Summary –

The ASX-listed bank hybrid market continues to show resilience amid a steady rate environment, with trading margins and running yields reflecting investor appetite for income-generating instruments.

Performance Highlights:

- Running Yields: Most bank-issued hybrids are offering running yields between 6.2% and 7.5%, with standout performers like Bank of Queensland (BOQPF, BOQPG) and Westpac (WBCPL) delivering yields near the top of the range.

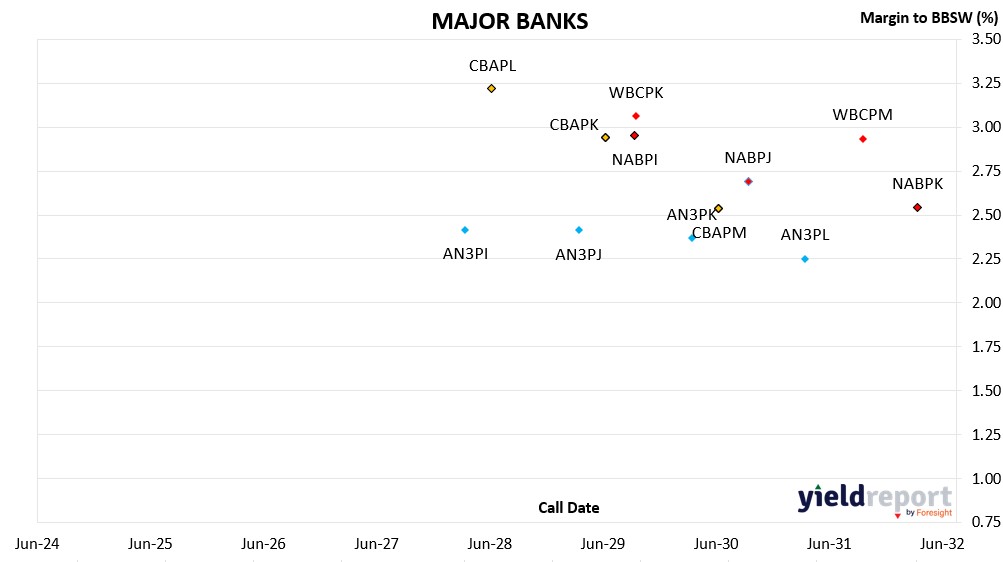

- Trading Margins: Margins have compressed slightly across longer-dated hybrids, with major bank notes such as ANZ’s AN3PK and CBA’s CBAPM trading at margins below 2.6%, indicating strong demand and lower perceived risk.

- Price Stability: Daily price movements were modest, with most securities recording changes of 0.01% to 0.05%, suggesting a stable secondary market with limited volatility.

- Short-Dated Notes: Hybrids maturing in 2025–2026, such as Westpac’s WBCPH and AMP’s AMPPB, continue to trade near par or slightly above, with elevated running yields above 8%, reflecting their shorter duration and higher margins.

-

Issuer Trends:

- Major Banks (CBA, ANZ, NAB, Westpac): Continue to dominate issuance volumes, with multiple tranches across varying maturities. Their hybrids remain popular for their liquidity and credit quality.

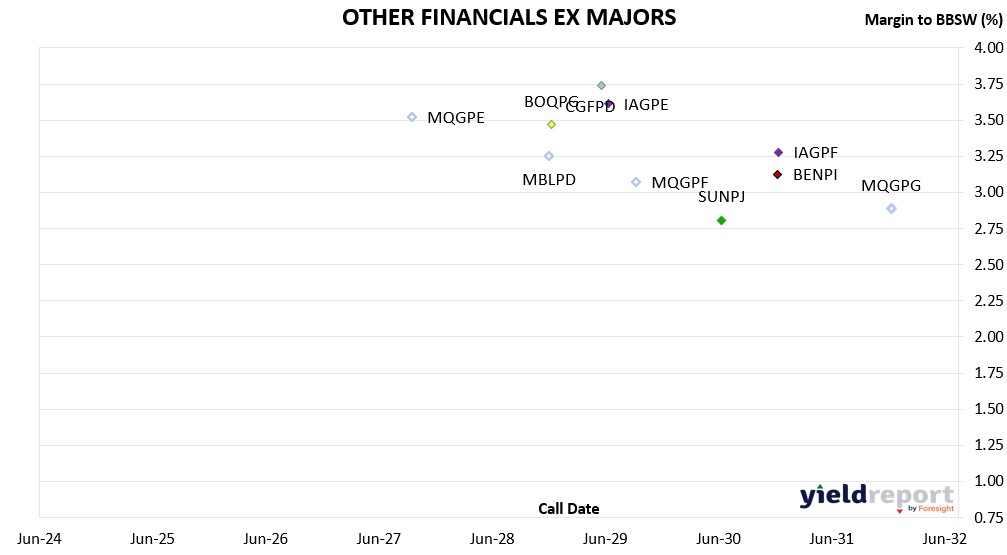

- Regional Banks & Non-Bank Issuers: Names like Bendigo Bank, Suncorp, and Judo Capital offer competitive margins and yields, appealing to investors seeking diversification beyond the Big Four.

-

Close Previous Close Change Australian 3-year bond (%) 3.43 3.447 -0.017 Australian 10-year bond (%) 4.288 4.345 -0.057 Australian 30-year bond (%) 5.031 5.093 -0.062 United States 2-year bond (%) 3.501 3.561 -0.06 United States 10-year bond (%) 4.08 4.134 -0.054 United States 30-year bond (%) 4.7665 4.8392 -0.0727 ASX-Listed Hybrids (Non-standard)

COMPANY CODE BOND TYPE CALL DATE ISSUE MARGIN (inc frank) TRADING MARGIN DAY CLOSING PRICE RUNNING YIELD Nufarm NFNG Step Up Perpetual 3.90% 5.23% 0.00% 89.8 8.81% Ramsay Health Care RHCPA Preference Share Perpetual 4.85% 4.54% 0.00% 108.99 8.13%