Summary:

U.S. corporations kicked off September 2025 with a surge in debt issuance, capitalizing on falling borrowing costs and strong investor demand ahead of anticipated Federal Reserve rate cuts. Investment-grade bond sales totalled $56.4 billion through Thursday, alongside $9.6 billion in high-yield (junk) bonds—marking the busiest week since March, though slightly below last year’s comparable figures.

Companies are eager to lock in current yields before rates decline, prompting a narrowing of credit spreads between corporate bonds and Treasurys. On Tuesday alone, 27 issuers raised $40.8 billion, nearly matching last year’s post–Labour Day record. Merck led with a $6 billion issuance to fund its $10 billion acquisition of Verona Pharma, while Ford’s financial arm issued $1.25 billion in bonds maturing in 2030.

Investor appetite extended to lower-rated issuers as well, with renewed flows into high-yield mutual funds and ETFs enabling refinancing and new borrowing. This marks a sharp turnaround from April’s market freeze triggered by tariff concerns.

September remains a historically active month for corporate issuance, with firms typically front-loading funding needs for the remainder of the year. The current environment, marked by stable financial asset pricing despite geopolitical noise, offers a favourable window for both issuers and investors to secure capital and returns before volatility resurfaces.

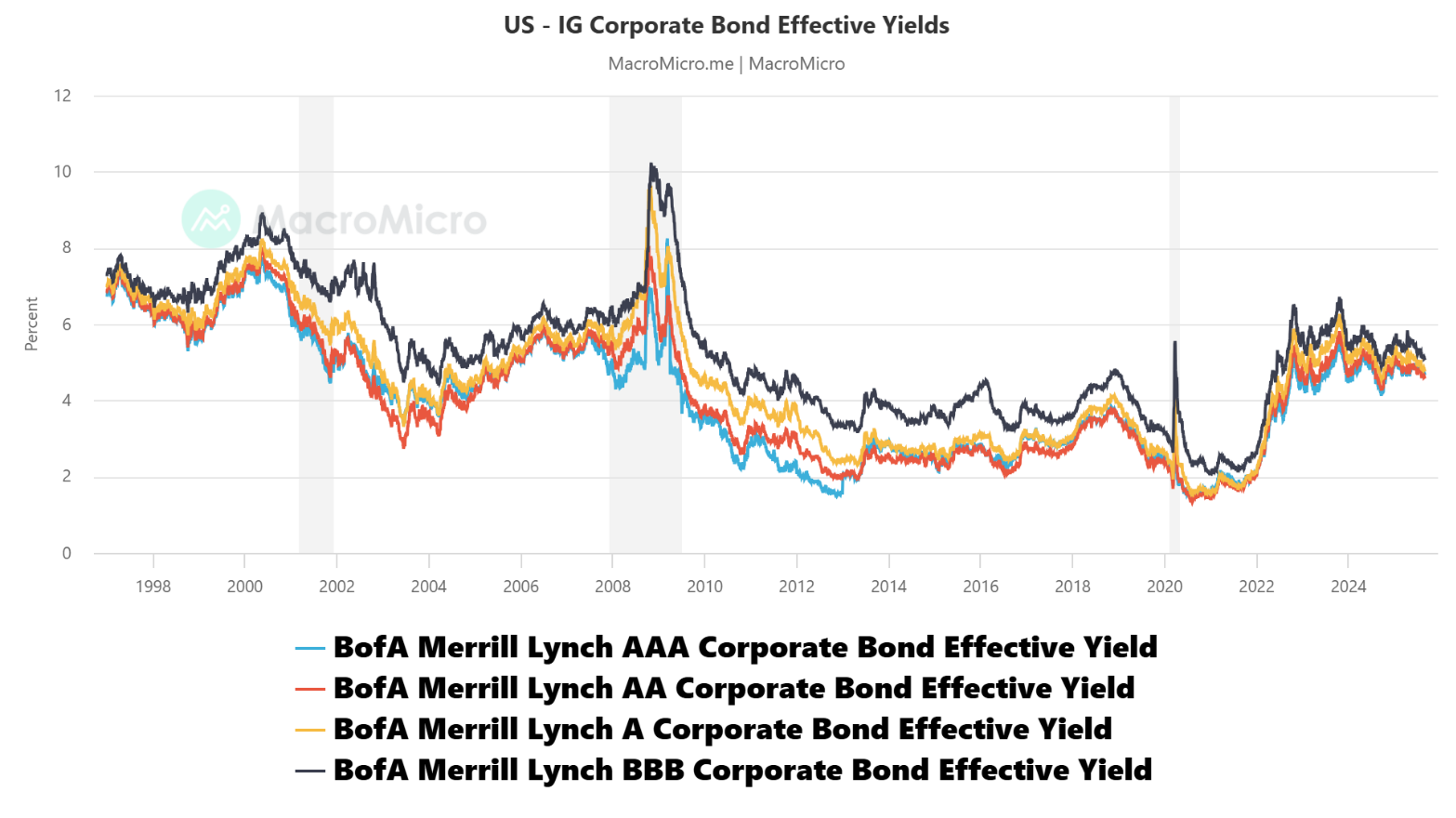

Figure 1- US Corporate Bonds Yields

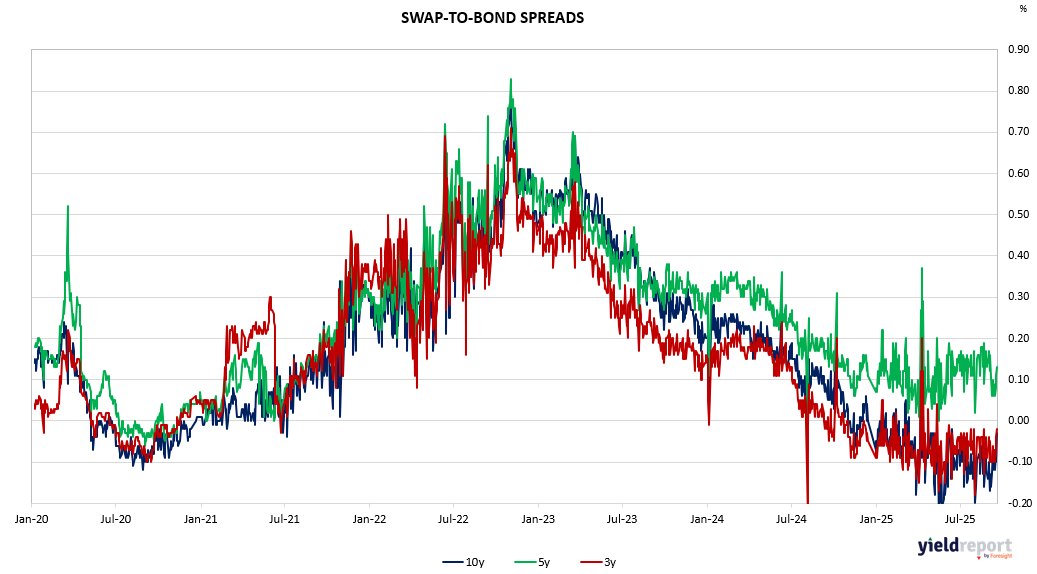

Figure 2: Australian Swap to Bond Spreads