| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,091.74 | -498.5 | -1.07% |

| S&P 500 | 6,617.32 | -55.09 | -0.83% |

| Nasdaq | 22,432.85 | -275.23 | -1.21% |

| VIX | 24.69 | 2.31 | 10.32% |

| Gold | 4,068.90 | 2.4 | 0.06% |

| Oil | 60.71 | -0.03 | -0.05% |

OVERVIEW OF THE US MARKET

Wall Street extended its slide on November 18, 2025, as a selloff in megacap technology stocks deepened amid growing skepticism over artificial intelligence valuations and profitability, marking the S&P 500’s longest losing streak since August. The S&P 500 dropped 0.83% to 6,617.32, its fourth straight decline and the lowest close in over a month, down more than 3% from its late-October peak. The Nasdaq Composite fell 1.21% to 22,432.85, reflecting heavy tech pressure, while the Dow Jones Industrial Average slid 1.07% to 46,091.74. The MSCI World Index also declined 1.1%, underscoring global risk aversion as investors de-risked ahead of Nvidia’s pivotal earnings.

Sector performance highlighted defensive rotations amid the rout: Health Care rose 0.54%, Energy gained 0.61%, and Real Estate added 0.36%. Communication Services eked out a 0.11% advance, while Consumer Staples climbed 0.15%. However, losses dominated: Consumer Discretionary tumbled 2.50%, Information Technology slid 1.68%, and Industrials fell 0.48%. Nvidia dropped 2.81% as anxiety built over Wednesday’s results, expected to test AI hype despite anticipated beats—analysts like JPMorgan’s Daniel Pinto warned of potential corrections in lofty valuations. Ondas Holdings surged 25.34% on volume, while Opendoor Technologies fell 4.08%. The Bloomberg Magnificent 7 Total Return Index shed 1.8%, with Microsoft and Amazon declining after downgrades from Rothschild & Co, citing unclear AI returns.

The pullback reflects mounting doubts on AI’s revenue generation amid massive capex, with Carson Group’s Sonu Varghese questioning the trend’s longevity. Investors’ cash below Bank of America’s sell-signal threshold signals positioning headwinds, per Michael Hartnett, potentially exacerbating declines without a December Fed cut. Home Depot fell 6% after cutting guidance, citing consumer caution on big-ticket items, while the Russell 2000 rose 0.3%, showing small-cap resilience. VIX hovered near 25, its highest in a month, amid broader volatility.

Corporate news included Microsoft and Nvidia’s $15 billion Anthropic investment, tying the startup closer to OpenAI backers, and Meta’s antitrust win on Instagram/Whatsapp. Alphabet rose after a Loop Capital upgrade. Strategists remain mixed: Navellier & Associates’ Louis Navellier sees amplified leverage from mega-tech weighting but strong earnings as support, while Main Street Research’s James Demmert expects Nvidia to exceed estimates, potentially fueling a Santa rally to 7,100. HSBC’s Harriet Smith dismisses bubble fears, noting deep-pocketed incumbents. However, Piper Sandler’s Craig Johnson warns of deeper corrections, and Miller Tabak’s Matt Maley flags financial stocks nearing breakdowns amid credit woes like Capital One’s charge-off spike.

Economic data showed jobless claims at 232,000 for week ended October 18, with ADP noting 2,500 weekly cuts through early November, signaling labor softness. Homebuilder confidence edged to 38, per NAHB, amid high rates and prices. Fed’s divide deepened: Governor Waller backed December cut on weakening jobs, while Richmond’s Barkin offered optimistic inflation views but urged data wait. Minutes Wednesday may reveal October splits.

Volume was 18.66 billion shares, below averages, with advancers edging decliners 1-to-1 on Nasdaq. Tuesday brings August durable goods (0.2%), Wednesday October CPI (core MM 0.3%), and Thursday September jobs (50,000 payrolls, 4.3% unemployment)—a soft print could revive cut odds, now ~50%, per futures.

