| Close | Previous Close | Change | |

|---|---|---|---|

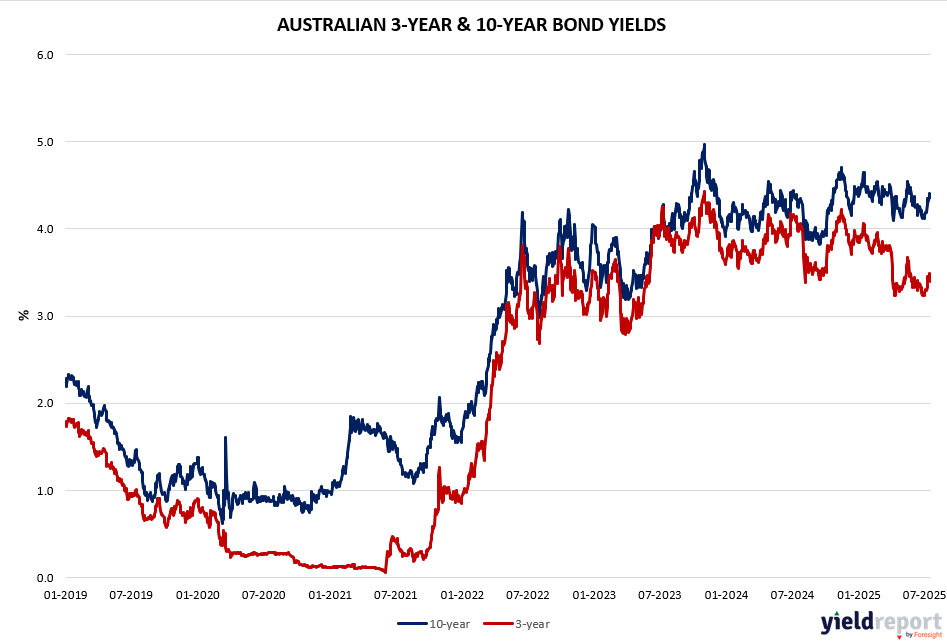

| Australian 3-year bond (%) | 3.396 | 3.486 | -0.09 |

| Australian 10-year bond (%) | 4.357 | 4.405 | -0.048 |

| Australian 30-year bond (%) | 5.031 | 5.065 | -0.034 |

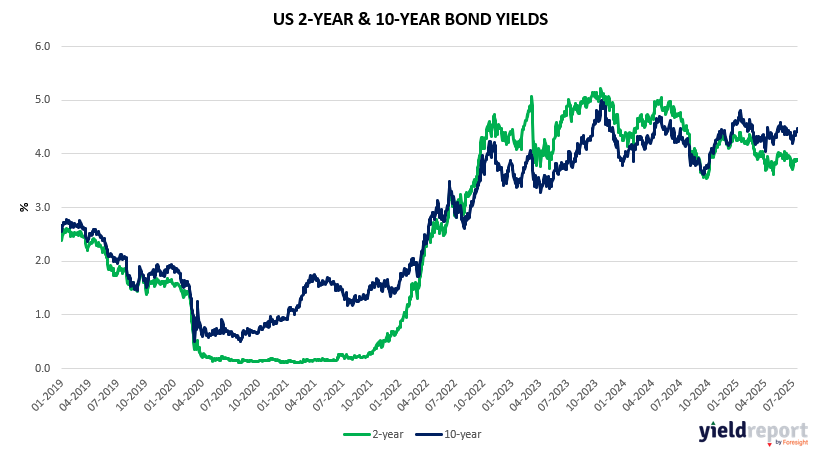

| United States 2-year bond (%) | 3.905 | 3.885 | 0.02 |

| United States 10-year bond (%) | 4.467 | 4.455 | 0.012 |

| United States 30-year bond (%) | 5.0271 | 5.015 | 0.0121 |

Overview of the Australian Bond Market

Australian government bond yields fell on Thursday, July 17, 2025, with the 10-year yield dropping 7 basis points to 4.32%, and the 2-year yield declining 12 basis points to 3.32%, driven by soft employment data signaling potential RBA easing. The 15-year yield eased 5 basis points to 4.67%.

Yesterday’s labor market report, with unemployment at 4.3% and only 2,000 jobs added, has pushed August rate cut probability to 94%, with 75-100 basis points of cuts priced over the next year, targeting 2.85%-3.10% by mid-2026. Albanese’s China visit supports trade hopes, but the AUD’s 0.64% drop reflects tariff and data pressures. US retail strength and tomorrow’s housing starts could influence global yields, impacting local bonds.

Overview of the US Bond Market

US Treasury yields edged higher on Thursday, July 17, 2025, with the 10-year note up 6 basis points to 4.45%, reflecting optimism from today’s strong retail sales and Philly Fed data, though tempered by tariff risks. The 2-year yield dipped 5 basis points to 3.90%, while the 30-year yield rose 12 basis points to 5.01%, steepening the curve.

Yesterday’s import price decline to -0.2% year-over-year and today’s retail sales surge to 0.6% suggest easing inflation, supporting a September rate cut outlook, with two cuts expected by year-end. However, Trump’s tariffs could reverse this, keeping yields elevated. Tomorrow’s housing starts data will test this balance, alongside ongoing bank capital relief proposals boosting bond demand.