| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.447 | 3.436 | 0.011 |

| Australian 10-year bond (%) | 4.28 | 4.274 | 0.006 |

| Australian 30-year bond (%) | 5.001 | 4.997 | 0.004 |

| United States 2-year bond (%) | 3.546 | 3.513 | 0.033 |

| United States 10-year bond (%) | 4.089 | 4.072 | 0.017 |

| United States 30-year bond (%) | 4.7419 | 4.7223 | 0.0196 |

Overview of the Australian Bond Market

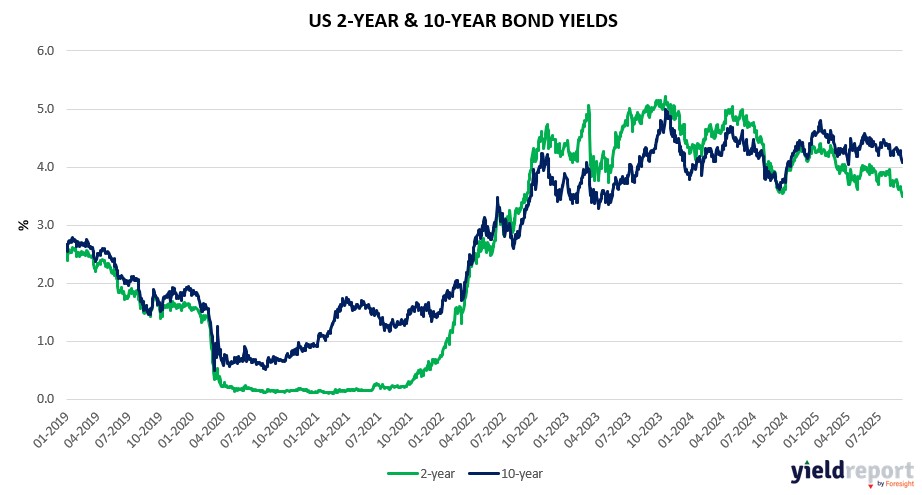

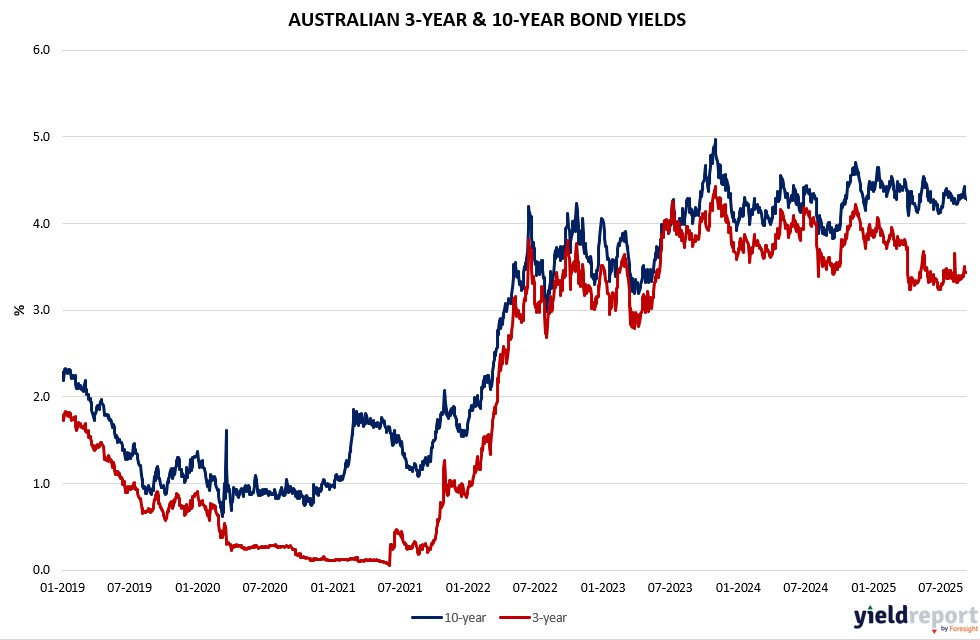

Government bond yields eased on September 10, 2025, tracking US Treasuries lower after benign PPI data reinforced global easing bets amid labor cooling. The 10-year yield fell two basis points to 4.24%, five-year one basis point to 3.64%, two-year unchanged at 3.36%, 15-year down two to 4.61%.

The move reflects spillover from US inflation surprise, easing tariff pass-through concerns and bolstering Fed cut prospects, which could pressure the RBA to follow if domestic data softens. With US jobs revisions signaling weaker global growth, impacting AU commodities, Moomoo’s McCarthy noted potential share market reactions if CPI shows rising inflation amid tanking growth—the S-word scenario.

Upcoming US CPI on September 11, forecast at 0.3% monthly core, could sway RBA views, especially with local miners hit hard. Jobless claims and Michigan sentiment follow, amid AU’s defensive sector tilt toward banks and telcos as fund flows seek safety.

Overview of the US Bond Market

Bond prices climbed on September 10, 2025, driving yields lower after the benign PPI report alleviated inflation worries and bolstered Fed cut bets. The 10-year Treasury yield fell five basis points to 4.05%, the two-year declined two basis points to 3.55%, and the 30-year dropped four basis points to 4.70%. The move reflected relief that tariffs aren’t drastically hitting supply chains, with the PPI drop signaling economic softening but not derailing easing plans.

The unexpected August PPI decline, driven by compressed trade margins reversing July’s spike, underscores slow pass-through from tariffs, as noted by Neil Dutta at Renaissance Macro, allowing firms to absorb costs without aggressive price hikes. This, combined with last week’s weak jobs and record payroll revisions, validates Fed Chair Jerome Powell’s Jackson Hole openness to cuts, with traders nearly fully pricing three reductions in 2025. Scott Helfstein at Global X sees the data as mixed—positive on contained tariffs but hinting at slowdown—likely leading to a modest September cut.

Eric Teal at Comerica Wealth Management said stagnant jobs take precedence, with more cuts ahead despite reduced consumer rate sensitivity. Matthew Weller at Forex.com noted above-target inflation may cap aggressive easing, but a soft CPI could enable 50 basis points. Stephen Brown at Capital Economics anticipates a 25 basis-point cut with possible triple dissent for larger, and a slightly faster easing path in projections.

Positioning showed asset managers trimming long Treasury futures for a second week per recent CFTC data, signaling caution, while leveraged funds pared shorts in longer tenors. Dealers expect steady coupon auction sizes for August-October, per April guidance.

On the docket, core CPI on September 11 is seen at 0.3% monthly, with overall at 0.3%, potentially testing stagflation risks if hotter. Initial jobless claims and University of Michigan sentiment follow on September 11 and 12. Marco Casiraghi at Evercore views PPI as cover for sequential cuts, with Powell sensitive to labor downside. A 22V survey expects in-line CPI on a Fed-friendly path, while options imply a 0.7% S&P swing post-report, below average, per Citigroup’s Stuart Kaiser.