| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 42,171.66 | -44.14 | -0.10% |

| S&P 500 | 5,980.87 | -1.85 | -0.03% |

| Nasdaq | 19,546.27 | 25.18 | 0.13% |

| VIX | 20.5 | 0.36 | 1.79% |

| Gold | 3,372.00 | -36.1 | -1.06% |

| Oil | 75.72 | 0.58 | 0.77% |

OVERVIEW OF THE US MARKET

Israel’s ongoing strikes and Trump’s two-week window for U.S. involvement promise to keep oil markets on edge in the coming days. Should nuclear talks with Tehran resume, trading firm Ritterbusch and Associates told clients Friday,

The S&P 500 and Nasdaq ended lower on Friday, with investors on edge over the Iran-Israel conflict heading into the weekend, as the U.S. considers whether to get involved.

Trading was choppy for much of the session. The S&P 500 also ended lower for the week, while the Nasdaq registered a weekly gain.

The Dow Jones Industrial Average (.DJI) rose 35.16 points, or 0.08%, to 42,206.82, the S&P 500 (.SPX) lost 13.03 points, or 0.22%, to 5,967.84 and the Nasdaq Composite (.IXIC) lost 98.86 points, or 0.51%, to 19,447.41.

Tech-related megacap stocks, including Nvidia (NVDA.O), were among the biggest negatives on the S&P 500 and Nasdaq.

Iran said it would not discuss the future of its nuclear program while under attack by Israel, as Europe tried to coax Tehran back into negotiations.

The White House said on Thursday that President Donald Trump will decide in the next two weeks whether the U.S. will get involved in the Israel-Iran air war, adding pressure on Tehran to negotiate.

For the week, the Dow was little changed, the S&P 500 was down 0.2% and the Nasdaq was up 0.2%.

Friday’s volume was higher than the recent average. The day marked a “triple-witching” event, which is the simultaneous expiration of stock options, stock index futures, and stock index options contracts that takes place once every quarter.

Investors also weighed comments from Federal Reserve officials after the Fed on Wednesday left interest rates unchanged and Fed Chair Jerome Powell warned inflation could pick up pace over the summer as Trump’s tariffs work their way to consumers.

The Fed this week held its policy rate steady in the 4.25% to 4.5% range where it has been since December.

In a Wednesday press conference, Fed Chair Jerome Powell cautioned against putting too much weight on any particular outlook at this point, given how volatile the debate around trade has been and how many key decisions remain outstanding.

OVERVIEW OF THE AUSTRALIAN MARKET

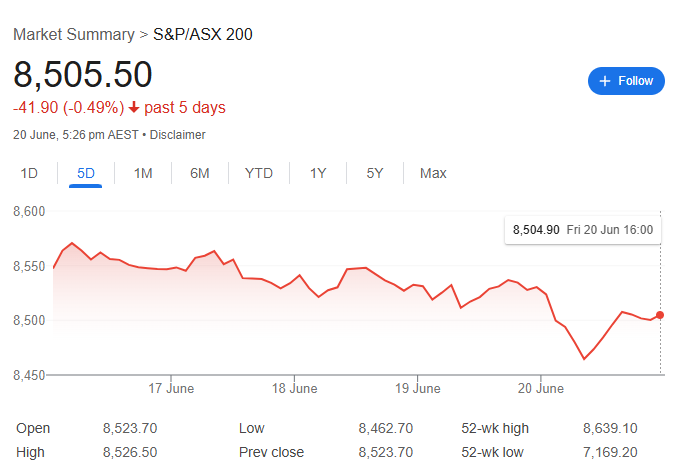

The Australian equity market fell to the lowest in more than two weeks on Friday as investors took some money off the table as they wait to see if the United States joins Israel’s conflict with Iran.

The benchmark S&P/ASX 200 Index fell 18.2 points, or 0.2 per cent, to 8505.5 on Friday AEST – its fourth day down in a row and the lowest level since the start of June as six out of 11 sectors traded in the red. Over the week, the bourse has fallen just 0.5 per cent.

Australia’s share market has given up a five-week winning streak, as investors grapple with military conflict, global growth concerns and lofty valuations.

The slump came after six sessions of surging oil prices amid escalating Israel-Iran conflict and as US President Donald Trump flagged potential American military involvement within two weeks.

The broader investor uncertainty then collided with heavy falls in big miners after weak economic data from China, as Rio Tinto plummeted to its lowest close since 2022, IG Markets analyst Tony Sycamore told AAP.

Five of 11 local sectors sectors improved on Friday, but a whopping 4.4 per cent drop in materials stocks over the week weighed on the bourse.

Financials slipped 0.6 per cent on Friday to finish roughly flat for a second week, a day after CBA etched its latest record high of $183.31 a share.

All four big banks closed in the red, with ANZ facing the sharpest decline with a 2.5 per cent slip to $28.39.

In banking news, former federal coalition finance minister Simon Birmingham was appointed the Australian Banking Association’s chief executive, replacing Anna Bligh after eight years at the helm.

Australian energy stocks have had a massive week, surging almost 11 per cent since Israel launched air strikes on Iran last Friday.

Woodside is up 7.7 per cent over the same period, while Santos has rallied 12 per cent.

Oil prices hit their highest levels since January overnight as the conflict raged on, but eased to $US75.24 a barrel after Mr Trump’s two-week decision window relieved fears of an immediate US attack. The IT sector had a surprisingly good week despite broader risk-off sentiment, edging 0.3 per cent higher since Monday’s open.

The Australian dollar is buying 64.76 US cents, up slightly from 64.71 US cents on Thursday at 5pm, coiling tightly near the mid-level of its recent range with the greenback.

Looking ahead, while the Middle East conflict is likely to dominate headlines, it’s also a massive week for macroeconomic data.