| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 42124.65 | 61.29 | 0.15% |

| S&P 500 | 5718.57 | 16.02 | 0.28% |

| Nasdaq | 17974.27 | 25.95 | 0.14% |

| VIX | 15.89 | -0.26 | -1.61% |

| Gold | 2652.70 | 0.70 | 0.04% |

| Oil | 70.80 | 0.45 | 0.65% |

US MARKET

U.S. stocks closed higher today, with all three major indices posting gains. The Dow Jones Industrial Average (DJIA) inched up by 0.1% to close at 42,124.65, while the S&P 500 rose 0.3% to 5,718.57. The Nasdaq Composite followed with a modest 0.1% gain, finishing at 17,974.27.

Among the top performers in the S&P 500, Tesla Inc surged by 4.93%, First Solar Inc climbed 3.76%, and Tapestry Inc saw a 3.65% lift.

On the downside, Regeneron Pharmaceuticals Inc led the decliners with a 4.63% drop, followed by Moody’s Corp, which fell 3.17%, and Ross Stores Inc, which slid 2.81%.

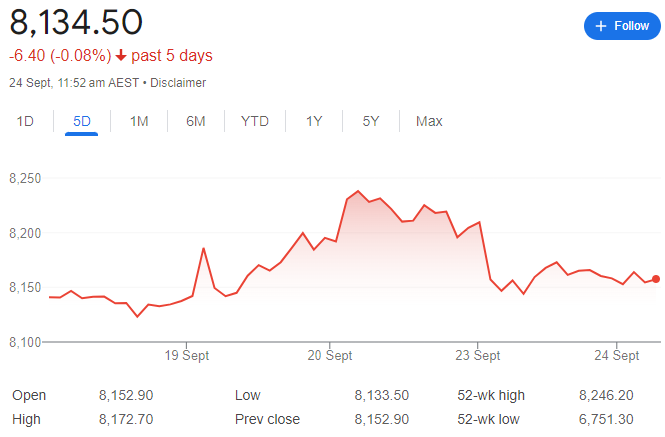

LOCAL MARKET