| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 42761.76 | -1.11 | 0.00% |

| S&P 500 | 6005.88 | 5.52 | 0.09% |

| Nasdaq | 19591.24 | 61.28 | 0.31% |

| VIX | 17.16 | 0.39 | 2.33% |

| Gold | 3345.70 | -9.20 | -0.27% |

| Oil | 65.36 | 0.07 | 0.11% |

OVERVIEW OF THE US MARKET

Wall Street traders focused on commercial talks between the US and China and which drove stocks higher, adding to an advance that put the S&P 500 within a striking distance of its record. Treasuries bounced after Friday’s selloff amid a drop in consumer expectations for inflation. The US equity benchmark is now just about 2% away from its February peak. Big tech led gains Monday, but Apple Inc. slipped 1% as it hasn’t featured much in the way of major AI releases during its Worldwide Developers Conference. Tesla Inc. erased losses that were earlier driven by a pair of analyst downgrades.

The S&P 500 rose 0.1%. The Nasdaq 100 rose 0.3%. The Dow Jones Industrial Average was unchanged. The Magnificent 7 rose 1.0%.

The S&P 500 has round-tripped from selloff to full recovery in under two months, marking the shortest “vol shock” on record. During prior volatility shocks, equities would typically take six to seven months for a round-trip and usually at this stage the US gauge would still be down almost 10%.

Trade talks between Washington and Beijing stretched on in London, with the US signalling a willingness to remove restrictions on some tech exports in exchange for assurances that China is easing limits on rare earth shipments. The meeting, which began Monday just after 1 p.m. local time, extended into the UK evening and may restart Tuesday if necessary. But markets moved higher on tariff postponement and the perception that they will be more moderate than initially announced. Markets are remaining headline-sensitive, as trade deals take time to negotiate and unsettling tariff news is likely to cause noticeable volatility.

Wall Street strategists are growing optimistic about US stocks, with forecasters at Morgan Stanley and Goldman Sachs Group Inc. suggesting resilient economic growth would limit any pullback over the northern hemisphere summer. A slate of strategists including at JPMorgan Chase & Co. and Citigroup Inc. have raised their year-end targets for the S&P 500 in recent days, on bets that the worst shock from the trade war was over.

The S&P 500 equity risk premium — the spread between the earnings yield on stocks and the yield on the 10-year Treasury — is negative, below its long-term average, and likely still too low to support an expectation for strong forward returns. We should note though, a negative or low risk premium isn’t necessarily a predictor of poor forward returns. It was negative for two long stretches in the post-WWII era — from October 1968 to October 1973 and from September 1980 to June 2002. During the first stretch, stocks gained 1.1% annually, but they surged an annualized 10% in the latter.

OVERVIEW OF THE AUSTRALIAN MARKET

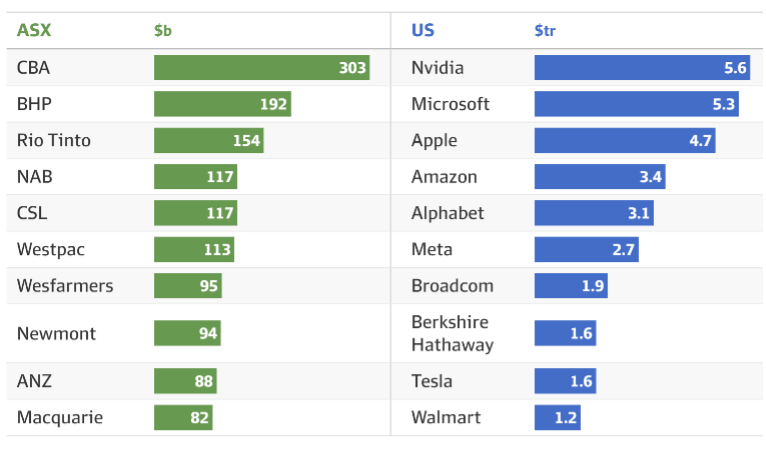

Closed for Monday. However worth reflecting on a topic raised by the AFR over the weekend, and a topic we are all too familiar with. The ASX is dominated by 5 banks. As was noted, it’s a stark contrast to the US sharemarket, where innovative technology companies take out the top seven positions: Nvidia, Microsoft, Apple, Amazon, Alphabet, Meta and Broadcom. Productivity is booming in the tech-savvy US. See Figure 1.

While healthy banks are a positive, bank profits are earned from lending to a relatively unproductive asset class: residential property. The national obsession with loading up on debt to build wealth from property is likely contributing to stagnant productivity, a lack of business dynamism and failure to produce more world-leading businesses.

And there is a bigger problem. A growing pool of either actually constrained or home country biased ‘constrained’ money chasing a decreasing pool of ASX stocks (there’s a lack of ASX equitisation). CBA is the poster child. The valuation metrics on a company with subdued profit growth is staggering. CBA is trading at circa 31 times and well above the 16.5 times long-term average. The tech giants like Nvidia, Microsoft, Meta, Apple and Google have carried international share markets to prosperity by growing their profits at double-digit rates. But as we sit here today, CBA’s 31 times valuation is on par with some of the so-called magnificent seven tech giants, namely Apple and Meta, but below that of Microsoft, Amazon and Nvidia. And all those stocks are both Growth and Defensive – they have massive Moats and throw off huge amounts of cash.

Regarding Figure 2, well, the upside is the ASX has less Beta than the US markets, and that typically translates into a lower drawdown profile.

-

- Figure 1: Top 10 Companies by Mkt Capitalisation

-

- Figure 2: Drawdowns of Select Global Stock Mkts