| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.486 | 3.469 | 0.017 |

| Australian 10-year bond (%) | 4.405 | 4.383 | 0.022 |

| Australian 30-year bond (%) | 5.065 | 5.067 | -0.002 |

| United States 2-year bond (%) | 3.885 | 3.9 | -0.015 |

| United States 10-year bond (%) | 4.455 | 4.417 | 0.038 |

| United States 30-year bond (%) | 5.015 | 4.9574 | 0.0576 |

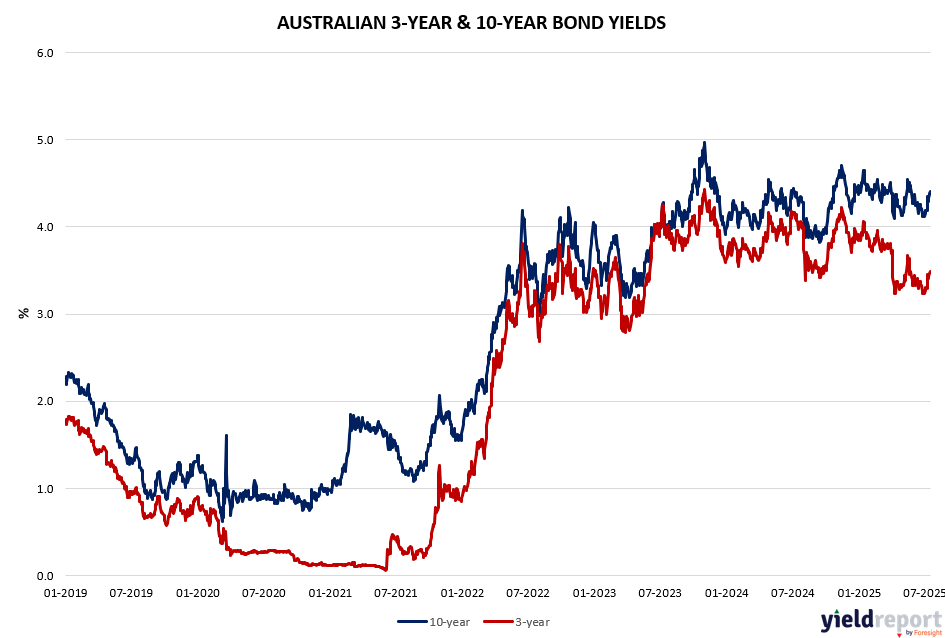

Overview of the Australian Bond Market

Australian government bond yields edged up on Wednesday, July 16, 2025, with the 10-year yield rising 1 basis point to 4.38% and the 15-year yield steady at 4.72%. The 2-year yield dipped 1 basis point to 3.42%, reflecting a cautious market ahead of today’s employment data.

The RBA’s recent hold at 3.85% on July 8-9 has shifted rate cut expectations to August, with markets pricing 75-100 basis points of cuts over the next year, targeting 2.85%-3.10% by mid-2026, influenced by yesterday’s US CPI and local economic signals. Albanese’s China visit offers trade hope, but tariff risks persist. Today’s employment figures—expected at 20,000 jobs added versus -2,500 prior—could sway sentiment, with the AUD’s 0.21% gain to 0.6527 reflecting cautious optimism.

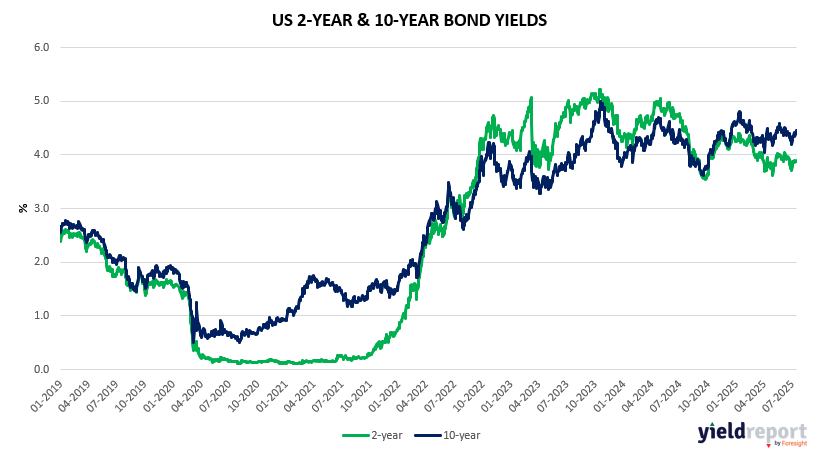

Overview of the US Bond Market

US Treasury yields ticked higher on Wednesday, July 16, 2025, with the 10-year note up 1 basis point to 4.46%, reflecting a muted reaction to yesterday’s CPI data. The 2-year yield fell 7 basis points to 3.89%, while the 30-year yield rose 6 basis points to 5.01%, steepening the yield curve as markets adjust to inflation trends.

Yesterday’s CPI, with a core MM rise of 0.2% against 0.3% expected, has reinforced a cautious Fed stance, with September rate cut odds rising. Today’s industrial production and Philly Fed Index will provide further clues. Trump’s tariff threats continue to fuel inflation concerns, while the proposed bank capital relief could support bond demand, keeping yields in focus amid mixed economic signals.