| Close | Previous Close | Change | |

|---|---|---|---|

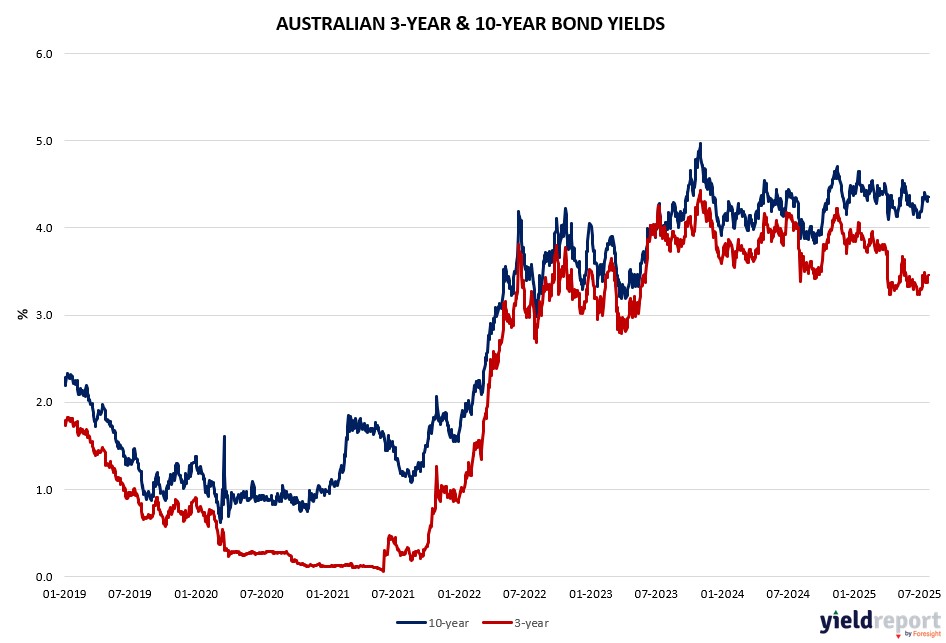

| Australian 3-year bond (%) | 3.454 | 3.455 | -0.001 |

| Australian 10-year bond (%) | 4.35 | 4.355 | -0.005 |

| Australian 30-year bond (%) | 5.506 | 5.064 | 0.442 |

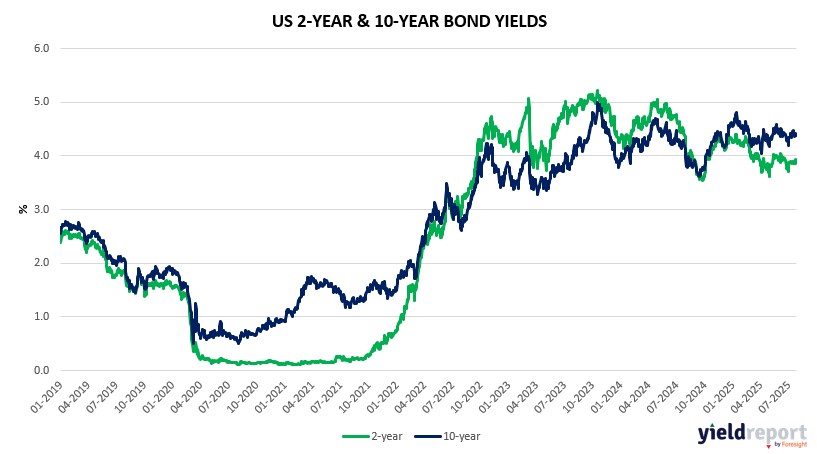

| United States 2-year bond (%) | 3.917 | 3.925 | -0.008 |

| United States 10-year bond (%) | 4.38 | 4.412 | -0.032 |

| United States 30-year bond (%) | 4.9235 | 4.9543 | -0.0308 |

Overview of the Australian Bond Market

Australian 10-year Treasuries dipped slightly as markets awaited key inflation data, with the yield falling 1 basis point to 4.34%. The 2-year yield eased 2 basis points to 3.40%, while the 5-year yield dropped 2 basis points to 3.72%. The 15-year yield held steady at 4.70%, reflecting a flat yield curve amid cautious sentiment.

Yields have risen over the past month, with the 10-year up 21 basis points, supported by solid PMI data (composite 53.6) but tempered by a -0.03% leading index. The RBA’s gradual rate-cut path, targeting 3.00% by mid-2026 with an 85-basis point reduction, remains in focus. The AUD’s 0.25% drop to 0.655 signals commodity weakness and tariff uncertainty.

Interest-rate swaps show a slight flattening, with yields reacting to global trade tensions, including Trump’s 15-20% tariff threats. Tomorrow’s CPI and US consumer confidence will be critical, alongside the August 1 deadline. The market balances domestic resilience with global risks, with focus on RBA’s trimmed mean CPI (expected 0.7% quarterly, 2.7% yearly).

Overview of the US Bond Market

The start of a week that will set the tone for the rest of the year in markets saw a dollar gauge up nearly 1%. The euro slid the most in over two months. US Treasuries barely budged amid mixed results from US debt sales.

The Treasury jacked up its estimate for federal borrowing for the current quarter to $1 trillion, mainly due to distortions from the debt limit. On Wednesday, the department will announce its plans for note and bond sales over coming months — which dealers widely seen as staying unchanged.

In the run-up to the Aug. 1 US tariff deadline, investors are focused on a raft of key data from jobs to inflation and economic activity. The big news comes Wednesday, when the Federal Reserve is expected to keep rates unchanged.

US and Chinese officials finished the first of two days of talks aimed at extending their tariff truce beyond a mid-August deadline and hashing out ways to maintain trade ties while safeguarding economic security. Canada Prime Minister Mark Carney said his government is still deep in trade talks with the Trump administration.