OVERVIEW OF THE AUSTRALIAN MARKET

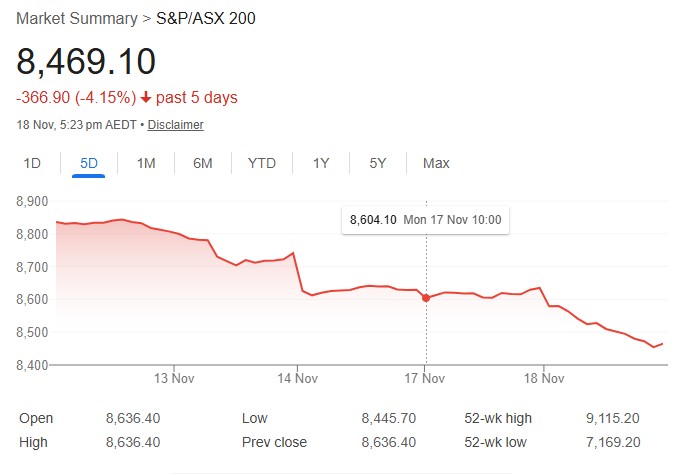

Australian shares plunged on November 18, 2025, posting their second-biggest daily loss of the year as global AI valuation concerns hammered technology stocks and broader risk aversion weighed, erasing over $200 billion from market value since mid-October peaks. The S&P/ASX 200 tumbled 1.94% to 8,469.1, its lowest since June, down 7% from four-week highs amid US selloffs and RBA minutes signaling limited cut scope without inflation turnaround. The All Ordinaries dropped 1.99% to 8,738.3, with Small Ords falling 2.66%, All Tech crashing 4.34%, and Emerging Companies sliding 3.67%. Decliners crushed advancers 264-to-23 in ASX 300.

Sector carnage was widespread: Information Technology plunged 5.99%, with Technology One cratering 17.2%—its worst in two decades—post-missed FY25 profit, joined by Catapult Sports (-11.7%), Superloop (-11.7%), and Wisetech Global (-4.6%). Materials sank 3.00%, dragged by iron ore giants, gold miners amid spot gold’s 4% drop since Thursday, and mixed falls—BHP, Rio Tinto, Fortescue all down. Financials fell 1.90%, with big banks like Commonwealth (-2% to seven-month low) hit by rate-cut doubts. Energy dropped 1.78% on oil/gas slips and coal/uranium weakness. Consumer Discretionary (-1.33%), Communication Services (-1.40%), Real Estate (-1.45%), Industrials (-1.29%), Utilities (-0.74%), Health Care (-0.52%), and Consumer Staples (-0.20%) all declined.

Bright spots were sparse: James Hardie surged 9.9% after Q2 FY26 results and CFO appointment, boosting guidance. Inverse ETFs gained: Global X Ultra Short Nasdaq-100 (+5.3%), BetaShares US Strong Bear (+4.5%), BetaShares Australian Equities Strong Bear (+4.4%). Eroad rose 5.0% on Cleanaway deal, SKS Technologies +4.3% on acquisition. Lithium bucked trends: Pilbara Minerals (+3.3%), Liontown (+2.1%) in uptrends. A2 Milk (+1.7%) and GQG Partners (+3.5%) advanced.

The rout reflects de-risking ahead of Nvidia earnings, US data resumption, and Japan’s bond jitters, per IG’s Tony Sycamore—calling it an overreaction ripe for bounce. RBA minutes Tuesday (11:30 AEDT) may clarify easing views; Q3 wages Wednesday (QQ 0.8%, YY 3.4%) key for inflation—stronger could delay cuts. Flash PMIs Wednesday gauge activity.

Strategists mixed: Capital.com’s Kyle Rodda sees positioning and momentum driving drops, while Schroders’ Johanna Kyrklund remains optimistic on benign economy, valuations expensive but sustainable. Dakota Wealth’s Robert Pavlik warns of protracted slowdowns. Bitcoin below $90,000 and gold slips amplified risk-off.

Volume reflected panic, with AUD/USD -0.15% to 0.6484. Wednesday’s wages precede Thursday’s FOMC minutes, PBoC LPR unchanged (3%/3.5%), Friday’s US jobs (50,000 payrolls). Brokers like Morgan Stanley favor equities over bonds, eyeing earnings despite pullbacks.