| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 42,171.66 | -44.14 | -0.10% |

| S&P 500 | 5,980.87 | -1.85 | -0.03% |

| Nasdaq | 19,546.27 | 25.18 | 0.13% |

| VIX | 20.14 | -1.46 | -6.76% |

| Gold | 3,385.40 | -22.7 | -0.67% |

| Oil | 76 | 0.86 | 1.14% |

OVERVIEW OF THE US MARKET

U.S. index futures fell Thursday, as conflict in the Middle East pushed global oil prices toward their highest settling level since January.

U.S. equity and bond markets were closed for the Juneteenth holiday, but futures continued to trade. Contracts tied to the S&P 500 and Dow Industrials dropped about 0.9%.

Global markets have been rattled in recent days by the conflict between Iran and Israel, which investors fear could spread into a wider conflict and disrupt oil supply. The two sides continued to trade fire Thursday. President Trump told senior aides late Tuesday he approved of attack plans for Iran, but was holding off to see if Tehran would abandon its nuclear program, The Wall Street Journal reported.

The Fed’s decision to hold rates steady – coupled with Powell’s latest warning on tariffs – underscores the delicate balance facing policymakers guiding the economy toward continued expansion. While officials continued to pencil in two rate cuts in 2025, they downgraded their estimates for growth this year while lifting forecasts for unemployment and inflation.

OVERVIEW OF THE AUSTRALIAN MARKET

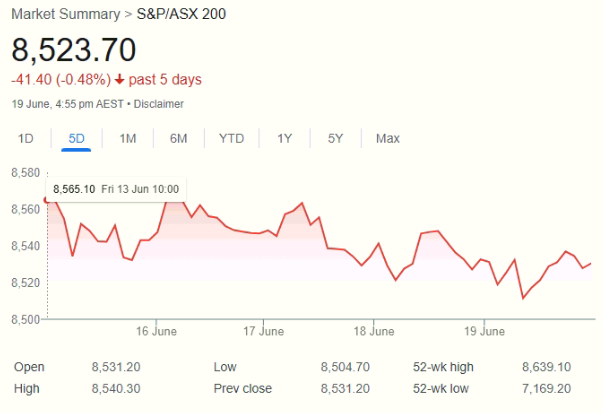

The ASX 200 edged down 0.09% to close at 8,523.7, weighed by heavy losses in miners despite a strong showing from the banks. Geopolitical jitters and stagflation concerns kept sentiment subdued.

Financials lifted 0.9%, powered by rate cut hopes after May’s jobs data surprised to the downside.

Westpac surged 1.7%, and CBA hit an all-time high, closing at $182.85 after briefly touching $183.31 intraday.

But the shine faded elsewhere—materials sank 1.8%, as iron ore tumbled to US$94.40/tonne, a nine-month low.

BHP dropped 2.3%, Rio Tinto fell 2.1%, and Fortescue lost 1.7%, dragging the broader market lower.

Tech stocks reversed Wednesday’s gains—WiseTech slid 1.9% after board shake-up news, while Xero fell 0.9% and Technology One lost 1.5%.

Healthcare dipped 1%, led by CSL, which dropped 1.3% ahead of upcoming U.S. regulatory hearings.

Among consumer names, KMD Brands (owner of Kathmandu and Rip Curl) sank 3.9% after blaming warmer autumn weather for sluggish insulated clothing sales.

On the upside, Brent crude rose 2% to just under US$76, helping limit losses in energy, though the sector still slipped 0.6% overall.

The Australian dollar weakened, buying 64.71 US cents, down from 65.07 on Wednesday.