| Close | Previous Close | Change | |

|---|---|---|---|

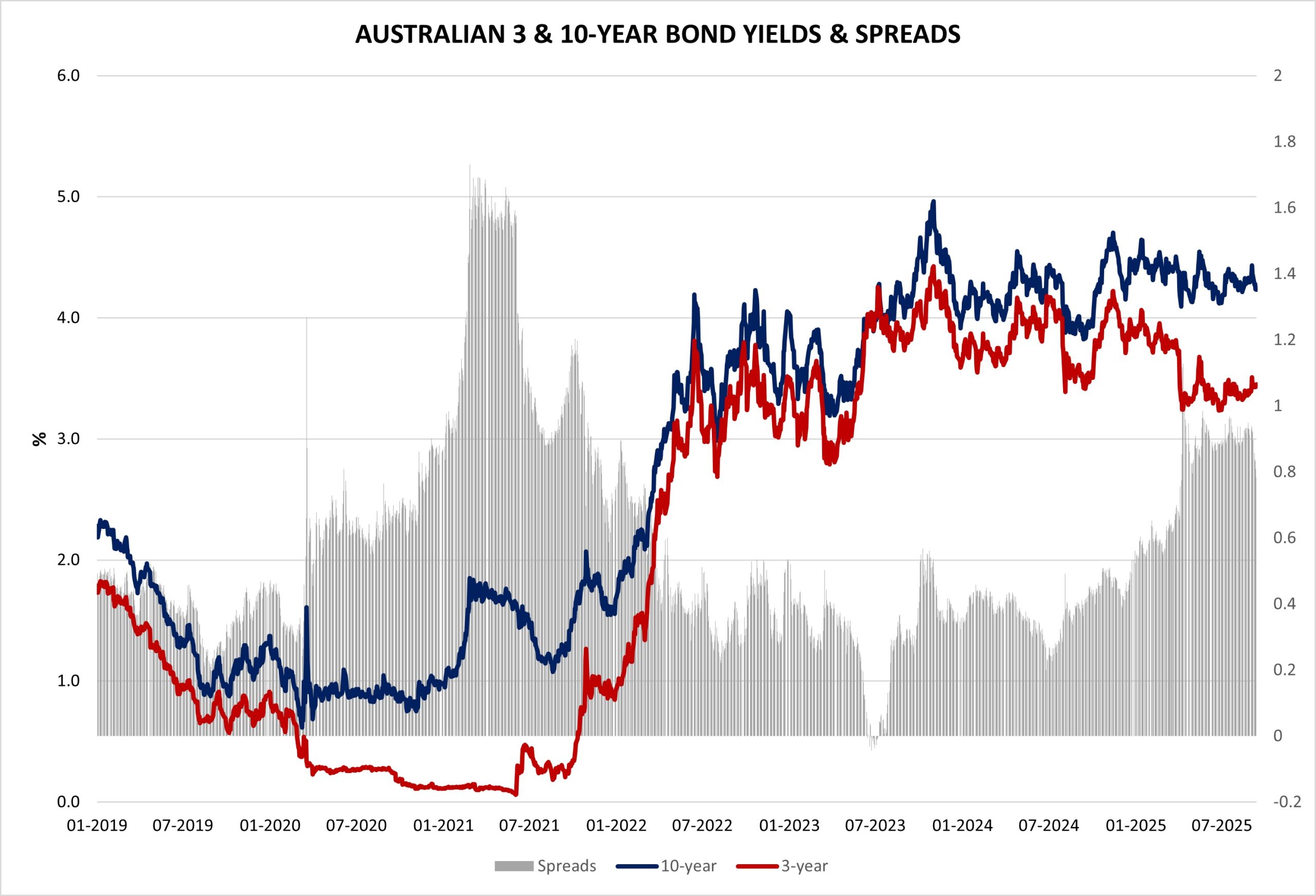

| Australian 3-year bond (%) | 3.45 | 3.429 | 0.021 |

| Australian 10-year bond (%) | 4.23 | 4.238 | -0.008 |

| Australian 30-year bond (%) | 4.94 | 4.957 | -0.017 |

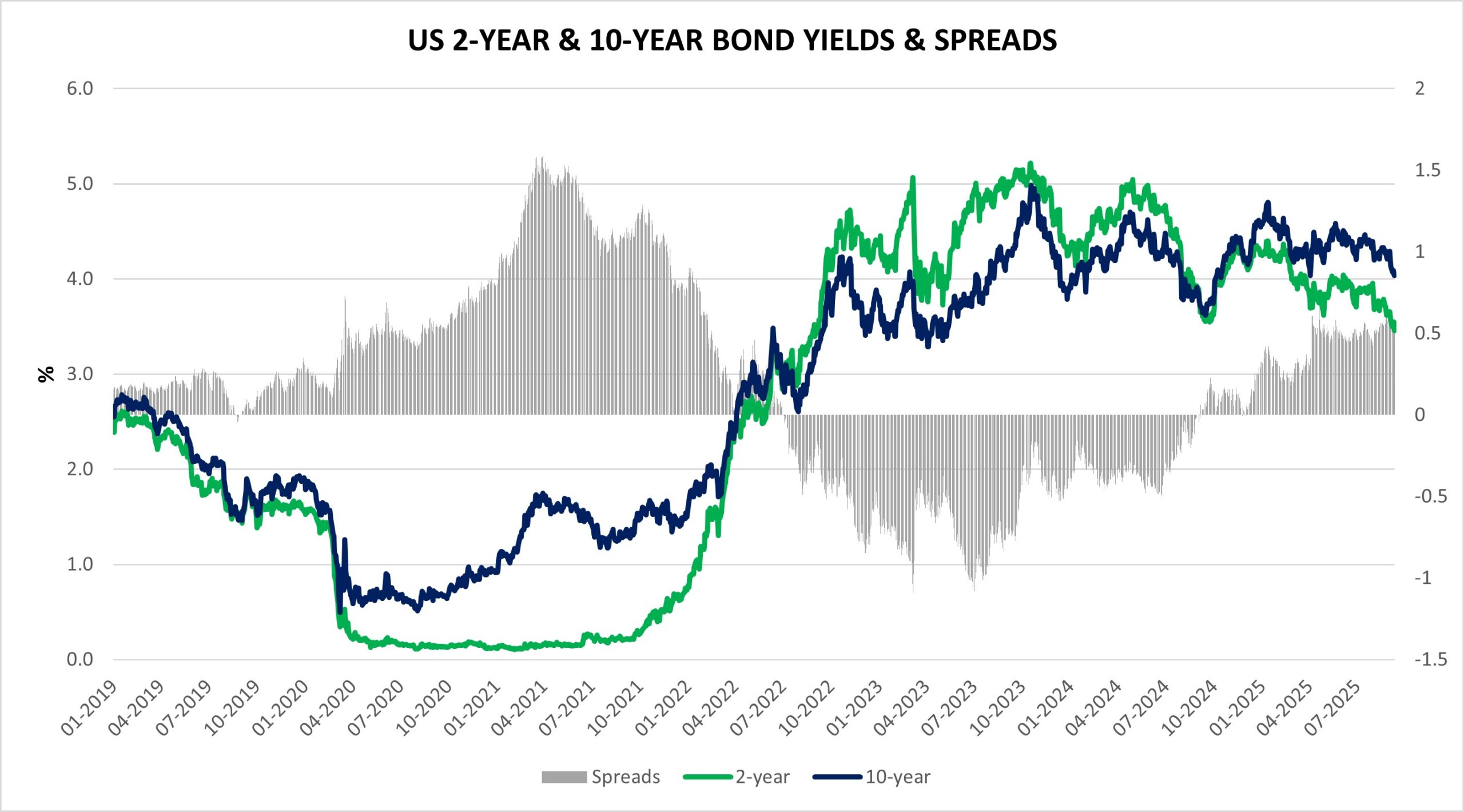

| United States 2-year bond (%) | 3.56 | 3.548 | 0.012 |

| United States 10-year bond (%) | 4.04 | 4.055 | -0.015 |

| United States 30-year bond (%) | 4.66 | 4.7057 | -0.046 |

Overview of the Australian Bond Market

Australian government bond yields mostly rose, with the 2-year up two basis points to 3.37% and the 5-year one basis point to 3.64%, while the 10-year dipped two basis points to 4.21% and the 15-year three to 4.57%. This came amid global yield shifts following US CPI data that met expectations but showed sticky inflation, influencing Reserve Bank of Australia rate outlooks tied to Fed moves.

Local markets benefited from Wall Street’s resilience and commodity rebounds, but energy weakness highlighted oversupply concerns. With US consumer sentiment weaker than expected and jobless claims due next week, economists see synchronized easing supporting Aussie growth, though Beijing’s stimulus signals added tailwinds for resources.

Overview of the US Bond Market

Bond prices slipped as yields rose, with the 10-year Treasury note climbing four basis points to 4.06% from a five-month low, trimming a four-week advance amid consumer data that reinforced bets on Federal Reserve easing. The 2-year yield edged up one basis point to 3.56%, while the 30-year advanced two basis points to 4.68%. This