| Close | Previous Close | Change | |

|---|---|---|---|

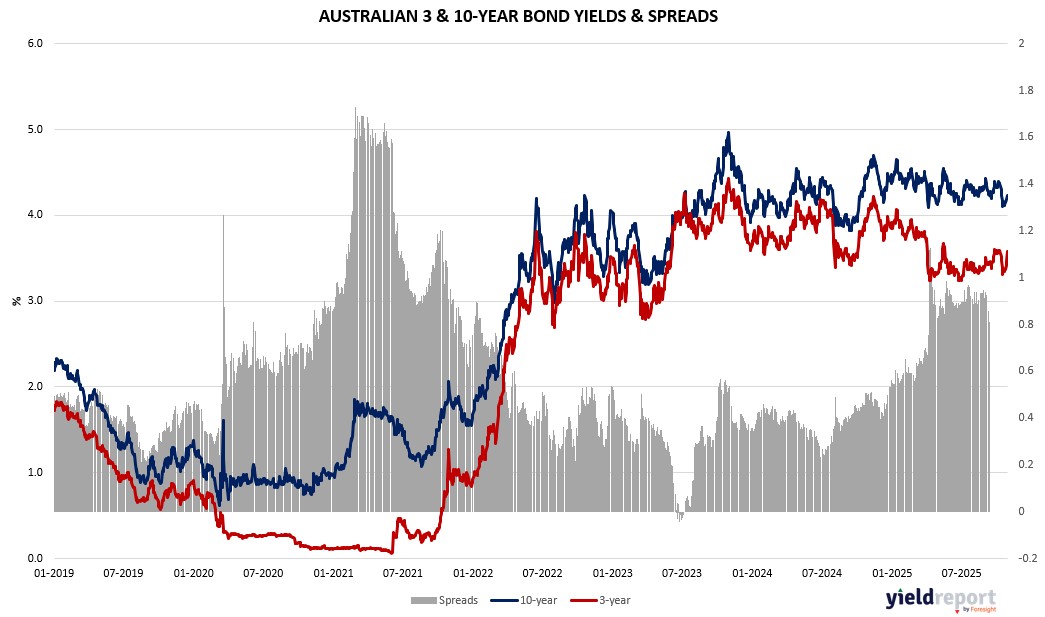

| Australian 3-year bond (%) | 3.649 | 3.616 | 0.033 |

| Australian 10-year bond (%) | 4.348 | 4.31 | 0.038 |

| Australian 30-year bond (%) | 4.995 | 4.946 | 0.049 |

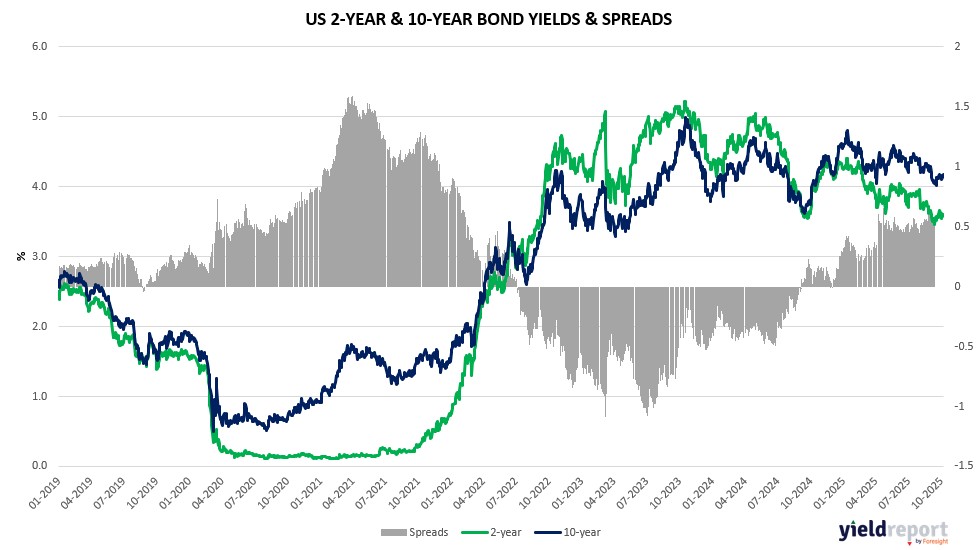

| United States 2-year bond (%) | 3.6 | 3.609 | -0.009 |

| United States 10-year bond (%) | 4.107 | 4.105 | 0.002 |

| United States 30-year bond (%) | 4.69 | 4.6647 | 0.0253 |

Overview of the Australian Bond Market

Australian government bond yields climbed on November 3 as stronger-than-expected building approvals and bank results reinforced economic stability, reducing near-term easing bets ahead of the RBA’s decision and amid global yield upticks. The 10-year yield rose five basis points to 4.34%, the 2-year advanced four to 3.59%, the 5-year gained five to 3.81%, and the 15-year climbed six to 4.66%. The AUD/USD edged up 0.24% to 0.656, supported by US dollar wavers, while commodity weakness pressured metals.

September approvals jumped 12% month-on-month versus 5% forecast, with year-on-year at 12.4%, signaling housing resilience despite high rates, though exports plunged 7.8% and trade surplus narrowed to A$1.825 billion, missing A$4 billion estimates. Reuters polling shows unanimous hold at 3.6% on November 4, with minutes from September highlighting data dependence; Q3’s 1.0% trimmed mean inflation exceeded the RBA’s 0.9% threshold, shifting 2025 cut expectations to none from most economists. S&P Global Services and Composite PMIs finalize November 4 at 53.1 and 52.6, potentially guiding the statement, which may retain easing option without commitment.

An aversion to cuts could lift AUD/USD toward 0.6707, per analysis, while balance of goods on November 6 and RBA’s Bullock comments loom. Yields track US moves amid Fed uncertainty, with AI deals and US growth tailwinds seen limiting downside if tariffs ease further.

Overview of the US Bond Market

Bond traders pushed Treasury yields higher on November 3 as Fed speakers’ mixed signals clouded the December rate path and AI-driven equity gains underscored economic resilience, prompting a reassessment of easing bets. The 10-year yield climbed two basis points to 4.10%, the 2-year advanced two to 3.59%, and the 30-year rose three to 4.68%, steepening the 2s-10s curve to +50.4 basis points. The move came amid broader dollar gains and crypto weakness, with Bitcoin down 3%, as markets weighed Goolsbee’s inflation caution against Miran’s push for deeper cuts and Daly’s balanced view.

A scarcity of data due to the shutdown amplifies focus on upcoming releases like ISM services PMI on November 5, non-farm payrolls on November 5, and third-quarter GDP advance on November 6, which could sway expectations for a half-point of easing by year-end. Treasury Secretary comments were absent, but ongoing AI infrastructure deals from Microsoft ($9.7 billion with IREN) and Amazon bolster the case for sustained growth, potentially pressuring yields if they signal less Fed support needed. Swap contracts still price in about a 50% chance of a December cut, though Evercore ISI’s Krishna Guha sees lingering dovish anxiety tilting odds toward easing.

In futures, asset managers trimmed net long positions across tenors last week per CFTC data, with leveraged funds reducing shorts in the classic Bond contract. Dealers expect steady coupon auction sizes for August-October, aligning with April guidance, as the department signals no changes. The resilience of equities amid tariff uncertainties and Fed splits has some bears arguing rates stay higher longer, though narrow credit spreads and buoyant stocks don’t fully reflect policy stance, per Miran.