Summary: 10-year bond yield up in Australia; ACGB 10-year spread to US Treasury yield rises to -9bps; 10-year bond yields up in US, most major European markets; $2.8 billion of bonds, notes issued by AOFM.

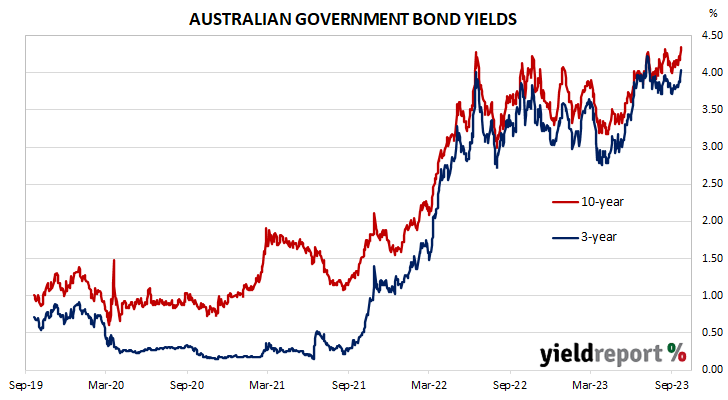

Locally, long-term ACGB yields jumped at the start of the week, pulled back somewhat the next day and then rose each over the remainder of the week. By this point, the 3-year ACGB yields had added 22bps to 4.03%, the 10-year yield had gained 24bps to 4.35% while the 20-year yield finished 22bps higher at 4.66%. The spread between US and Australian 10-year Treasury bond yields increased from -22bps to -9bps.

Over in the US, 10-year bond yields slipped at the start of the week, then rose each day until Friday when they fell back moderately.

The FOMC’s two-day meeting ended on Wednesday with the announcement of an unchanged target range for the federal funds rate.

The Conference Board’s August reading of its Leading Index posted a 0.4% fall the next day, its sixteenth consecutive fall.

S&P Global Market Intelligence’s latest flash reading of its composite index was released at the end of the week, with the index slipping from August’s final reading of 50.2 to 50.1. The manufacturing index rose from 47.9 to 48.9 while the services index lost 0.3 to 50.2. S&P Global’s Siân Jones said, “Although the overall Output Index remained above the 50.0 mark, it was only fractionally so, with a broad stagnation in total activity signalled for the second month running.”

The US Fed’s Nowcast model was also updated. The September quarter GDP growth forecast was lowered from 2.3% to 2.1% annualised, or a 0.5% expansion over the quarter. Its estimate of December quarter’s GDP growth was also reduced, from 2.4% to 2.0% annualised.

By this point, the US 2-year Treasury bond yield had gained 6bps to 5.09% while 10-year and 30-year yields both finished 11bps higher at 4.44% and 4.53% respectively.

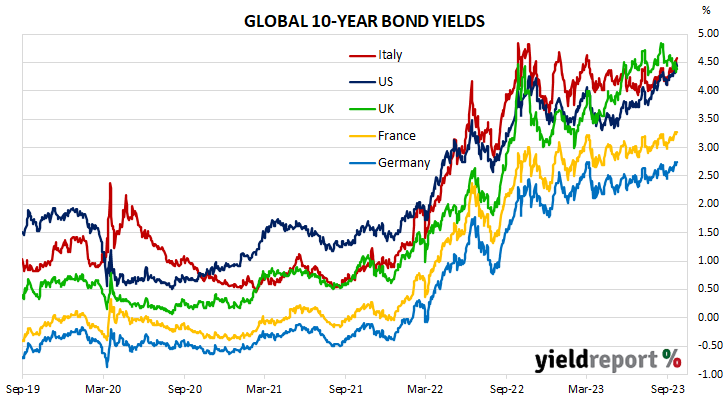

In major euro-zone markets, 10-year bond yields followed a differently path to their US counterpart, generally rising each day with the exception of a moderate fall midweek.

The results of September’s consumer sentiment survey were released on Thursday. The index indicated euro-zone sentiment had deteriorated for a second consecutive month.

The BoE surprised a few that same day when it did not raise its policy rate in a tight vote.

S&P Global Market Intelligence released its September flash PMI figures for the euro-zone some hours before the US figures on Friday. The preliminary reading of the composite index was 47.1, up from August’s final reading of 46.7. Dr. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said he expects “the eurozone to enter a contraction in the third quarter.”

