| Close | Previous Close | Change | |

|---|---|---|---|

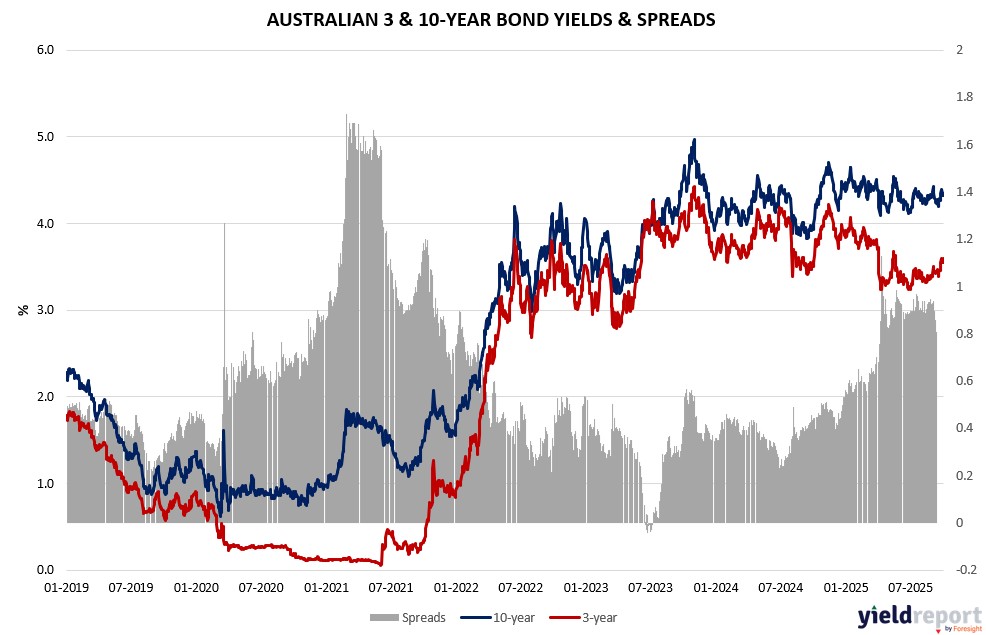

| Australian 3-year bond (%) | 3.553 | 3.592 | -0.039 |

| Australian 10-year bond (%) | 4.326 | 4.348 | -0.022 |

| Australian 30-year bond (%) | 5.018 | 5.025 | -0.007 |

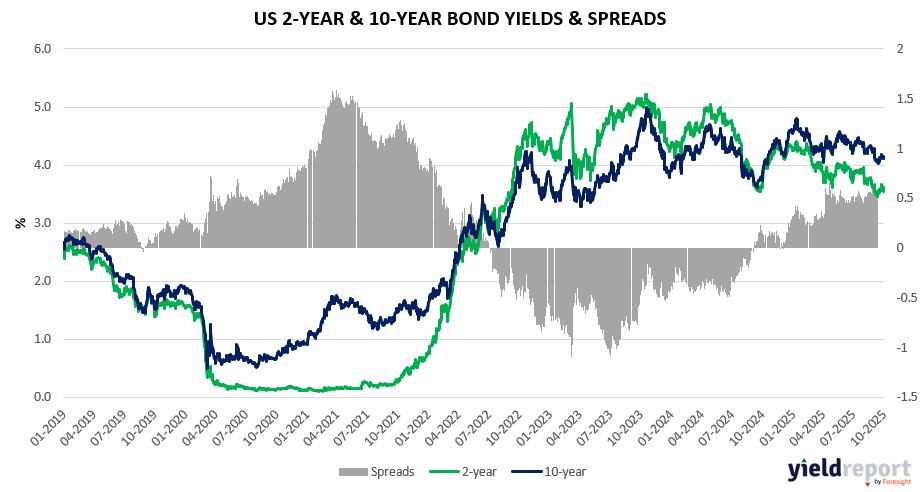

| United States 2-year bond (%) | 3.545 | 3.611 | -0.066 |

| United States 10-year bond (%) | 4.108 | 4.154 | -0.046 |

| United States 30-year bond (%) | 4.7173 | 4.7438 | -0.0265 |

Overview of the Australian Bond Market

Australian government bonds gained on October 2, 2025, with the 10-year yield down 5 basis points to 4.31% amid global shutdown volatility and local data misses supporting caution. The 2-year fell to 3.47%, 5-year to 3.73%, and 15-year to 4.66%.

August trade surplus plunged to A$1.825 billion against A$6.2 billion expectations, hit by 7.8% export drop outweighing 3.2% imports, signaling vulnerability to China’s slowdown and US tariffs. Household spending’s weak 0.1% underscores conservative consumers, per AMP Economics noting nominal 5% growth masks per capita volumes at 0.4% amid population and prices. S&P Global Services PMI at 52.4 confirms expansion but uneven recovery post-RBA’s 3.6% hold. US impasse amplifies policy uncertainty, potentially curbing demand and inflating costs for RBA ahead of Financial Stability Review.

Overview of the US Bond Market

Treasuries saw yields dip slightly on October 2, 2025, with the 10-year declining 1 basis point to 4.09% as shutdown concerns and labor signals kept Fed cut bets alive despite data voids. The 2-year fell to 3.54%, 5-year to 3.67%, and 30-year to 4.69%. Shorter ends held with 3-month at 3.85% and 6-month at 3.69%.

Challenger’s September hiring slowdown with fewer cuts underscores cooling market, aligning with JPMorgan’s Kim Crawford on cyclical weakness and absent wage growth, bolstering expectations for quarter-point cuts in October and December. Shutdown delays initial claims and nonfarm payrolls, with Charles Schwab’s Joe Mazzola noting prolonged closure could halt late-October easing without inflation reads, potentially hurting growth as per Treasury Secretary Scott Bessent. Past shutdowns had negligible macro effects, but layoff threats could extend payroll drags.

Dollar rose after four losses, gold cooled from records. OPEC+ supply fears deepened oil glut, pushing WTI below $61.