| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,474.46 | 185.13 | 0.39% |

| S&P 500 | 6,829.37 | 16.74 | 0.25% |

| Nasdaq | 23,413.67 | 137.75 | 0.59% |

| VIX | 16.59 | -0.65 | -3.77% |

| Gold | 4,245.40 | 24.6 | 0.58% |

| Oil | 58.65 | 0.01 | 0.02% |

OVERVIEW OF THE US MARKET

Wall Street ended modestly higher on December 2, 2025, with major indexes posting gains amid a rebound in cryptocurrencies and cautious optimism ahead of key economic data releases. The S&P 500 climbed 0.25% to close at 6,829.37, marking its sixth advance in seven sessions, though breadth remained narrow as most components declined. The Nasdaq Composite rose 0.59% to 23,413.67, buoyed by technology stocks, while the Dow Jones Industrial Average added 0.39% to 47,474.46. Gains were led by mega caps like Apple and NVIDIA, with the latter seeing heavy volume of 182 million shares traded, up 0.86% to $181.46. Intel surged 8.65% on positive developments, but Tesla slipped amid valuation concerns from investor Michael Burry. Boeing jumped 10% after forecasting a return to positive cash flow in 2026, while Warner Brothers Discovery and Philip Morris also featured among notable movers.

Sector performance was mixed, with Information Technology up 0.84% and Industrials gaining 0.87%, reflecting ongoing enthusiasm for AI and manufacturing resilience. Energy fell 1.28% on volatile oil prices tied to Russia-Ukraine talks, and Health Care dropped 0.58%. Active stocks highlighted speculative fervor, including Polyrizon Ltd. soaring 131.96% on high volume and Bitfarms Ltd. down 5.49%. Bitcoin’s rebound above $92,000 after a sharp selloff provided a lift to risk assets, erasing some of the $1 billion in leveraged bets wiped out earlier.

Investors are navigating a fragile year-end environment, balancing tight equity ranges with Fed policy uncertainty. President Donald Trump announced plans to name a new Fed chair in early 2026, with Kevin Hassett emerging as a frontrunner, potentially signalling a dovish shift. This fuelled bets for more rate cuts, with money markets pricing nearly four quarter-point reductions over the next year, including one at the December 10 meeting. Fed officials show widening disagreement on terminal rates, the most since 2012, amid debates over a “hawkish cut” next week possibly drawing dissents.

Strategists remain constructive for December, expecting back-and-forth patterns before new highs, per Fundstrat’s Mark Newton. Morgan Stanley’s CIO sees the S&P 500 reaching 7,800 in 2026 on earnings growth, while 22V Research highlights AI capex and consumer spending as supports. However, concerns linger over crypto volatility and Strategy Inc.’s plunge, with its leveraged ETFs down over 80% this year, underscoring leverage risks. Upcoming data like November ISM Manufacturing PMI (poll: 49) and jobless claims could sway sentiment, as traders reassess global rally momentum.

OVERVIEW OF THE AUSTRALIAN MARKET

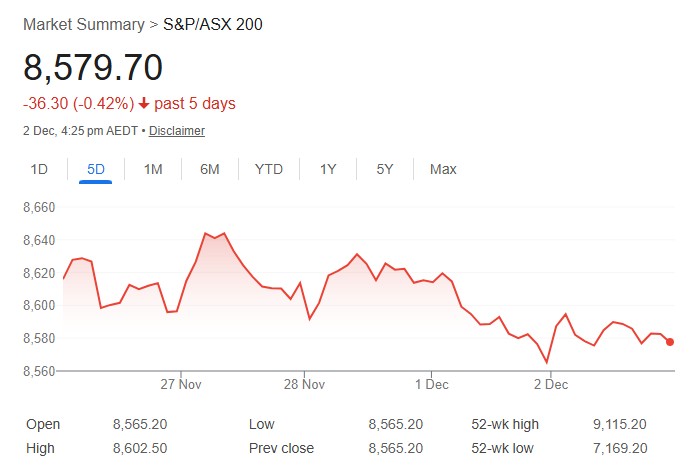

The S&P/ASX 200 closed up 0.17% at 8,579.7 on December 2, 2025, grinding out a modest gain in a lackluster session amid mixed global cues and rising bond yields. The All Ordinaries rose 0.13% to 8,877.5, with advancers edging decliners 144 to 129. Energy led gains at 1.08%, buoyed by coal sector strength, while Materials added 0.74% on commodity resilience. Coronado Global Resources climbed 7.1% and Stanmore Resources 3.9% amid broader coal firmness. Consumer Staples rose 0.46% and Real Estate 0.43%, but Information Technology plunged 1.55%, dragging the All Tech index down 1.12%. Health Care was flat, Financials unchanged, and Utilities fell 0.41%.

High P/E stocks faced pressure from elevated risk-free rates, which have risen since July on doubts over RBA easing, spiking post-September CPI. This hurts growth-oriented sectors like tech, where future earnings are discounted more heavily, and favors commodities with near-term margins. African Gold surged 66.7%, Mayfield Group 10.3% on SPP results, and Turaco Gold 7.4% on drilling updates. Kingsgate Consolidated gained 4.8% and Select Harvests 4.4%, aligning with uptrends. On the downside, Pantoro Gold dropped 11.9% on share sales, Resolution Minerals 11.8% despite gold intercepts, and Minerals 260 10.8% post-resource double.

October building approvals fell 6.4% MM, worse than -4.3% forecast, signaling construction weakness, while Q3 current account deficit hit A$16.6B and net exports contributed 0.1%. Q3 GDP due tomorrow (poll: +0.7% QQ, +2.2% YY) is critical, with RBA Governor Bullock testifying today. Consumer confidence is rising, but inflation at 3.3% in October exceeds the 2-3% target, suspending easing; economists now eye hikes late 2026.

Futures point to cautious Asian opens, with Nikkei up 0.6%, Hang Seng down 0.5%, and ASX 200 up 0.2%. AUD/USD rose 0.13% to 0.6552 on firm yields and Fed cut bets. Strategists see resource stocks benefiting from inflation-hedge rotations, while bond proxies like banks lag.