Summary: Corporate bond spreads 3bps tighter on average; swap spreads tighter; iTraxx decreases.

Corporate spreads finished the week about 3bps tighter on average as corporate bond yields lagged the rises of most of their Commonwealth counterparts. The majority of spreads’ week-on-week changes at the individual level were within a range of -3bps to +8bps and the exceptions were limited to a few 2024 lines.

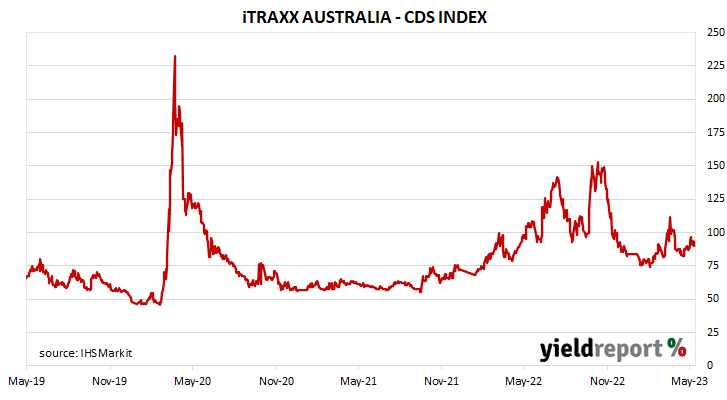

One of the two other main measures of corporate risk, swap-to-bond spreads, tightened. The other main measure, credit default swap premiums, decreased on average. The Australian credit default swap index, the iTraxx Australia Series 37, finished 2.5 points lower at 90.00 points.

AUSTRALIAN CORPORATE BONDS

| ISSUER | MATURITY | COUPON (%) | RATING | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|---|

