JCB find the YieldReport to be an invaluable summary of all debt market activity. Whilst we are focussed on the highest grade bonds it is important to see what is..Angus Coote, Executive Director, JCB Active Bond Fund

Signs of stress are emerging in US credit markets as investors grow increasingly cautious about economic growth and the sustainability of the AI investment boom. While markets are far from panic, risk premiums across investment-grade and high-yield bonds have risen toward multi-week highs, signalling subtle but broad-based unease. The shift in sentiment became clear when investors withdrew roughly 40% of orders from several corporate bond deals once final pricing was released, an unusually sharp attrition rate in a market where drop-offs typically hover around 20%. One investment-grade deal was even pulled entirely, highlighting deteriorating demand.

Money managers say a global market malaise, already pressuring equities, is flowing into credit. The S&P 500 has fallen for four straight days, while many of 2025’s high-flying tech names have stumbled as investors begin questioning whether artificial intelligence can justify its enormous hype and capex demands. Concerns are also raising that bond yields are not fully reflecting underlying growth risks.

The caution is amplified by an extraordinary surge in big-tech borrowing. Hyperscalers have issued US$121 billion in high-grade US-dollar bonds this year, far above the ~$28 billion annual average of the past five years, with US$81 billion issued since September alone. Investors are now questioning which AI leaders will ultimately generate returns, and which may over-invest.

Monday’s Amazon US$15 billion bond sale illustrated this dynamic: peak orders of US$80 billion collapsed to US$47 billion after pricing, a more than 40% drop.

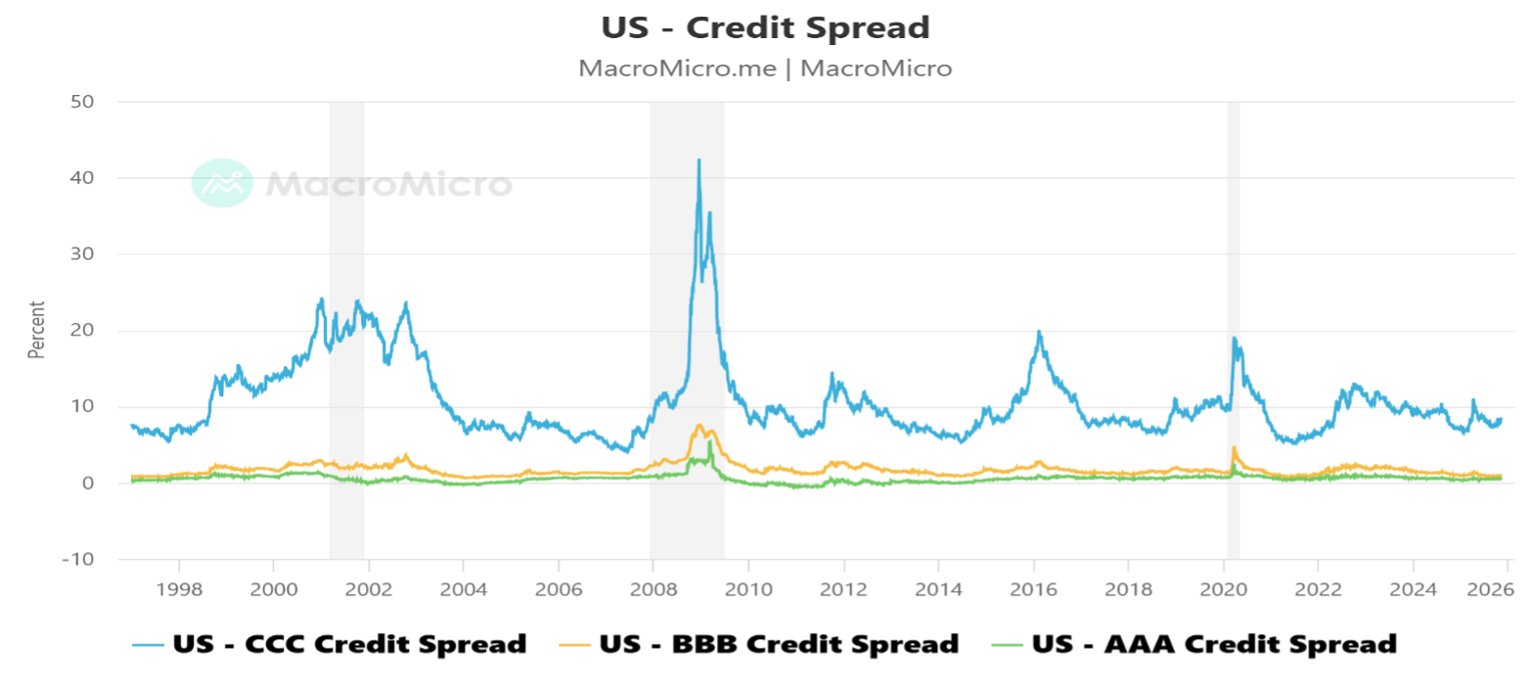

Market stress is also evident in lower-rated credits. CCC-rated bond yields climbed to 10.38%, the highest since August, and high-yield CDS indices weakened to multi-month lows. A recent Applied Digital bond dropped to 94 cents on the dollar before partially rebounding.

Despite these pressures, average high-grade spreads remain tight at 83 basis points, well below the decade average of 117 bps. For many investors, that’s the problem: valuations appear too rich relative to evolving macro and AI-related risks. As PineBridge’s Michael Kelly put it, “we’re getting paid so little on spread… in a technologically turbulent and rapidly changing world.”