| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.556 | 3.553 | 0.003 |

| Australian 10-year bond (%) | 4.32 | 4.326 | -0.006 |

| Australian 30-year bond (%) | 5.015 | 5.018 | -0.003 |

| United States 2-year bond (%) | 3.555 | 3.545 | 0.01 |

| United States 10-year bond (%) | 4.098 | 4.108 | -0.01 |

| United States 30-year bond (%) | 4.7007 | 4.7173 | -0.0166 |

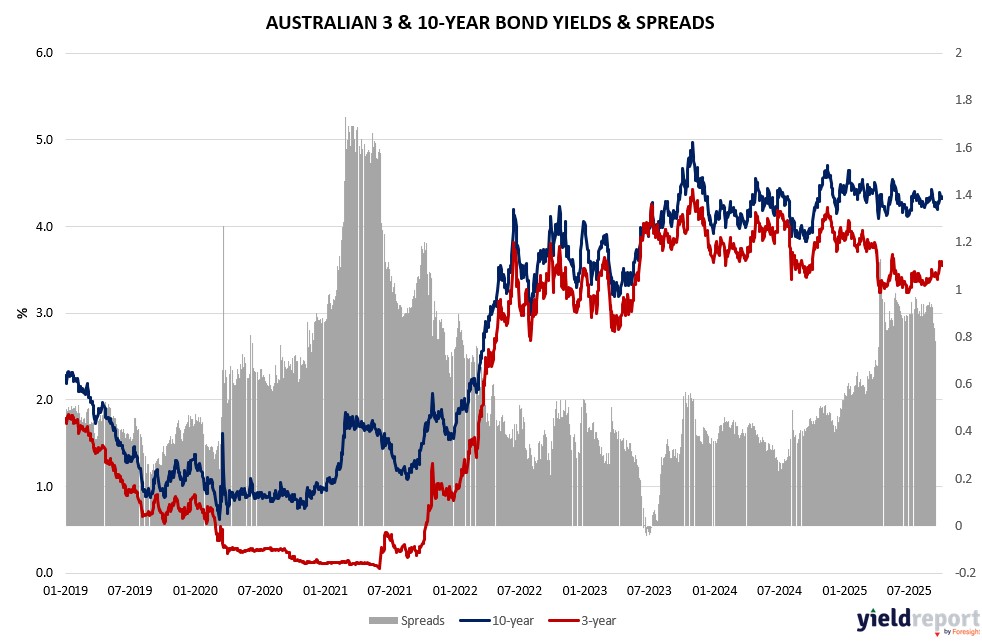

Overview of the Australian Bond Market

Australian government bond yields were mixed as markets digested weaker trade data and building approvals, with the RBA’s steady cash rate reinforcing stability amid global shutdown ripple effects. The 10-year yield held steady at 4.33%, while the 2-year raised one basis point to 3.49% and the 15-year eased to 4.67%, reflecting cautious bets on policy amid US Fed uncertainty.

Traders see limited tailwinds from rate cuts, justified by signs of growth like the composite PMI at 52.4, but the trade surplus miss and import growth of 3.2% highlighted external pressures. Consumer credit data due Tuesday is polled at 15 billion, potentially influencing sentiment, while FOMC minutes Wednesday could sway global yields. West Texas Intermediate crude rose to $60.67, supporting energy-linked bonds, as the ASX’s weekly gain underscored diversification into risk assets.

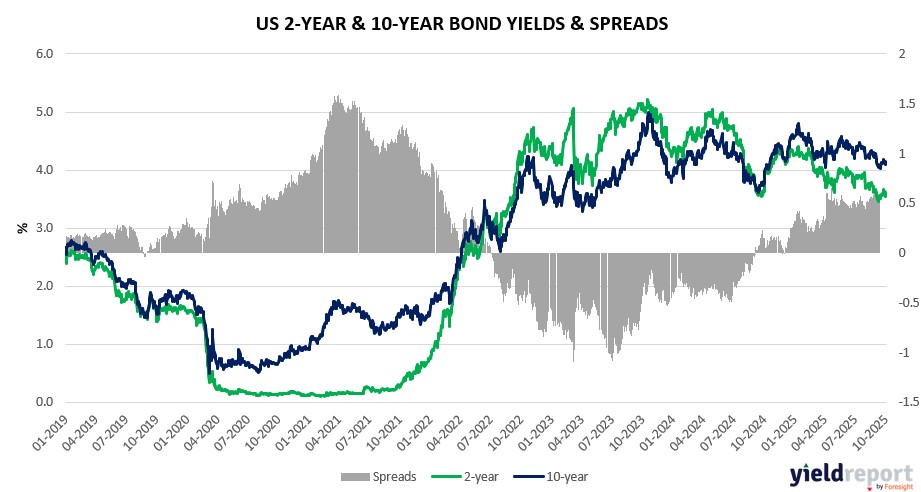

Overview of the US Bond Market

Bond traders pared long positions in Treasuries over the past week, bracing for delayed labor data and Fed signals amid the government shutdown, which has heightened focus on potential extensions and their impact on fiscal stability. A rally in longer-dated bonds pushed the 10-year yield down three basis points to 4.12%, with 30-year yields advancing to 4.71%, as oil climbed on Gaza tensions and gold hit $3,887 an ounce on inflation worries.

Treasury Secretary Karoline Leavitt reiterated plans to pull funds from Democratic areas, adding to market volatility, while strategists at Morgan Stanley priced the shutdown lasting 10 to 29 days via options. Economic resilience, including stalled but non-recessionary service-sector growth at ISM’s reading, has tempered aggressive rate-cut bets, with swap contracts now implying just under a half-point of easing by year-end. Fed officials like Austan Goolsbee urged caution on cuts, contrasting with calls for larger moves if housing costs spike.

JPMorgan’s client survey showed net longs at a two-month low, with asset managers trimming positions by $23.5 million per basis point across tenors, concentrated in 5-year and 30-year contracts. Leveraged funds reduced shorts in the classic bond by $5 million. Dealers expect steady coupon auction sizes for August-October, aligning with April guidance, though a $1 billion increase in 10- and 5-year re-openings is anticipated. The Bloomberg Dollar Spot Index fell 0.1%, supporting Treasuries as the euro and pound strengthened.