| ANZ BANK | 16-Aug-23 | 5.00 | AA- | 4.24 | 0.02 | 4.28 | 4.23 | |

| SUNCORP-METWAY | 13-Sep-23 | 3.00 | 4.26 | 0.01 | 4.26 | 4.24 | ||

| QANTAS | 10-Oct-23 | 4.40 | 4.94 | 0.04 | 4.94 | 4.92 | ||

| AUSTRALIA POST | 13-Nov-23 | 5.50 | A+ | 4.30 | 0.04 | 4.30 | 4.29 | |

| WESTPAC | 21-Nov-23 | 5.25 | 4.26 | 0.02 | 4.28 | 4.26 | ||

| FONTERRA | 26-Feb-24 | 5.50 | A- | 4.34 | 0.04 | 4.35 | 4.34 | |

| NATIONAL AUST. BANK | 11-Mar-24 | 5.00 | 4.27 | 0.02 | 4.28 | 4.27 | ||

| RABOBANK NEDERLANDS AUST | 11-Apr-24 | 5.50 | A+ | 4.41 | 0.02 | 4.45 | 4.41 | |

| COMMONWEALTH BANK | 27-May-24 | 4.75 | 4.30 | 0.04 | 4.33 | 4.30 | ||

| AURIZON NETWORK | 21-Jun-24 | 4.00 | BBB+ | 4.74 | 0.10 | 4.78 | 4.72 | |

| MACQUARIE BANK | 7-Aug-24 | 1.75 | A+ | 4.38 | 0.01 | 4.43 | 4.38 | |

| WELLS FARGO | 27-Aug-24 | 4.75 | BBB+ | 4.85 | 0.04 | 4.90 | 4.85 | |

| WOOLWORTHS | 20-May-25 | 1.85 | BBB | 4.22 | 0.03 | 4.31 | 4.22 | |

| UNIVERSITY OF SYDNEY | 28-Aug-25 | 3.75 | 4.06 | 0.02 | 4.16 | 4.06 | ||

| NBN CO | 3-Dec-25 | 1.00 | 4.34 | 0.02 | 4.45 | 4.34 | ||

| APPLE | 10-Jun-26 | 3.60 | AA+ | 3.95 | 0.02 | 4.07 | 3.95 | |

| COMMONWEALTH BANK | 11-Jun-26 | 4.20 | AA- | 4.23 | 0.02 | 4.33 | 4.23 | |

| ANZ BANK | 22-Jul-26 | 4.00 | AA- | 4.22 | 0.01 | 5.72 | 4.22 | |

| NBN CO | 28-Sep-26 | 4.75 | 4.25 | -0.03 | 4.41 | 4.25 | ||

| QANTAS | 12-Oct-26 | 4.75 | NR | 5.07 | 0.01 | 5.18 | 5.07 | |

| AUST. PACIFIC AIRPORTS | 4-Nov-26 | 3.75 | BBB+ | 4.59 | 0.04 | 4.67 | 4.59 | |

| WSO FINANCE | 1-Dec-26 | 4.00 | A+ | 4.13 | 0.01 | 4.24 | 4.13 | |

| WSO FINANCE | 31-Mar-27 | 4.50 | 4.55 | 0.00 | 4.67 | 4.55 | ||

| NBN CO | 14-Apr-27 | 4.20 | 4.36 | -0.02 | 4.49 | 4.36 | ||

| TELSTRA | 19-Apr-27 | 4.00 | A- | 4.22 | 0.00 | 4.33 | 4.22 | |

| PACIFIC NATIONAL FINANCE | 12-May-27 | 5.40 | BBB- | 6.26 | 0.01 | 6.38 | 6.26 | |

| LENDLEASE | 27-Oct-27 | 3.40 | 5.83 | 0.11 | 5.96 | 5.80 | ||

| FONTERRA | 2-Nov-27 | 4.00 | A- | 4.45 | 0.01 | 4.55 | 4.45 | |

| WOOLWORTHS | 15-Nov-27 | 1.85 | BBB | 4.39 | -0.01 | 4.52 | 4.39 | |

| AUSTRALIA POST | 8-Dec-27 | 4.99 | 4.38 | 0.00 | 4.50 | 4.38 | ||

| MACQUARIE GROUP | 15-Dec-27 | 4.15 | BBB+ | 5.41 | 0.00 | 5.54 | 5.41 | |

| NBN CO | 2-Jun-28 | 2.15 | 4.70 | -0.02 | 4.84 | 4.70 | ||

| WESFARMERS | 23-Jun-28 | 1.94 | A- | 4.58 | -0.02 | 4.71 | 4.58 | |

| AUSNET | 21-Aug-28 | 4.20 | BBB+ | 5.13 | 0.08 | 5.20 | 5.13 | |

| QANTAS | 27-Sep-28 | 3.15 | 5.45 | -0.02 | 5.59 | 5.45 | ||

| AIRSERVICES AUST | 15-Nov-28 | 5.40 | 4.11 | -0.01 | 4.24 | 4.11 | ||

| AUSNET | 31-Jul-29 | 2.60 | BBB+ | 5.38 | 0.04 | 5.49 | 5.38 | |

| QANTAS | 27-Nov-29 | 2.95 | 5.87 | -0.03 | 6.01 | 5.87 | ||

| WOOLWORTHS | 20-May-30 | 2.80 | BBB | 5.15 | -0.03 | 5.29 | 5.15 | |

| QANTAS | 9-Sep-30 | 5.25 | 5.77 | -0.03 | 5.91 | 5.77 | ||

| NBN CO | 16-Dec-30 | 2.20 | 5.15 | -0.03 | 5.30 | 5.15 | ||

| BRISBANE AIRPORT | 30-Dec-30 | 4.50 | BBB | 5.40 | 0.01 | 5.54 | 5.40 | |

| LENDLEASE | 31-Mar-31 | 3.70 | 6.88 | 0.08 | 7.03 | 6.88 | ||

| WESFARMERS | 23-Jun-31 | 2.55 | A- | 5.22 | -0.04 | 5.36 | 5.22 | |

| WOOLWORTHS | 15-Nov-31 | 2.75 | BBB | 5.41 | -0.04 | 5.55 | 5.41 |