| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,147.48 | -309.74 | -0.65% |

| S&P 500 | 6,734.11 | -3.38 | -0.05% |

| Nasdaq | 22,900.59 | 30.23 | 0.13% |

| VIX | 19.83 | -0.17 | -0.85% |

| Gold | 4,084.20 | -110.3 | -2.63% |

| Oil | 59.95 | 1.26 | 2.15% |

OVERVIEW OF THE US MARKET

Wall Street ended mixed on November 14, 2025, as a tech rebound faded amid persistent Fed caution and data anticipation, with the S&P 500 slipping 0.05% to 6,734.11 after erasing an earlier 1.4% drop, holding above its 50-day average. The Nasdaq Composite edged up 0.13% to 22,900.59, buoyed by AI names, while the Dow Jones Industrial Average fell 0.65% to 47,147.48. Post-shutdown volatility persisted, with shutdown relief giving way to rate uncertainty—December cut odds below 50%—as speakers like Kansas City’s Jeffrey Schmid highlighted “too hot” inflation beyond tariffs, risking governance tensions per Evercore’s Krishna Guha.

Information technology gained 0.74%, snapping a three-day slide, with Nvidia up 1.77% ahead of Wednesday’s earnings—options implying a 6.2% swing, the highest in a year—as hyperscaler capex signals sustained AI demand. Tesla rose 0.59%, Ondas surged 9.45% topping actives. Energy led at +1.37% on oil’s 2.1% rise to $59.90 amid Russia-Ukraine risks, Novorossiysk export halt. Real estate added 0.28%, utilities 0.02%. Communication services dropped 0.80%, financials 0.97% on rate-pause bets.

Kyle Rodda at Capital.com flagged Nvidia’s report as a test for AI valuations, potentially easing or inflaming fears. Morningstar noted S&P flat weekly, healthcare +3.6%, energy +2.53%, consumer cyclicals -2.6%. Large-caps +0.20%, small-caps -1.23%. Bob Lang at Explosive Options saw bounce potential but dip-buyers wary; Ken Mahoney at Mahoney Asset Management noted rotations into healthcare, staples—bottoming signals amid AI doubts. Daniel Skelly at Morgan Stanley called it a tech reckoning, not wreck, with healthcare overlooked.

President Trump’s tariff cuts on 200+ foods—beef, coffee, bananas—retroactive midnight, via deals with Argentina, Ecuador, etc., addressed inflation angst post-election losses, eyeing $2,000 dividends funded by duties. Analysts like Reuters’ Lewis Krauskopf eyed Nvidia as pivotal for tech, amid AI bubble worries—S&P +14% YTD. Walmart, Target reports next week gauge consumer amid delayed data like September nonfarms (actual 22k vs 50k poll), October core CPI (0.3% actual matching poll).

Corporate highlights: Google’s $40B Texas data centers, emphasizing grid support; Oracle CDS surged on AI debt jitters. Applied Materials flagged sales drop but 2026 uptick. Walmart’s McMillon retires, Furner succeeds. Warner Bros. amended Zaslav’s options for sale scenario. Merck acquired Cidara for flu drug. Bristol Myers fell on heart drug setback. Boeing eyed Flydubai order. Emirates plans Starlink Wi-Fi. BlackRock-ACS $2B data JV. American Tower, EQT eye TDF. JBS US beef loss. BHP liable in Brazil dam. Nu AI credit boosts. Sigma Lithium resumed mining. Allianz raised its outlook. Siemens Energy upped targets. Richemont sales up. Jaguar Land Rover loss. Overall, session reflected resets, with Nationwide’s Mark Hackett seeing pullback as emotion vs fundamentals.

OVERVIEW OF THE AUSTRALIAN MARKET

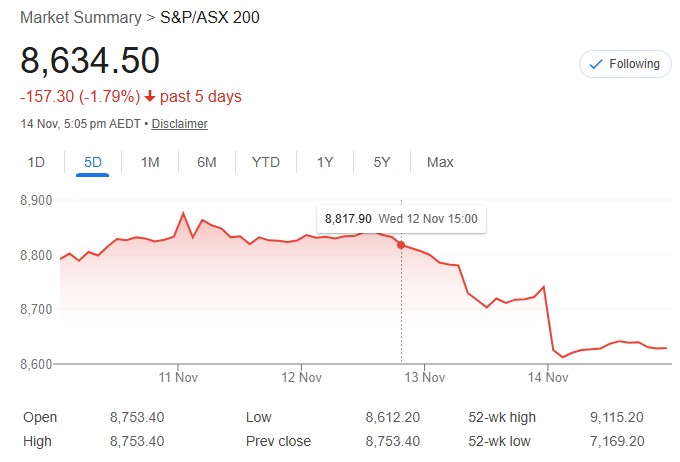

The Australian share market plunged to a near four-month low on November 14, 2025, marking its worst day in 10 weeks amid global risk aversion from Fed uncertainty and AI valuation jitters, with the S&P/ASX 200 tumbling 1.36% to 8,634.5—down 1.54% weekly, its third straight loss. All Ordinaries fell 1.41% to 8,907.0, decliners trouncing advancers 228 to 47 in ASX 300. Flat intraday reflected absent demand, low volume suggesting buyers on strike post-October jobs resilience—unemployment 4.3% vs 4.4% poll, +42.2k employed—cementing no RBA cuts soon.

Information technology cratered 4.42%, worst in seven months: Megaport -9.6%, Hub24 -8.0%, Life360 -6.7% (20% weekly loss). Financials dropped 1.86%: CBA -1.8% to a seven-month low $157.30 (down 18% from June peak), ANZ -2.6%, Westpac -1.6%, NAB -1.7%. Materials fell 1.43%: BHP -1.3%, Fortescue -1.0%, Rio -1.4%. Gold sub-index -2.2% on metal pause: Northern Star -1.9%, Evolution -2.4%, Westgold -4.9%. Consumer discretionary -1.30%, health -0.92% with CSL down.

Energy edged +0.20% on oil rebound: Santos +1.2%—utilities -0.07%, staples -0.16% least worst. AMP’s Shane Oliver tied to hawkish Fed—December odds 50/50—undercutting post-shutdown optimism. Capital.com’s Kyle Rodda saw AI unwind, valuations rich. Moomoo’s Jessica Amir flagged consolidation, global slowdown chasers.

Higher: Caprice +14.8% on gold extension, Lake +11.8% lithium, Nyrada +11.5%, Webjet +9.7% on prelims, Ausgold +8.0%. Lower: Rox -16.5% placement, Locksley -10.5%, BetaShares Crypto -9.8% on bitcoin plunge, Weebit -8.6%, Cobalt -8.7%, Silex -7.6% uranium. ACCC cleared the Seven-Southern merger. The opposition ditched net zero by 2050. Energy Minister Bowen pushes COP31 host in Brazil. ASX down 5% from October high, +5.8% YTD. AUD 65.37 US cents. Bitcoin $97,300, -4.7% daily. Overall, risk-off dominated, resources mixed amid China AI pivot to power, metals per BofA—copper demand +20% annually.