BOND_1.08.25.csv

| Close | Previous Close | Change | |

|---|---|---|---|

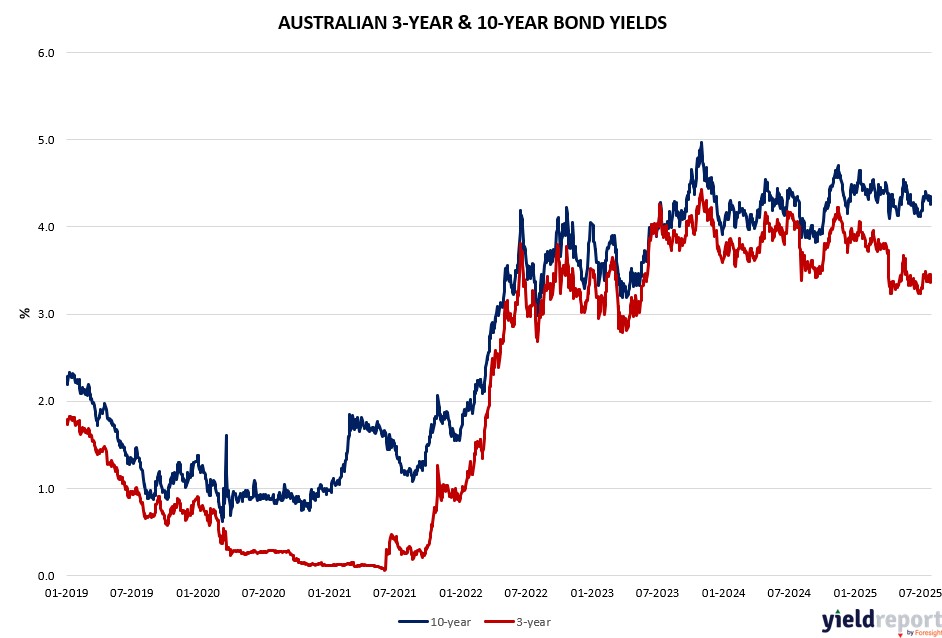

| Australian 3-year bond (%) | 3.434 | 3.392 | 0.042 |

| Australian 10-year bond (%) | 4.321 | 4.274 | 0.047 |

| Australian 30-year bond (%) | 5.027 | 4.972 | 0.055 |

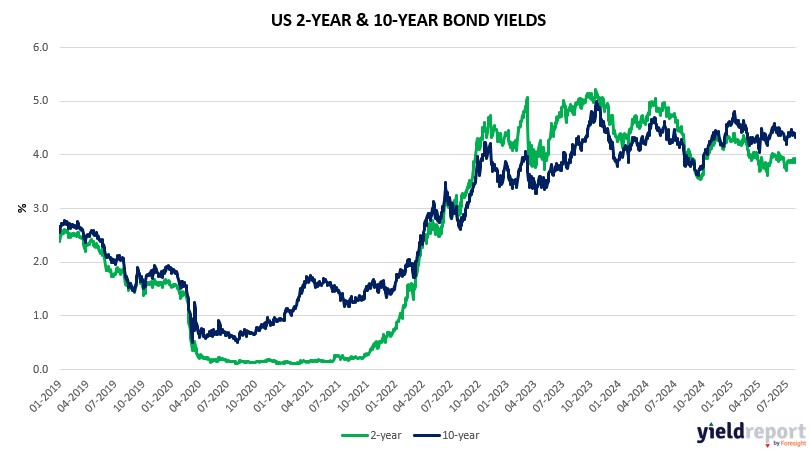

| United States 2-year bond (%) | 3.953 | 3.932 | 0.021 |

| United States 10-year bond (%) | 4.396 | 4.358 | 0.038 |

| United States 30-year bond (%) | 4.9327 | 4.8847 | 0.048 |

Overview of the Australian Bond Market

Australian government bond yields ticked higher on August 1, 2025, reflecting global risk-off sentiment and fading hopes for aggressive global rate cuts. The Australia 2-Year Bond Yield rose 4 basis points to 3.39%, the 5-Year Yield increased 5 basis points to 3.71%, the 10-Year Yield climbed 6 basis points to 4.31%, and the 15-Year Yield also raised 6 basis points to 4.67%.

