist.

The latest capital expenditure figures were also released. The report revealed a modest 0.3% decline in the June quarter. Spending was still up by 2.0% over the year to June.

3-month BBSW is a useful benchmark for cash rates and it finished the week 8bps higher at 2.49%. The RBA’s target for the overnight lending rate between banks is 1.85% but actual overnight interbank loans are still being negotiated at 1.81%, 4bps below the target but 6bps above the RBA’s exchange settlement account (ESA) rate for ADI deposits with it.

There were three increases made by deposit-taking institutions in our survey of cash account interest rates this week. Rates on RAMS’ Saver Account, Up Bank’s Saver Account and UBank’s Save Accounts were all raised by 50bps each. The average rate across the 23 accounts rose from 1.25% to 1.32%.

| Product | Interest Rate p.a. | Special Conditions |

|---|---|---|

| AMP Saver Account | 0.60% | |

| AMP Notice Account | 0.10% | |

| ANZ Premium | 0.15% | |

| ANZ Progress Saver | 1.65% | Minimum $10 deposit and no withdrawal per month |

| Arab Bank Online Savings | 1.00% | Minimum balance $500,000. |

| Bankwest Smart eSaver | 1.10% | On balances up to $500,000.99. No withdrawals per month |

| BOQ Fast Track Saver | 0.05% | Minimum monthly balance of $5000. |

| BoQ Bonus Interest Savings | 1.30% | Maximum 1 withdrawal per month. |

| CBA NetBank Saver | 0.85% | |

| CBA Goal Saver Account | 1.50% | On balances of $250,000 - $999,999. Minimum $200 deposit and no withdrawal per month. |

| Great Southern Bank | 1.70% | No maximum balance |

| Heritage Online Saver | 1.35% | Minimum balance $250,000 |

| ING Savings Accelerator | 2.10% | Minimum balance $150,000 |

| Macquarie CMA | 0.90% | Minimum balance $5000 |

| ME Online Savings | 2.20% | On balances up to$250,000. Make at least four tap & go purchases per month |

| NAB iSaver | 0.85% | |

| NAB Reward Saver | 1.75% | 1 deposit and no withdrawal per month |

| RAMS Saver Account | 1.15% | On balances $0 - $500,000. Minimum $200 deposit each month and no withdrawals |

| Suncorp Growth Saver | 2.40% | Minimum $200 deposit each month and no more than 1 withdrawal |

| UBank Save Account | 2.10% | Make 5 successful purchases using your Up or 2Up debit card or digital wallets in a month. |

| Up Saver Account | 2.85% | On a combined balance of upto $250,000. Minimum $200 deposit each month into Spend or Save accounts. |

| Westpac eSaver | 0.85% | |

| Westpac Reward Saver | 1.85% | Make a deposit to the account and ensure account balance is higher at the end of the month than the beginning. |