| Close | Previous Close | Change | |

|---|---|---|---|

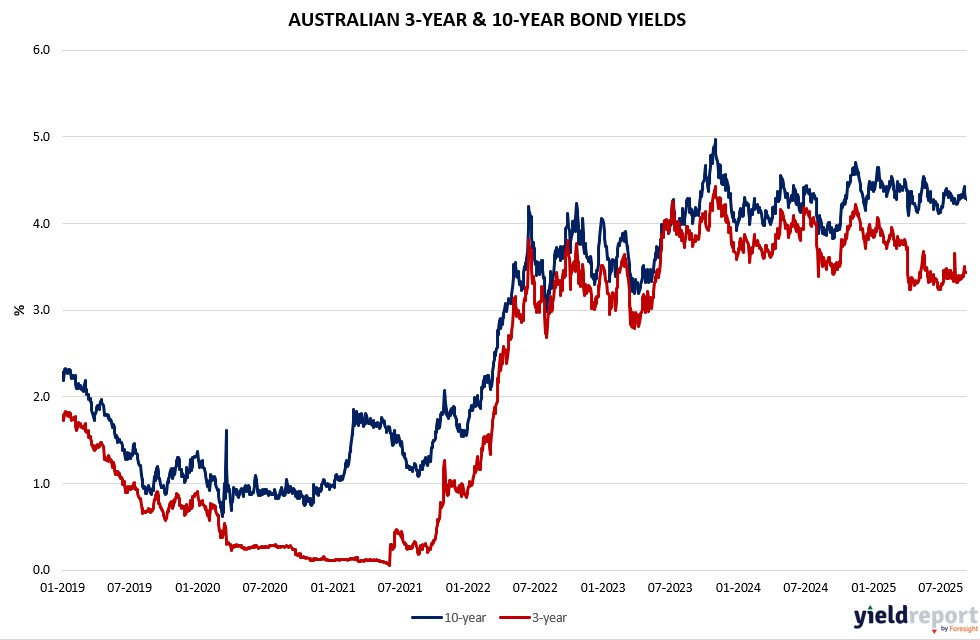

| Australian 3-year bond (%) | 3.429 | 3.447 | -0.018 |

| Australian 10-year bond (%) | 4.238 | 4.28 | -0.042 |

| Australian 30-year bond (%) | 4.957 | 5.001 | -0.044 |

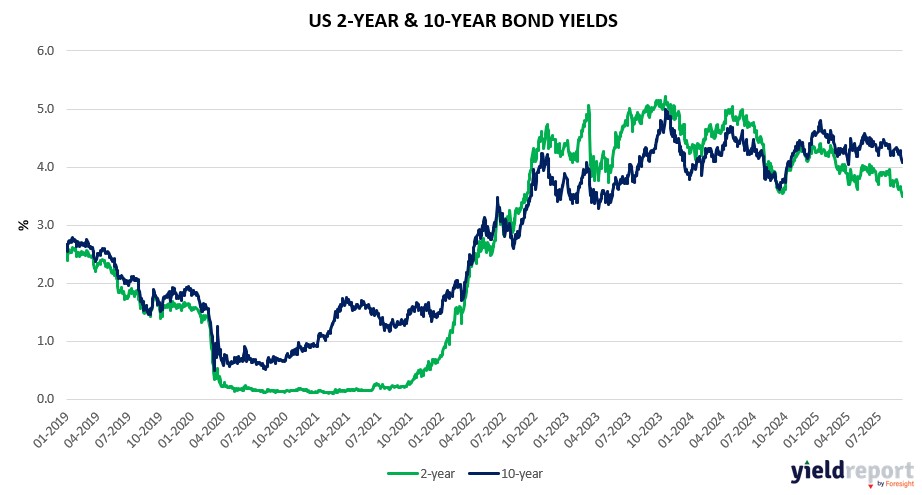

| United States 2-year bond (%) | 3.546 | 3.533 | 0.013 |

| United States 10-year bond (%) | 4.055 | 4.032 | 0.023 |

| United States 30-year bond (%) | 4.705 | 4.677 | 0.028 |

Overview of the Australian Bond Market

Government bond yields declined on September 11, 2025, with the 10-year dropping eight basis points to 4.19%, five-year down four to 3.62%, two-year off one to 3.36%, and 15-year falling eight to 4.56%. The slide to one-month lows reflected anticipation for US CPI and global easing signals, supporting bond proxies like real estate amid AU market consolidation.

