| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,427.12 | 314.67 | 0.67% |

| S&P 500 | 6,812.61 | 46.73 | 0.69% |

| Nasdaq | 23,214.69 | 189.1 | 0.82% |

| VIX | 17.42 | 0.23 | 1.34% |

| Gold | 4,221.30 | 19 | 0.45% |

| Oil | 59.08 | 0.43 | 0.73% |

OVERVIEW OF THE US MARKET

US equities extended their rally on November 28, 2025, in a shortened post-Thanksgiving session, capping a strong week despite a technical glitch at the Chicago Mercantile Exchange that disrupted futures and options trading. The S&P 500 rose 36.48 points or 0.54% to 6,849.09, marking its fifth straight gain and best weekly advance since May, reversing November’s earlier slide to end the month green. The Dow Jones Industrial Average climbed 289.30 points or 0.61% to 47,716.42, while the Nasdaq Composite added 151.00 points or 0.65% to 23,365.69. This cross-asset rebound, including stocks, bonds, Bitcoin, and commodities, defied recent AI valuation concerns and CME’s outage caused by a data center cooling failure, which lasted longer than a 2019 incident but saw alternative venues handle spillover.

Sector gains were broad, with Energy leading at 1.32%, followed by Consumer Discretionary at 0.90% and Communication Services at 0.72%, while Health Care lagged at -0.49%. Actives featured NVIDIA down 1.81% to 177.00 on 121.3 million volume amid AI scrutiny, Intel surging 10.19% to 40.56, Bitfarms up 12.26% to 3.48, and BigBear.ai up 5.32% to 6.34. The week’s 3.7% S&P gain was fueled by Alphabet’s AI model release restoring Big Tech confidence, with the index up 17% year-to-date.

Corporate highlights included Tilray Brands slumping after a one-for-10 reverse stock split. Broader sentiment reflected renewed risk appetite, with Bitcoin above $90,000 up 7% from November lows, and heavily shorted stocks surging 28% year-to-date. Volatility eased, with the Cboe Volatility Index at 16.35, down 5%. Goldman Sachs’ most-shorted basket soared, while inverse ETFs plunged 84%. Barclays’ Emmanuel Cau noted “don’t fight the Fed and don’t fight AI” as the mantra, amid dovish signals like Kevin Hassett as potential Fed chair and Fed Governor Stephen Miran’s rate-cut views.

Weekly, the Morningstar US Market Index gained 3.84%, led by consumer cyclicals up 5.33% and communication services up 4.59%. Large-caps rose 3.88%, mid-caps 3.46%, small-caps 4.54%; growth up 4.52%, blend 3.67%, value 2.89%. Top gainers: Kohl’s up 56.37%, Bloom Energy 21.40%, Broadcom 18.46%, Reddit 17.97%, SoFi 17.85%. Losers: Tilray down 10.27%, Zscaler 8.55%, Warner Music 7.98%, John Deere 4.67%.

Black Friday online spending hit $11.8 billion, up 9.1%, driven by AI tools like Walmart’s Sparky, per Adobe, with global AI influence at $14.2 billion. Mastercard noted 10.4% e-commerce growth vs. 1.7% in-store. Hot items: LEGO, Pokemon, consoles. Investors eye December’s Santa rally, with swaps pricing nearly a full quarter-point Fed cut, amid labor softness. Upcoming: ISM Manufacturing December 1, ADP Employment December 3.

OVERVIEW OF THE AUSTRALIAN MARKET

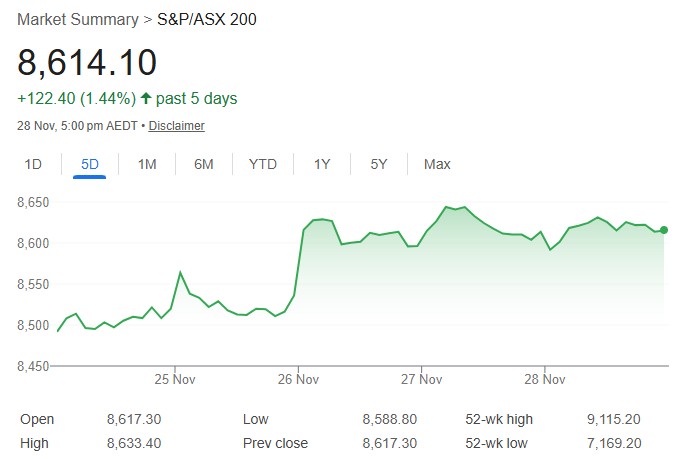

Australian equities closed mixed on November 28, 2025, in a low-volume session amid US holiday aftermath, snapping a four-week ASX 200 losing streak with the benchmark’s best weekly gain since May. The S&P/ASX 200 dipped 3.2 points or 0.04% to 8,614.1, while the All Ordinaries rose 6.7 points or 0.08% to 8,918.7. Advancers outnumbered decliners 181 to 98 in the ASX 300, with the index up 2.4% weekly, 2.4% from intraweek low.

Eight sectors advanced, led by Consumer Staples up 1.25% to 11,943.8 on Woolworths’ 3.2% rally post-JP Morgan upgrade and Endeavour up 2%. Utilities gained 0.99% to 9,856.9, Information Technology 0.91% to 2,370.0, extending a 6% weekly surge snapping four-week losses. Materials rose 0.43% to 19,918.9, up over 5% weekly despite China property woes pressuring iron ore. Health Care up 0.11%, Industrials 0.10%. Financials fell 0.72% to 8,993.1 with big banks lower but up 0.2% weekly; Real Estate down 0.34%, Communication Services flat.

Gold Sub-Index up 1.3%, with spot gold at $4,184 lifting VanEck Goldminers ETF 10% weekly to five-week highs. Lithium and silver stocks shone: Lake Resources up 22.0%, Argosy Minerals 15.5%, Boab Metals 13.6%, Winsome Resources 13.3%, Aeris Resources 12.4%, Silver Mines 11.1%, Galan Lithium 10.4%, Polymetals Resources 10.1%. Invictus Energy up 19.0% post-AGM. Focus Minerals up 10.7%, Titan Minerals 9.6%, Select Harvests 9.5% on substantial holding. HMC Capital up 9.0%, Artrya 8.6%, New Murchison Gold 8.1%.

Losers: SKS Technologies down 5.3% post-rally, Eagers Automotive 3.7%, Qualitas 3.6%, Suncorp 3.6% on weather update, Centuria Capital 3.5% post-AGM.

Moomoo’s Michael McCarthy noted US rate cut hopes drove gains but warned local repricing risks as October CPI at 3.8% year-on-year (above 3.6% poll) leaves RBA no easing room, possibly hiking. Q3 capex surged 6.4% vs. 0.5% expected.

Energy flat weekly, coiling on Ukraine peace vs. Middle East risks. Tech’s dip-buying mirrored Nasdaq. AUD/USD at 0.6528, down 0.09% but two-week highs.

Upcoming: Q3 GDP December 3, October trade December 4. Mr McCarthy flags slow burn on rate divergence.