| Close | Previous Close | Change | |

|---|---|---|---|

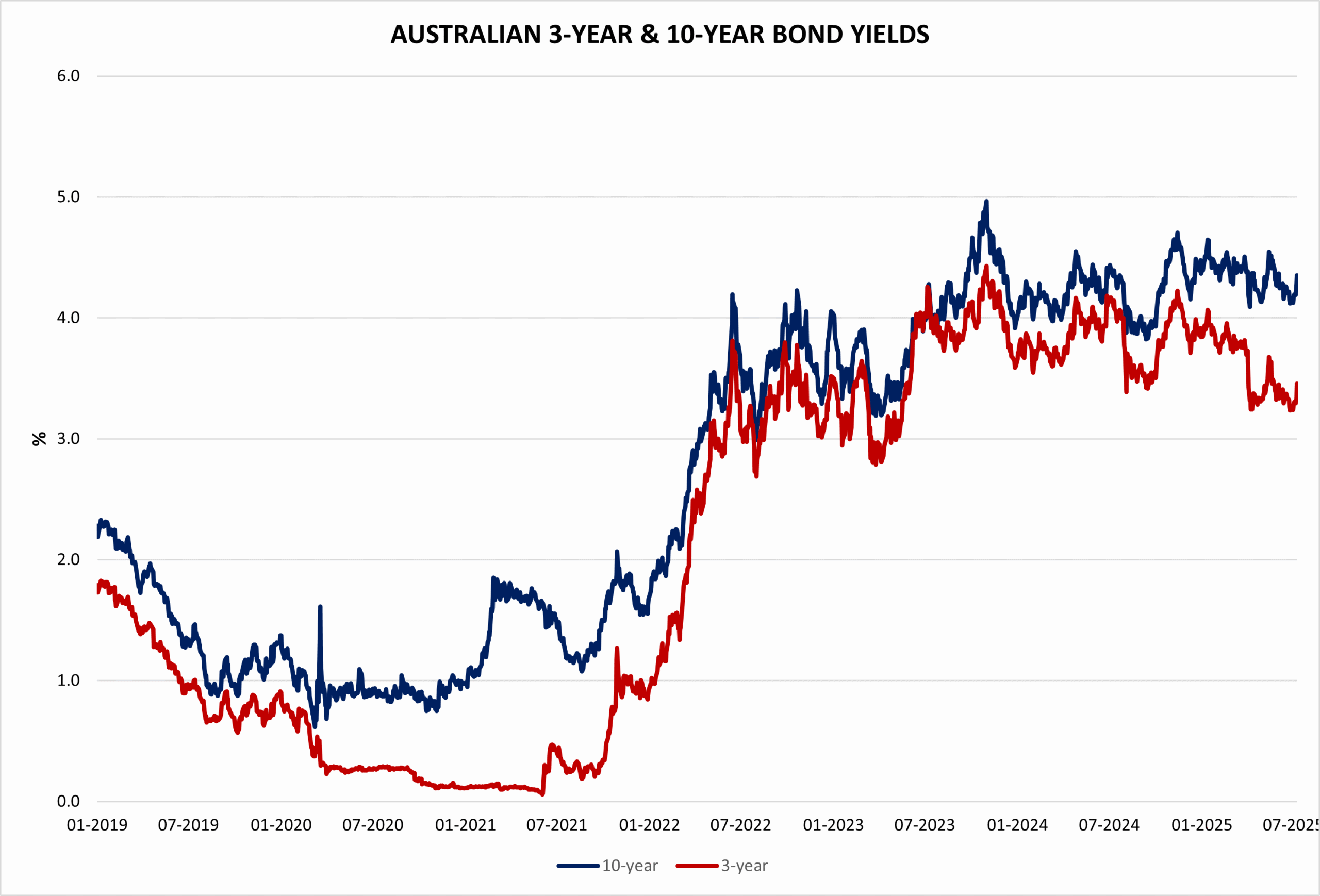

| Australian 3-year bond (%) | 3.459 | 3.467 | -0.008 |

| Australian 10-year bond (%) | 4.367 | 4.377 | -0.010 |

| Australian 30-year bond (%) | 5.044 | 5.050 | -0.006 |

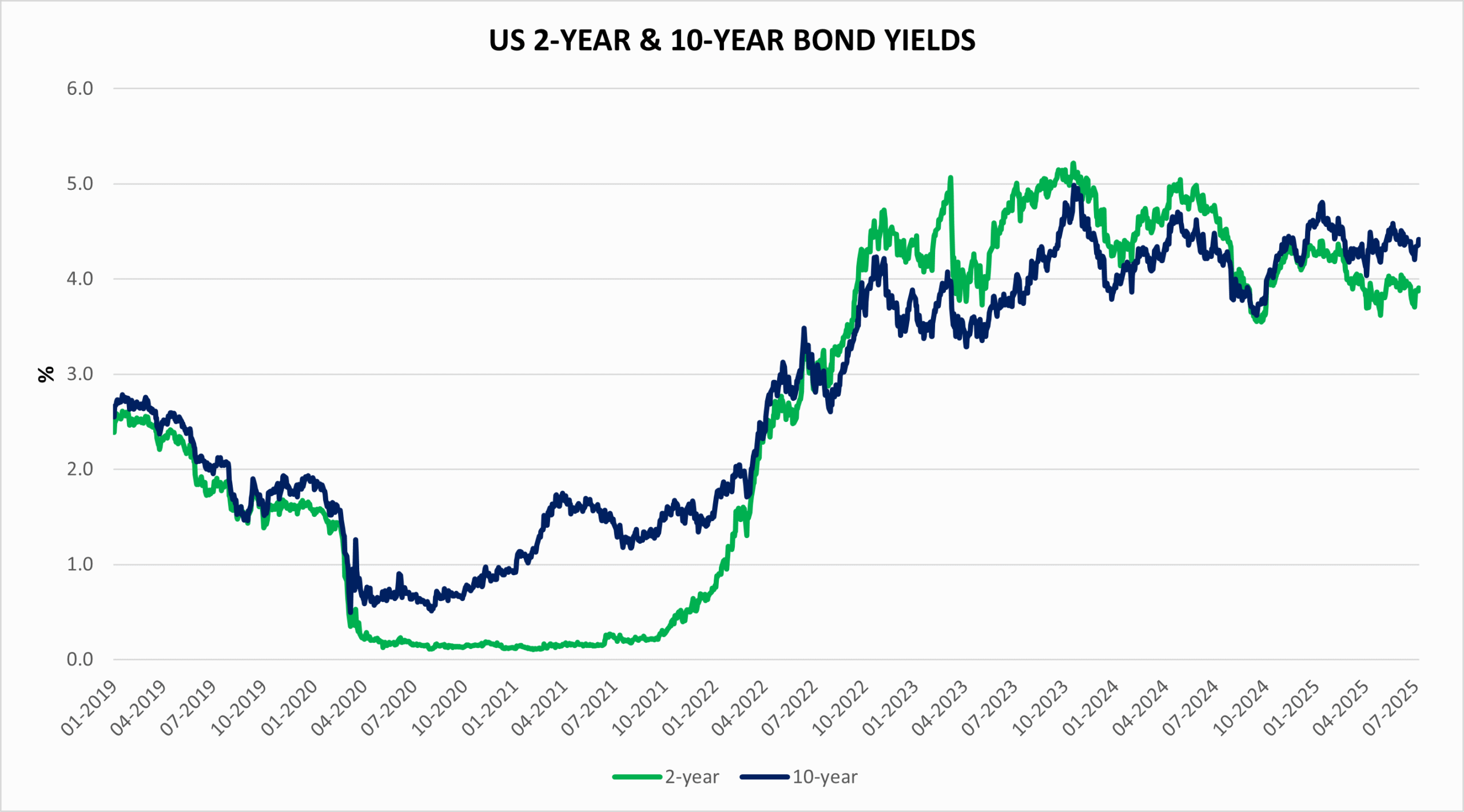

| United States 2-year bond (%) | 3.900 | 3.898 | 0.002 |

| United States 10-year bond (%) | 4.429 | 4.427 | 0.002 |

| United States 30-year bond (%) | 4.973 | 4.973 | 0.000 |

Overview of the Australian Bond Market

Australian government bond yields rose modestly on Monday, July 14, 2025, with the 10-year yield up 3 basis points to 4.35% and the 15-year yield increasing 4 basis points to 4.70%. The 2-year yield ticked up 1 basis point to 3.41%, reflecting a stable yet cautious market following the RBA’s decision to hold the cash rate at 3.85% on July 8-9, 2025.

The tariff threat from Trump’s 30% tariff announcement on EU and Mexico goods, effective August 1, has introduced uncertainty, potentially influencing inflation forecasts.

Markets have adjusted expectations post-decision, now pricing in around 75-100 basis points of cuts over the next 12 months, targeting a cash rate near 2.85%-3.10% by mid-2026, though today’s US CPI data—due at 10:30 PM AEST and expected to show a 2.7% year-over-year rate—could prompt further recalibration. The AUD’s 0.23% decline to 0.6562 adds pressure, with traders now focused on the CPI outcome and its global trade implications.

Overview of the US Bond Market

US Treasury yields edged higher on Monday, July 14, 2025, with the 10-year note rising 3 basis points to 4.43%, reflecting cautious optimism ahead of Tuesday’s CPI data. The 2-year yield dipped 5 basis points to 3.90%, while the 30-year yield climbed 8 basis points to 4.98%, signaling mixed expectations for future rate adjustments. The yield curve steepened slightly, with short-term rates softening amid tariff uncertainty.

The focus remains on Tuesday’s CPI release, which could shift Fed rate cut probabilities. Current market pricing leans toward two cuts by year-end, with September favored over July, though a higher-than-expected CPI could delay easing. Trump’s tariff threats continue to stir debate, with potential inflationary pressures keeping Fed Chair Jerome Powell’s recent cautious stance in the spotlight.