| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,457.22 | -797.6 | -1.65% |

| S&P 500 | 6,737.49 | -113.43 | -1.66% |

| Nasdaq | 22,870.36 | -536.1 | -2.29% |

| VIX | 20 | 2.49 | 14.22% |

| Gold | 4,182.90 | -11.6 | -0.28% |

| Oil | 58.89 | 0.2 | 0.34% |

OVERVIEW OF THE US MARKET

Wall Street tumbled on November 13, 2025, snapping a brief post-shutdown rally as hawkish Federal Reserve comments and impending data deluge reignited concerns over rate cuts, triggering heavy selling in tech megacaps and broader risk assets. The S&P 500 dropped 1.66% to 6,737.49, its steepest decline in over a month and third such drop in two weeks, while the Nasdaq Composite slid 2.29% to 22,870.36 amid AI valuation jitters. The Dow Jones Industrial Average fell 1.65% to 47,457.22, erasing recent highs. With the 43-day government shutdown ended by President Trump’s signature, markets shifted from relief to skepticism, as delayed reports like October’s incomplete jobs data—skipping unemployment per White House adviser Kevin Hassett—clouded the economic picture, prompting rotations into defensives.

Information technology led losses at -2.37%, with Nvidia down 3.58% on profit-taking ahead of next week’s earnings, extending Magnificent Seven’s 2.7% plunge. Tesla sank 6.64%, and consumer discretionary fell 2.73% amid broader growth worries. Ondas Holdings topped actives with 220 million shares, surging 19.06% on network hype, while Opendoor dropped 8.64%. Pfizer edged down 0.31%. Energy bucked the trend up 0.31% as oil rose slightly to $58.67, while consumer staples held flat. Bitcoin plunged 3.3% below $100,000, down 20% since early October, reflecting fading risk appetite.

Fed officials fueled the rout: St. Louis’s Alberto Musalem urged caution on rates amid above-target inflation, Cleveland’s Beth Hammack called for “somewhat restrictive” policy, and Minneapolis’s Neel Kashkari opposed October’s cut, undecided on December. Odds of a December reduction dipped below 50%, per CME FedWatch, as Powell’s prior “not foregone” stance gained traction. Matt Maley at Miller Tabak noted expensive markets need lower rates to justify valuations, with data uncertainty raising fears. Fawad Razaqzada at Forex.com highlighted sentiment-driven action amid data voids, questioning if the rally’s exuberance has peaked.

Analysts like Michael O’Rourke at JonesTrading saw profit-taking post-earnings, while Chris Grisanti at MAI Capital viewed it as healthy rotation, not yet buying weakness. David Miller at Catalyst Funds noted shifts from AI narratives to cyclicals like industrials (-1.52%) and financials (-1.31%), signaling sustainable broadening. Carol Schleif at BMO Private Wealth cautioned on debt-financed AI spend but noted under-levered hyperscaler balance sheets. Louis Navellier emphasized Nvidia’s report as pivotal for year-end strength.

Corporate news included Boeing ending its strike with a new contract, Cisco jumping 4.6% in late trade on upbeat 2026 forecast capturing AI demand. Disney tumbled 7.8% on distribution fights and film slate warnings. Tencent’s 15% revenue beat sustained growth, Alibaba eyed ChatGPT-like AI revamp. Google’s EU probe over news rankings added pressure. Verizon eyed job cuts under new CEO. Pfizer eyed BioNTech stake sale. Uber expanded ski rides, Starbucks faced strikes. Overall, the session underscored volatility, with Seema Shah at Principal urging nimble portfolios amid magnified reactions to scarce data.

OVERVIEW OF THE AUSTRALIAN MARKET

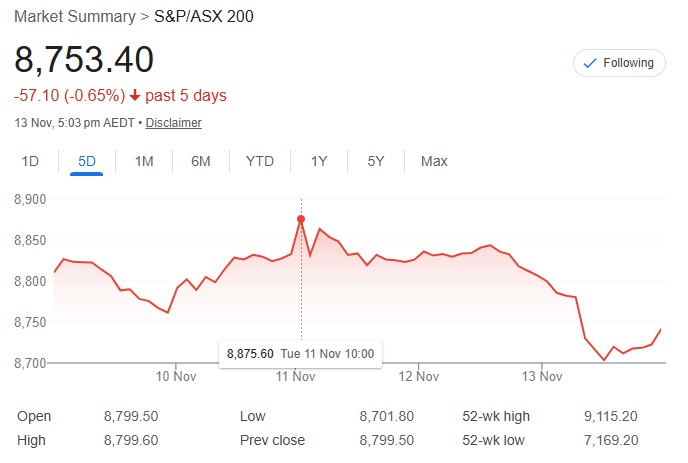

The Australian share market extended losses on November 13, 2025, closing at its lowest since September 18 as stronger-than-expected October jobs data—unemployment at 4.3%, employment +42.2k—dashed near-term RBA cut hopes, spiking yields and hammering rate-sensitive sectors. The S&P/ASX 200 fell 0.52% to 8,753.4, near session midpoint, while All Ordinaries dropped 0.49% to 9,034.5, with decliners outpacing advancers 182 to 99 in ASX 300. This reflected global risk-off from US Fed divisions and data anxiety, prompting rotations into cyclicals amid US shutdown end.

Information technology plunged 3.92%, with Xero down 9.0% on interim results raising expansion doubts. Communication services fell 2.31%, real estate 2.78% with GPT, Stockland, others off over 3%. Energy slid 2.09% on crude supply worries, dragging Woodside (-2.8%), Santos (-2.3%). Financials shed 0.80%, ANZ tumbling 4.9% ex-div, though CBA rebounded 1.1%. Consumer staples dropped 1.34%, utilities 0.75% on yield spike—2-year to 3.73% +10bps.

Materials bucked at +1.71%, lithium surging: Core Lithium +26.7%, IGO +15.3%, Galan +15.2%, Lake +13.3%, Wildcat +12.8%, Liontown +10.3%, Pilbara +10.2%. Gold shone with spot at $US4,215/oz; Northern Star, Newmont, Evolution up 2.5-3.8%. Fortescue led large caps +2.4% to $20.44, BHP, Rio edged up on iron ore recovery. Health care gained 0.23%, CSL +1.6% near seven-year lows.

BetaShares’ David Bassanese said data wiped December cut chances, affirming RBA’s tight economy view—rates down next year only on inflation easing or weakening. BDO’s Anders Magnusson noted statistical variation in September spike, healthy market intact. EY’s Cherelle Murphy saw employment growth slowing to 1.6% annually, post-pandemic boom fading. Indeed’s Callam Pickering flagged sluggish 160k YTD jobs vs 325k prior.

Stock movers: Domino’s +11.7% on AGM, Flight Centre +7.4% on guidance. Droneshield cratered 31.4% on exec sales, query response. GrainCorp -10.8% on profit drop. Webjet -17.2% on prelims. Infratil -7.1% on interim. ACCC cleared Seven-Southern Cross merger. Opposition ditched net zero by 2050, per Liberal’s Sussan Ley. Moomoo’s Jessica Amir eyed consolidation, big money chasing global slowdown plays. Overall, session highlighted yield-driven pressures, resources eyeing China data dump Friday.