| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,734.61 | 144.2 | 0.31% |

| S&P 500 | 6,738.44 | 39.04 | 0.58% |

| Nasdaq | 22,941.80 | 201.4 | 0.89% |

| VIX | 17.3 | -1.3 | -6.99% |

| Gold | 4,130.70 | -14.9 | -0.36% |

| Oil | 61.71 | -0.08 | -0.13% |

OVERVIEW OF THE US MARKET

Wall Street rebounded on October 23, 2025, with big tech leading gains as trade tensions eased ahead of Friday’s consumer price index report, offsetting a spike in oil that fueled inflation concerns. The S&P 500 rose 0.6% to near all-time highs, the Nasdaq 100 climbed 0.9%, and the Dow Jones Industrial Average added 0.3%. Energy stocks surged 1.3% amid crude’s 5.4% jump following US sanctions on Russian oil firms to pressure an end to the Ukraine war, while information technology gained 1% led by Tesla’s 2.3% rally despite missing profit estimates. Industrials and materials also rose nearly 1%, but consumer staples fell 0.4%.

Gold halted its slide, up 0.5% as geopolitical risks bolstered safe-haven demand, while Bitcoin advanced 2.3%. Beyond Meat plunged 20.7% amid ongoing volatility, Rigetti Computing soared 9.8% on quantum sector buzz, and Transocean jumped 13.7% with oil’s rally. Earnings showed durability, with 87% of S&P reporters beating estimates per Yardeni Research, supporting JPMorgan’s Andrew Tyler view that solid results offset inflation angst, though Super Micro Computer disappointed with weak guidance and Molina Healthcare sank 17% on earnings miss and outlook cut. T-Mobile beat subscriber forecasts but slipped on competition, while Blackstone’s credit assets hit $508 billion, up 18% yearly.

Trade optimism grew as the White House confirmed Trump’s October 30 meeting with Xi Jinping, spurring hopes for de-escalation, with quantum firms rallying on reported federal funding talks—later refuted by Commerce. Nationwide’s Mark Hackett noted buy-the-dip resilience amid Corporate America’s strength, while UBS’s Ulrike Hoffmann-Burchardi sees Fed easing, AI spending, and earnings driving further upside, advising diversification amid US-China risks. Investors await September existing home sales at 4.06 million—meeting poll—and October 24 core CPI at 0.3% monthly, 3.1% annually, where Principal’s Seema Shah warns temporary tariff cushions may fade, risking sustained inflation.

A 22V survey showed 45% expecting risk-on post-CPI, with 61% viewing core on a Fed-friendly path, as Bowersock’s Emily Bowersock Hill anticipates cuts October 29 and December despite sticky prices, given labor focus.

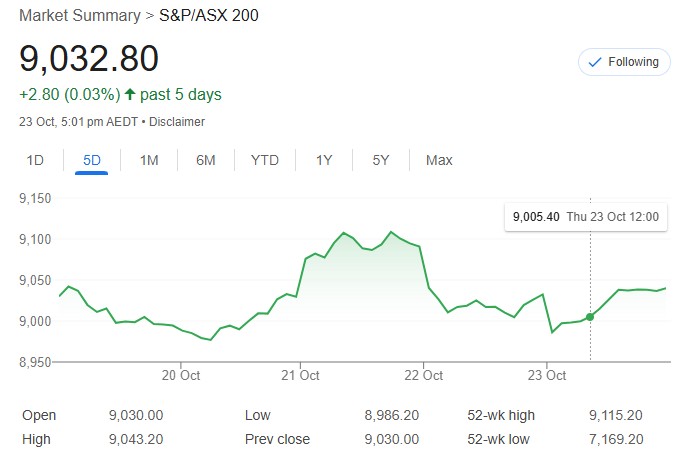

OVERVIEW OF THE AUSTRALIAN MARKET

The Australian share market edged higher on October 23, 2025, paring early losses as energy surged on global oil spikes, with the S&P/ASX 200 up 0.03% at 9,032.8 and the All Ordinaries gaining 0.09% at 9,329.1. Energy jumped 3.2% amid US Russia sanctions and crude’s rise, led by Woodside’s 4.3% advance on a US gas deal and Karoon Energy up 9.4% on Q3 report. Utilities rose 1.3%, consumer staples added 0.9%, but financials fell 0.8% with Big Four banks down modestly, and tech slipped 0.9%.

Fund flows favored energy amid Trump-Modi talks curbing Indian Russian oil buys, while gold rebounded 1.5% with Northern Star and Evolution up 2%, recovering a fraction of prior losses. Critical minerals gained post-US deal, with Iluka and Lynas over 3% higher, lithium’s Liontown and Pilbara up 4%. VHM surged 14.8% on funding support, Baby Bunting jumped 12.7%, but Cobalt Blue fell 21.4% amid sector weakness. Fortescue rose 2.4% on production, but BHP dipped 1.2% at AGM.

IG’s Tony Sycamore noted energy driving recovery from below 9000, with mixed miners and gold bounce. Investors digest October manufacturing PMI at 49.7—below prior 51.4 signaling contraction—services at 53.1, composite 52.6, potentially pressuring sentiment amid tariff risks and China ties.