followed August CPI data showing core inflation at 3.1% year-over-year, in line with forecasts, but headline at 2.9% with a hotter-than-expected monthly rise, pulling the Fed in opposite directions between persistent price pressures and a softening job market.

Economists at Comerica Bank highlighted the tension, expecting further cuts but debating the pace. Bloomberg’s survey points to two quarter-point reductions this year, with a sizable group seeing three, as labor cracks prompt action starting next week. Deutsche Bank now forecasts three in 2025, while Morgan Stanley anticipates four consecutive cuts before assessing inflation noise. TD Securities predicts a dovish Fed tone on labor but cautious on inflation, with projections shifting slightly hawkish and reluctance to commit to future moves potentially reversing recent rate momentum.

Bank of America’s Michael Hartnett noted markets view the Fed as ahead of the curve, with rallies in banks and rate-sensitive stocks signaling credible cuts into growth re-acceleration. Cash inflows dominated at $266 billion over four weeks, per EPFR data, while US stocks saw $19 billion outflows. JPMorgan’s Treasury client survey showed net longs shrinking to a two-month low ahead of the Fed meeting, with asset managers paring positions across tenors by $23.5 million per basis point. Leveraged funds reduced shorts in the bond contract.

Dealers expect steady coupon auction sizes for August-October, aligning with April guidance. The IPO surge raised over $4 billion, the busiest since 2021, though year-to-date volume at $28.9 billion lags pre-pandemic averages.