Summary:

In the bond market, yields edged higher as investors priced in sustained policy caution. The 3-year yield rose to 3.58%, the 5-year to 3.77%, and the 10-year to 4.38%, while the 30-year bond reached 5.01%—implying modestly higher long-term inflation or funding expectations. The yield curve remains positively sloped, having steepened since mid-2023, signalling improving growth prospects and potential support for bank profitability.

On currency markets, the Australian dollar held steady at US$0.6475, showing minimal volatility despite global rate adjustments. The euro and pound strengthened, while most Asian currencies traded narrowly mixed.

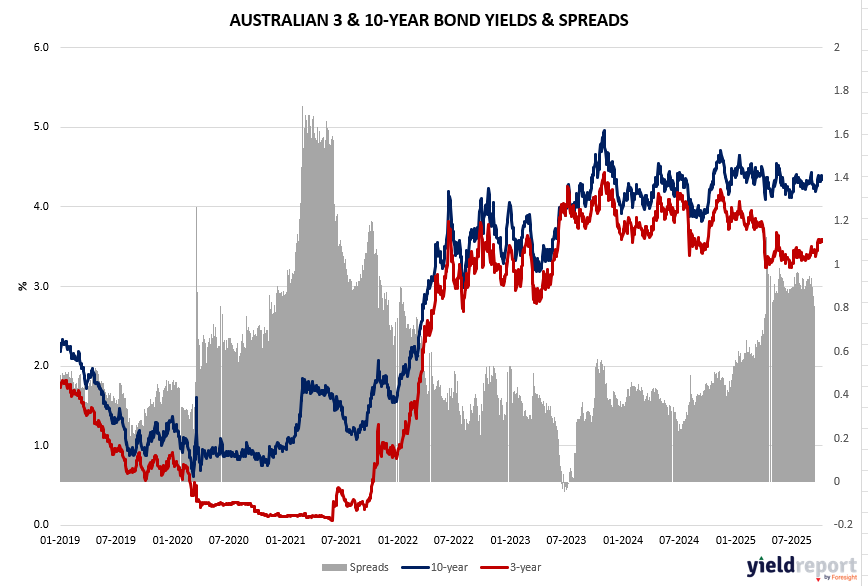

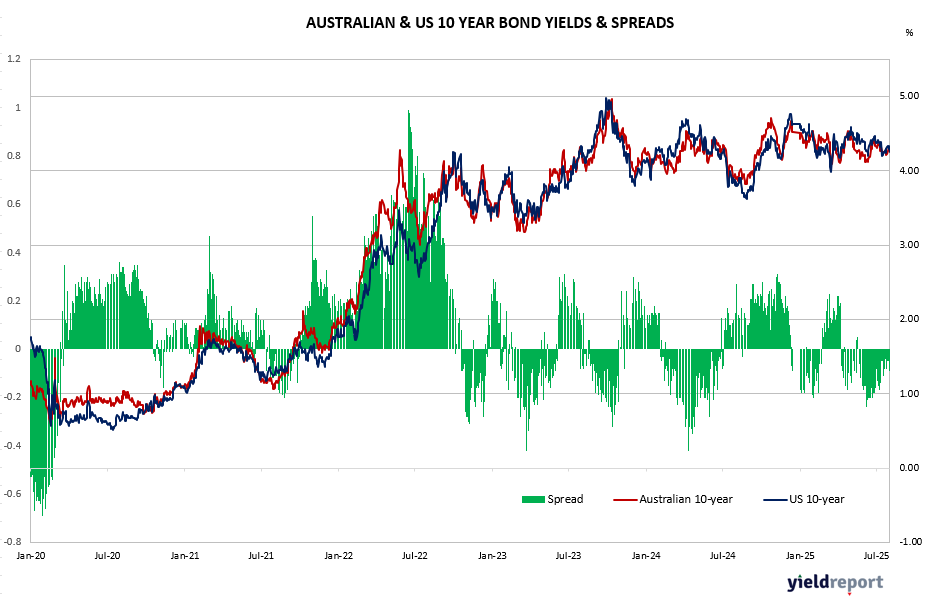

The Australian Bond spreads (3 & 10 years) continue to indicate positive sloping yield curve with significant steepening in the curve occurring from July 2023 (phase 1) and then accelerating from July 2024. The current spread continues to be at cyclical highs although lower than record highs observed in2021. From an investment perspective, steepening yield curves and a rebounding lending environment are likely to boost domestic economic environment and bank profitability. In a similar vein, the spread between the US 2 year bonds and US 10 Year bond has also been steepening since July 2023.

In her address to Parliament, Governor Bullock reaffirmed that inflation is now 2.1% headline and 2.7% trimmed mean, highlighting policy success in restoring price stability. She also underscored structural reforms from the RBA Review, including separate Monetary Policy and Governance Boards, and addressed ongoing efforts in payments modernization, cybersecurity, and digital consumer protection.

Overall, the RBA’s steady stance underscores policy stability amid cautious optimism, balancing inflation control with sustained employment and financial-system resilience.

Figure 1: Aust. 3 yr minus 10 yr Bond Spread

Figure 2: Australian & US Bond Yields

Figure 3: US 10-year minus 2-year Bond Spread