The yield uptick followed Wednesday’s robust Australian data, including Building Approvals (+11.9% vs. 2% expected) and Retail Sales (+1.2% vs. 0.4% expected), which signalled economic resilience and tempered expectations for an imminent RBA rate cut. While the Q2 CPI of 2.1% and Trimmed Mean CPI of 2.7% still support an August cut, markets now price in a more cautious RBA stance. Globally, higher-than-expected US inflation (Core PCE YY at 2.8%) and a weak non-farm payrolls report (73,000 vs. 110,000 expected) reduced bets on a Federal Reserve rate cut in September, pushing up global yields and pressuring Australian bond prices.

US tariff threats, including higher levies on over 60 countries but sparing Australia, added inflationary risks, limiting bond demand. Bond traders slightly increased net short positions in 10-year and 15-year tenors, reflecting caution ahead of the RBA’s August meeting. The Australian Treasury is expected to maintain steady auction sizes for August-October, signalling stable debt issuance. Strategists from Morgan Stanley and UBS suggest yields may remain elevated if global trade tensions persist, though Australia’s economic fundamentals provide a buffer.

Overview of the US Bond Market

U.S. Treasury yields tumbled in response to a significantly weaker-than-expected July jobs report, intensifying market pressure on the Federal Reserve to begin cutting interest rates. Nonfarm payrolls rose by just 73,000 jobs, well below the 100,000 forecasts, while previous figures were drastically revised down: May’s gain was slashed to 19,000 (from 144,000) and June’s to 14,000 (from 147,000). Unemployment ticked up to 4.2%, further signalling softening labour market conditions.

These developments triggered the largest one-day fall in Treasury yields this year. The 2-year yield plunged 25 basis points to 3.702%, its biggest drop in over 12 months. The 10-year yield fell 14.2 basis points to 4.218%, the sharpest daily decline since April. Both maturities posted significant weekly losses, with the 10-year down 16.7 basis points on the week. The WSJ Dollar Index also dropped 0.7%, reflecting broad investor expectations for monetary easing.

Before the data release, some Fed governors (notably Waller and Bowman) had already expressed concern over labour market weakness. Their views gained traction after the jobs data confirmed deterioration. President Trump’s reaction was politically charged, threatening to fire BLS head Erika McEntarfer, accusing her of manipulating job figures—a move that could stoke further institutional uncertainty.

Despite earlier expectations of a resilient labour market—especially amid inflation risks and rising tariffs—bond markets rapidly repriced Fed expectations. The report overshadowed recent tariff news, including Trump’s new import duties (15% on South Korea, 50% on Brazil), and diminished investor confidence in near-term U.S. economic strength.

Looking ahead, next week is light on economic data and Fed commentary, giving markets room to digest these developments. The sharp move in yields signals a possible pivot in Fed policy path, with markets increasingly pricing in a September rate cut despite lingering inflation pressures.

The U.S. Treasury announced steady auction sizes from August through October with $58B in 3-year notes, $42B in 10 year, and $25B in 30-year bonds—aligned with expectations. It also expanded TIPS and T-bill issuance, and is doubling long-end buybacks to a quarterly maximum of $38B, aiming to support liquidity.

Analysts and forecasters now warn GDP growth may decelerate significantly—EY and BNP Paribas expect growth to slow to between 1–1.5% in 2025, with downside risks including tariffs, softer labour conditions, and weaker consumer spending.

In short: this week’s labour weakness, renewed trade tensions, and political turbulence collectively pushed markets toward recession fears, raised rate-cut odds, and underscored hardening headwinds for U.S. growth.