| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 46,397.89 | 81.82 | 0.18% |

| S&P 500 | 6,688.46 | 27.25 | 0.41% |

| Nasdaq | 22,660.01 | 68.86 | 0.30% |

| VIX | 16.28 | 0.16 | 0.99% |

| Gold | 3,892.40 | 19.2 | 0.50% |

| Oil | 62.45 | 0.08 | 0.13% |

OVERVIEW OF THE US MARKET

US equities extended gains for a second consecutive quarter despite subdued trading Tuesday, as investors weighed the economic risks of a looming US government shutdown. The S&P 500 closed 0.4% higher, capping its strongest September in 15 years, fueled by optimism surrounding artificial intelligence and expectations of lower interest rates. The Nasdaq 100 and Dow Jones also advanced, while Treasuries gained for a third straight quarter, reflecting investor caution.

Concerns remain that a shutdown could delay the release of critical labor data, including Friday’s nonfarm payrolls, which would obscure the Federal Reserve’s policy outlook. Economic readings over the past month show a cooling labor market and inflation trending lower, though still above the Fed’s 2% target. Analysts warn that an “information vacuum” may increase volatility, with stocks vulnerable to corrections given stretched valuations. The JOLTS report showed job openings steady in August but subdued hiring, signaling weaker labor demand.

Fed officials struck a cautious tone. Chicago Fed President Austan Goolsbee cited tariff-related uncertainty, while Boston Fed’s Susan Collins said further rate cuts may be warranted this year. Fed Vice Chair Philip Jefferson noted simultaneous downside risks to employment and upside risks to inflation, underscoring the policy challenge. Economists, including Nomura’s David Seif, suggested that even without fresh data, the Fed is likely to proceed with a 25-basis-point rate cut in October as indicated in its dot plot.

Historically, short shutdowns have had limited impact on GDP or equities, though longer disruptions tend to weaken stocks while supporting bond markets, according to Citi Research. Sectors reliant on government contracts, such as defense and health care, may face near-term weakness but could present longer-term buying opportunities.

In corporate news, Pfizer secured relief from tariffs by agreeing to cut some drug prices, Nike posted stronger-than-expected sales on robust North American demand, and CoreWeave struck a $14.2 billion computing supply deal with Meta. Meanwhile, the Fed lowered Morgan Stanley’s stress capital buffer requirement to 4.3% from 5.1%.

On the broader market front, the Bloomberg Dollar Spot Index slipped 0.2%, the yen strengthened, and cryptocurrencies were mixed with Bitcoin steady but Ether falling nearly 2%. Commodities saw oil decline 1.4% as OPEC+ considered faster output hikes, while gold gained 0.5% on safe-haven demand.

Overall, markets remain resilient but face heightened uncertainty from political gridlock, slowing labor conditions, and a delicate balancing act for the Fed as it navigates both inflation risks and weakening growth.

OVERVIEW OF THE AUSTRALIAN MARKET

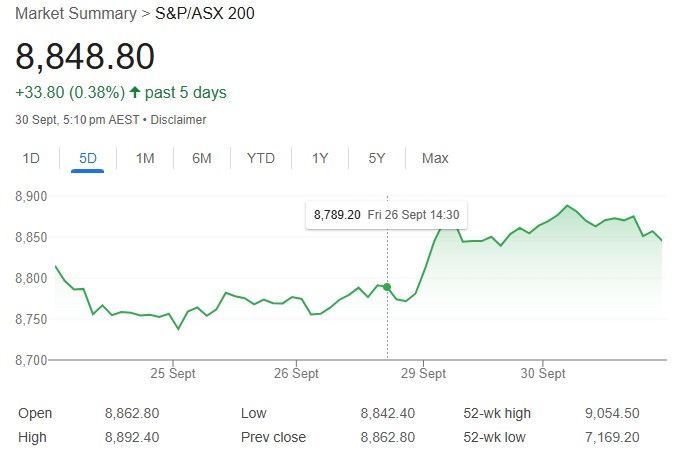

Australia’s share market erased early gains to close lower on September 30, 2025, after the Reserve Bank of Australia held interest rates steady and adopted a cautious tone on inflation, diminishing expectations for a November cut. The S&P/ASX 200 fell 0.16% to 8,848.8, while the All Ordinaries slipped 0.14% to 9,135.9. Nine of eleven sectors ended in the red, with Energy down 1.59% amid tumbling oil prices and OPEC+ signaling production increases, and Materials up 0.89% buoyed by record gold prices and supply concerns in copper. Resources majors like BHP Group rose 1.5%, Rio Tinto added 0.6%, and South32 climbed 3.0%, while gold miners such as Resolute Mining gained 4.0% and Ramelius Resources advanced 2.6%.

The RBA’s decision to keep the cash rate at 3.6% was unanimous, with Governor Michele Bullock emphasizing data dependency and noting upside surprises in recent inflation and activity figures, including partial data suggesting a higher-than-expected September quarter print. This hawkish lean prompted traders to pare bets on near-term easing, with the probability of a November cut dropping to about 38%. Energy stocks extended their monthly losses beyond 10%, led by Woodside Energy down 1.7%, Santos falling 2.5%, and Beach Energy dropping 3.4%, reflecting a supply glut in crude. Uranium plays bucked the trend, with Elevate Uranium up 11.3% and Alligator Energy rising 10.3% amid sector strength.

Financials shed 0.51%, with Commonwealth Bank declining 0.9% to $166.90, while health care and utilities also weakened. Defence firm Droneshield surged 5.9% to a new high of $4.66 for a second session. Outside the top 200, Stakk soared 82.4% on a T-Mobile vendor deal, and Veem jumped 23.8% following a capital raise. Building approvals data disappointed earlier, falling 6% in August against expectations of a 3% rise, adding to uncertainty on domestic recovery. Investors now eye Wednesday’s trade balance and exports figures, amid global risks from US shutdown threats and Trump’s new tariffs on pharmaceuticals and furniture, which could pressure Australian exports and inflate costs.