| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.556 | 3.522 | 0.034 |

| Australian 10-year bond (%) | 4.341 | 4.299 | 0.042 |

| Australian 30-year bond (%) | 5.05 | 5.004 | 0.046 |

| United States 2-year bond (%) | 3.604 | 3.565 | 0.039 |

| United States 10-year bond (%) | 4.141 | 4.11 | 0.031 |

| United States 30-year bond (%) | 4.7428 | 4.7252 | 0.0176 |

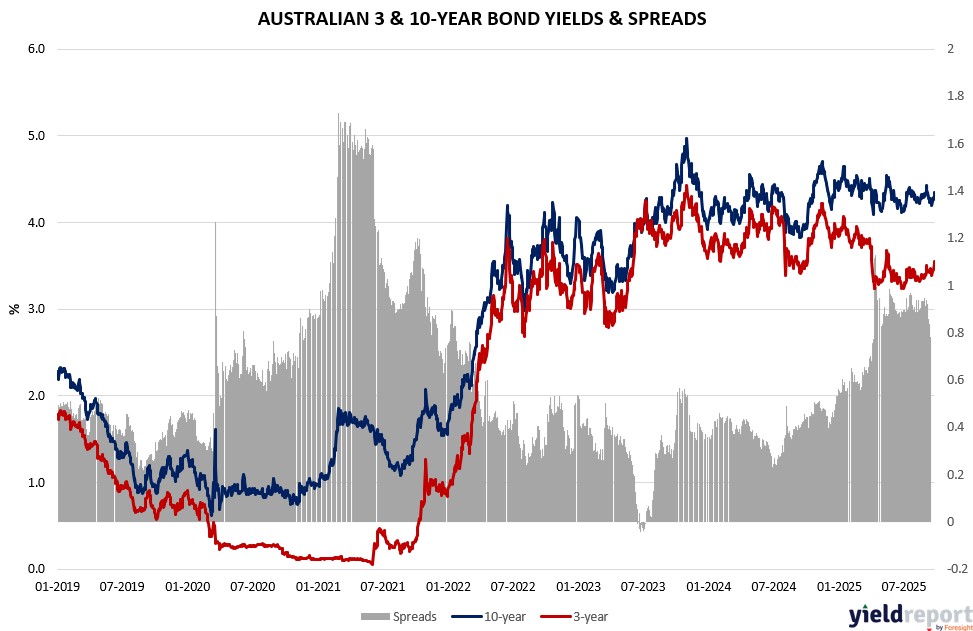

Overview of the Australian Bond Market

Australian government bond yields were little changed on September 25, 2025, stabilizing after CPI-driven surge as markets digest reduced RBA cut odds amid commodity strength. The 2-year yield flat at 3.49%, the 5-year unchanged at 3.77%, the 10-year steady at 4.34%, and the 15-year down 1 basis point to 4.68%.

August CPI rose 3.0% year-on-year, slightly above forecasts, with services remaining sticky despite easing pressures in goods. As a result, swaps now price less than a 50% probability of a cut at the November meeting, down from nearly 70% at the start of the week.

Flash PMI readings also indicated slowing momentum. September’s composite PMI eased to 52.1 from 55.5 in August, with both manufacturing (51.6) and services (52.0) showing cooling expansion. The data suggested growth is moderating while inflation remains above target, leaving policymakers cautious.

The Australian dollar traded at 0.6596 against the US dollar, up slightly on the day but off recent 11-month highs as US yields firmed and global risk appetite softened.

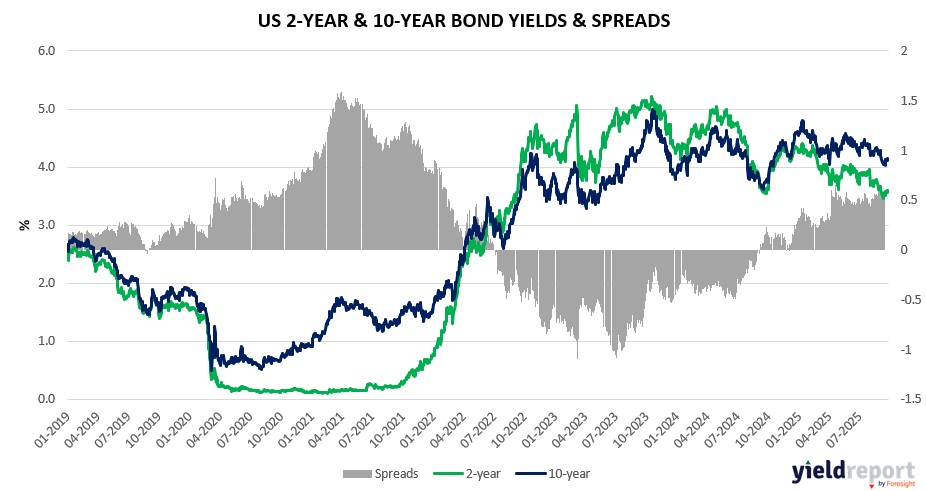

Overview of the US Bond Market

Treasury yields edged higher as investors digested strong growth data and labor market resilience. The two-year yield rose 6bps to 3.66%, while the 10-year climbed to 4.17%. The 30-year was steady at 4.75%. The move reflected a modest paring back of rate-cut bets, though money markets still price in roughly 40bps of easing by year-end following last week’s initial quarter-point cut.

GDP growth was revised upward to 3.8% annualized in Q2, the fastest pace in nearly two years, supported by household spending. Meanwhile, initial jobless claims fell to the lowest level since July, underscoring that while hiring has slowed, layoffs remain limited. Fed officials struck a mixed tone: Governor Miran reiterated the case for faster rate cuts to pre-empt downside risks, while regional presidents cautioned against over-delivering. Markets now await the August core PCE inflation print, expected to show a 0.2% monthly gain and 2.9% annual pace. A higher reading could dampen easing expectations and pressure Treasuries further.