| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,987.10 | 74.8 | 0.16% |

| S&P 500 | 6,728.80 | 8.48 | 0.13% |

| Nasdaq | 23,004.54 | -49.46 | -0.21% |

| VIX | 18.62 | -0.46 | -2.41% |

| Gold | 4,084.90 | 75.1 | 1.87% |

| Oil | 60.36 | 0.61 | 1.02% |

OVERVIEW OF THE US MARKET

Wall Street rallied sharply on November 10, 2025, fueled by optimism that the US government shutdown is nearing an end after the Senate advanced a bipartisan deal, potentially restoring economic data flows and easing headwinds. The S&P 500 climbed 1.5% to 6,832.43, its best day since May, while the Nasdaq Composite surged 2.3% to 23,527.17, led by AI rebound with Nvidia up 5.8%. The Dow Jones Industrial Average rose 0.8% to 47,368.63. Tech megacaps drove gains, with Information Technology up 2.7%, Communication Services 2.5%, and the Magnificent 7 jumping 2.8%, snapping recent weakness amid AI valuation doubts.

President Trump’s support for the deal, funding parts through Jan. 30 and banning layoffs, boosted sentiment, as City Index’s Fiona Cincotta noted it would clarify Fed policy via data resumption. Markets priced 60% odds for a December cut, down from mid-October but stable. Fed speakers mixed: St. Louis’s Alberto Musalem urged caution on easing amid resilience, San Francisco’s Mary Daly warned of high rates risking demand, and Governor Stephen Miran backed a cut on inflation/jobs balance.

Corporate highlights: TSMC slowed revenue growth amid AI sustainability debates, Instacart beat on orders, Tyson flat on profits amid beef losses. Health insurers slid as deal omitted ACA subsidies extension. Crypto rose, Bitcoin up 1.2% to $105,759, reversing weekly slump.

Broader context: Carson’s Sonu Varghese saw shutdown end removing risks, Deutsche’s Jim Reid eyed quick September jobs release post-reopen. Evercore’s Krishna Guha noted data aiding soft labor view for cuts. Morgan Stanley’s Michael Gapen anticipated 1-2 week delays on inflation/spending. UBS’s Ulrike Hoffmann-Burchardi expected bipartisan relief pre-Thanksgiving. Nationwide’s Mark Hackett viewed dip as froth purge, HSBC’s Max Kettner bullish on equities beyond tech into cyclicals. Oppenheimer’s John Stoltzfus dismissed AI give-up early. Q3 earnings grew 14.6%, doubling expectations, with upgrades near April highs per Bloomberg Intelligence, supporting 2026 outlook despite labor fragility.

OVERVIEW OF THE AUSTRALIAN MARKET

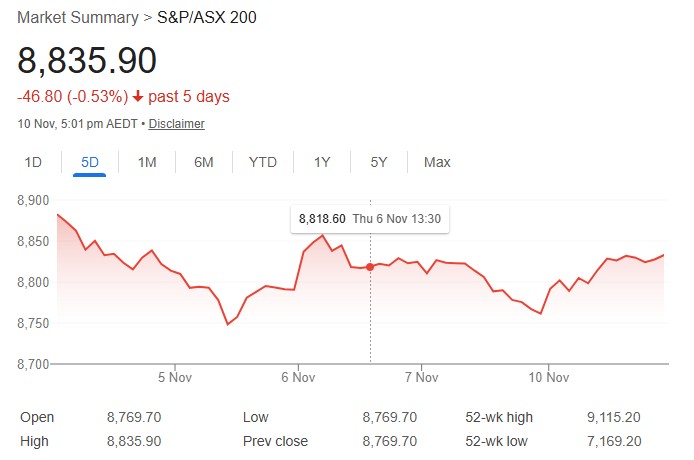

The Australian share market advanced on November 10, 2025, its best session in three weeks, buoyed by US shutdown deal hopes lifting global risk and tech rebound. The S&P/ASX 200 rose 0.8% to 8,835.9, All Ordinaries up 0.9% to 9,109.4. Tech surged 2.4% tracking Nasdaq futures, with WiseTech up 6%, Iress 6.6% on efficiency plan. Materials gained 1.6%, Energy 1.5% on China outlook upgrade by Goldman, oil uptick.

Critical minerals led: Liontown, Pilbara up over 9.5%, Lynas 4.8%. Uranium strong: Paladin, Deep Yellow, Silex up 7.9-9.6%. Gold miners rose as spot hit US$4,069/oz. Financials up 0.6%, ANZ surged 3.2% to record $39.52 despite 10% profit drop to $5.9B, Macquarie up 0.6%. Industrials +0.9%: Qantas rebound, Monadelphous 11% on contracts.

IG’s Tony Sycamore noted abated headwinds, though AI questions linger. AUD/USD up 0.5% to 0.6528 on risk-on.

Defensives lagged: Consumer Staples down 0.4% (Coles, Woolies lower), Real Estate -0.2%. Laggards: Brainchip -7.7% on placement, Alliance Aviation -7.6% on guidance reaction.

RBA’s Hauser cautious on growth/inflation. Westpac sentiment Tuesday. IG: AI marks not washed quickly. AFR: ANZ jump drove gains. Fool: SPI up 0.45% Tuesday. HSBC/MS/UBS bullish long-term on earnings/AI/tariffs, but shutdown resolution tempers prior drags.