| Close | Previous Close | Change | |

|---|---|---|---|

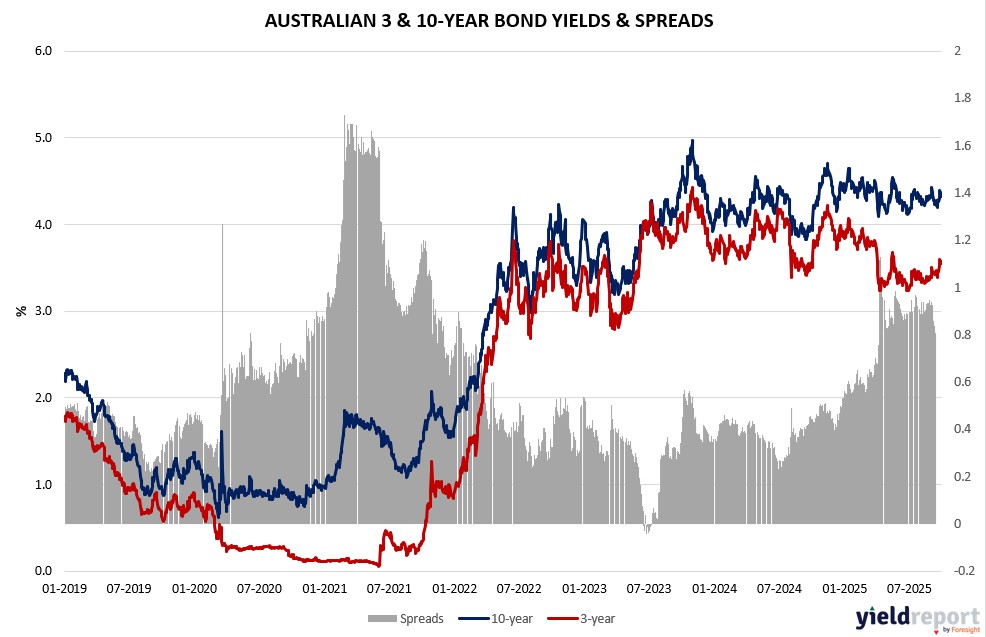

| Australian 3-year bond (%) | 3.592 | 3.574 | 0.018 |

| Australian 10-year bond (%) | 4.348 | 4.324 | 0.024 |

| Australian 30-year bond (%) | 5.025 | 4.992 | 0.033 |

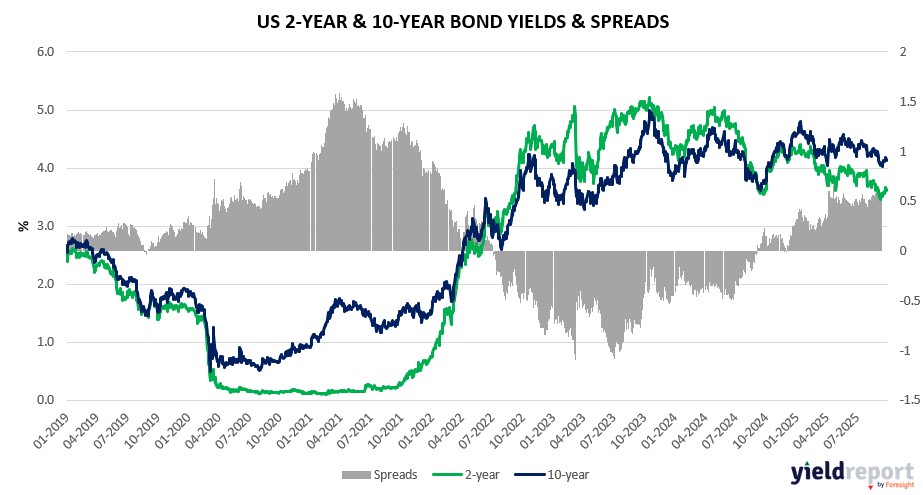

| United States 2-year bond (%) | 3.611 | 3.61 | 0.001 |

| United States 10-year bond (%) | 4.154 | 4.137 | 0.017 |

| United States 30-year bond (%) | 4.7438 | 4.7075 | 0.0363 |

Overview of the Australian Bond Market

Australian government bonds showed mixed moves on October 1, 2025, with the 10-year yield up 4 basis points to 4.33% amid US shutdown volatility and local trade concerns, while the 2-year held at 3.48% and 5-year dipped to 3.74%. The 15-year rose to 4.66%.

August building approvals plunged 6% against 3% expectations, underscoring uneven recovery, with S&P Global Manufacturing PMI final at 51.4. Wednesday’s goods balance anticipated at A$6.2 billion, bolstered by 3.3% export growth but tempered by imports and China’s slowdown. RBA’s recent hold at 3.6% maintains hawkish stance on sticky inflation. US impasse risks economic data voids, heightening global policy uncertainty and potentially curbing demand, while Trump’s protectionism adds inflationary supply chain pressures for the RBA ahead of Thursday’s Financial Stability Review.

Overview of the US Bond Market

Treasuries rallied on October 1, 2025, with the 10-year yield declining 5 basis points to 4.10% as ADP’s weak payrolls and ISM data bolstered bets for Fed easing amid shutdown-induced data gaps. The 2-year fell to 3.53%, 5-year to 3.67%, and 30-year to 4.71%. Shorter maturities adjusted with 3-month at 3.84% and 6-month at 3.69%.

ADP’s 32,000 drop, influenced by opaque benchmarking to BLS data, highlights slowing hiring across leisure, services, and manufacturing, with economists like Morgan Stanley questioning reliability but noting low-hire environment risks from Citigroup’s Veronica Clark. Shutdown delays official jobs report, complicating October decisions, but Berenberg’s Atakan Bakiskan argues sufficient private info for a 25bp insurance cut. Capital Economics’ Thomas Ryan flags potential prolonged payroll drags from layoffs, unlike past minimal effects averaging 0.35% GDP hit.

Wage gains softened to 6.6% for changers, easing inflation worries, though Fed remains cautious. Supreme Court lets Fed’s Lisa Cook stay pending January arguments, countering Trump’s Powell criticism as an “obstructionist.”