Overnight US CPI printed mixed, with headline accelerating 0.4% monthly above 0.3% consensus and 2.9% yearly in line, core steady at 0.3% monthly and 3.1% yearly, while initial jobless claims surged to 263k exceeding 235k estimate, underscoring labor cooling post-record payroll revisions. Despite hotter headline hinting persistent tariff effects, focus shifted to jobs downside, with Fed Chair Jerome Powell likely prioritizing employment mandate. Traders nearly fully priced three 2025 cuts, potentially starting 25 basis points next week, though hotter data tempers 50 basis-point odds.

US Treasuries rallied post-data, 10-year yield dipping below 4% to 4.010% close—lowest since April—two-year down three to 3.51%, extending gains as mixed inflation leaves easing intact. This spillover could ease pressure on RBA, with AU yields tracking lower amid commodity weakness, debt concerns, and tariff volatility. IG’s Tony Sycamore noted holding pattern ahead of central bank flurry and AU jobs, where softening could align RBA with global cuts if inflation moderates.

Positioning data outdated but recent CFTC showed asset managers trimming longs, leveraged paring shorts, signaling caution pre-data. Dealers anticipate steady auction sizes August-October per guidance. Upcoming University of Michigan sentiment September 12 seen at 58, potentially influencing sentiment amid weak seasonality.

Overview of the US Bond Market

In bond markets, the 10-year Treasury yield briefly dipped below 4% for the first time since April before settling at 4.01%. The drop reflected expectations of easier monetary policy, though yields later steadied as traders reassessed the outlook.

Commodities moved in the opposite direction, with oil prices falling as markets weighed OPEC+ plans to raise crude output against geopolitical tensions in the Middle East and Russia.

Overall, the combination of firmer inflation and weakening jobs data has cemented market expectations that the Fed will move to cut rates next week. With equities at record highs and bond yields easing, investors are positioning for a period of looser monetary policy, even as inflation remains above target.

The consumer price index (CPI) showed prices rising 0.4% in August, while core CPI, which strips out food and energy, climbed 0.3%. Both readings remain above the Fed’s 2% target but were tame enough to ease fears of runaway inflation. More impactful for markets was the sharp rise in initial jobless claims, which jumped to 263,000, the highest since late 2021, signaling growing cracks in employment conditions.

The combination of slowing jobs momentum and cooling inflation spurred speculation that the Fed will trim rates by 25 basis points at its meeting next week, with many investors now pricing in multiple cuts before year-end. Treasury yields briefly fell below 4% as bonds rallied, while equities surged to record highs. The S&P 500, Dow Jones, and Nasdaq all closed at fresh peaks, with small caps rising 1.8%. Gold topped its inflation-adjusted 1980 record, although oil and energy shares slipped. Analysts from firms including Morgan Stanley, PIMCO, and Regan Capital largely agreed that the Fed will move cautiously, starting with a modest cut but leaving open the door to further easing.

Fed Chair Jerome Powell had hinted at policy flexibility during the Jackson Hole symposium, and the latest data strengthened the case for a pivot. However, debate continues on the scope of cuts. Some economists believe a larger 50-basis-point move could be discussed, though the Fed is more likely to pursue a gradual path to avoid signaling panic. Others warn that persistent core inflation complicates the picture, raising stagflation risks. While jobless claims are climbing, they remain historically low, and broader economic indicators do not yet suggest imminent recession.

Market strategists framed the dynamic as a shift in emphasis from price stability to maximum employment—the dual mandate’s other pillar. With hiring slowing, policymakers appear more concerned about protecting labor-market health, even if inflation remains sticky. This perspective underpins forecasts from Evercore and others that the Fed could deliver three successive cuts in September, October, and December, recalibrating rates back toward neutral levels.