By this point, the German 10-year bund yield had gained 6bps to 2.74% and the French 10-year OAT yield had added 7bps to 3.28%. The Italian 10-year BTP yield increased by 12bps over the week to 4.57% while the British 10-year gilt yield finished 8bps lower at 4.39%.

The AOFM held just the one bond tender during the week; $800 million of June 2035s were priced at a nominal yield of 4.26%. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2023/2024 financial year (not taking into account buy-backs or short-term Treasury note tenders) is $8.3 billion. There are currently $831.55 billion of Treasury bonds and $40.036 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2024 when $35.90 billion worth of bonds are due. There are also $25.00 billion of short-term Treasury notes outstanding after $4.50 billion matured on Friday.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-24 | 2.75 | 35,900 | 4.13 | 0.08 | 0.07 | 4.15 | 4.08 |

| 21-Nov-24 | 0.25 | 41,300 | 4.18 | 0.16 | 0.14 | 4.19 | 4.07 |

| 21-Apr-25 | 3.25 | 41,500 | 4.12 | 0.19 | 0.14 | 4.14 | 3.98 |

| 21-Nov-25 | 0.25 | 39,200 | 4.05 | 0.20 | 0.13 | 4.06 | 3.91 |

| 21-Apr-26 | 4.25 | 39,600 | 4.03 | 0.20 | 0.13 | 4.04 | 3.89 |

| 21-Sep-26 | 0.50 | 37,800 | 4.03 | 0.20 | 0.14 | 4.04 | 3.89 |

| 21-Apr-27 | 4.75 | 36,700 | 4.03 | 0.20 | 0.14 | 4.04 | 3.89 |

| 21-Nov-27 | 2.75 | 31,400 | 4.04 | 0.20 | 0.13 | 4.05 | 3.89 |

| 21-May-28 | 2.25 | 30,900 | 4.05 | 0.21 | 0.12 | 4.05 | 3.90 |

| 21-Nov-28 | 2.75 | 34,800 | 4.07 | 0.21 | 0.11 | 4.07 | 3.92 |

| 21-Apr-29 | 3.25 | 36,600 | 4.10 | 0.21 | 0.10 | 4.10 | 3.94 |

| 21-Nov-29 | 2.75 | 34,700 | 4.13 | 0.21 | 0.10 | 4.13 | 3.98 |

| 21-May-30 | 2.50 | 37,100 | 4.18 | 0.22 | 0.10 | 4.18 | 4.02 |

| 21-Dec-30 | 1.00 | 38,700 | 4.22 | 0.23 | 0.10 | 4.22 | 4.06 |

| 21-Jun-31 | 1.50 | 38,100 | 4.25 | 0.23 | 0.10 | 4.25 | 4.09 |

| 21-Nov-31 | 1.00 | 21,000 | 4.28 | 0.23 | 0.10 | 4.28 | 4.11 |

| 21-May-32 | 1.25 | 39,300 | 4.30 | 0.23 | 0.10 | 4.30 | 4.13 |

| 21-Nov-32 | 1.75 | 29,000 | 4.32 | 0.23 | 0.10 | 4.32 | 4.15 |

| 21-Apr-33 | 4.50 | 25,100 | 4.32 | 0.23 | 0.10 | 4.32 | 4.15 |

| 21-Nov-33 | 3.00 | 22,500 | 4.34 | 0.24 | 0.11 | 4.34 | 4.17 |

| 21-May-34 | 3.75 | 18,800 | 4.35 | 0.23 | 0.10 | 4.35 | 4.18 |

| 21-Dec-34 | 3.50 | 17,000 | 4.37 | 0.23 | 0.10 | 4.37 | 4.20 |

| 21-Jun-35 | 2.75 | 13,050 | 4.40 | 0.24 | 0.10 | 4.40 | 4.23 |

| 21-Apr-37 | 3.75 | 12,300 | 4.48 | 0.23 | 0.09 | 4.48 | 4.31 |

| 21-Jun-39 | 3.25 | 10,300 | 4.56 | 0.21 | 0.09 | 4.56 | 4.40 |

| 21-May-41 | 2.75 | 14,300 | 4.63 | 0.21 | 0.08 | 4.63 | 4.47 |

| 21-Mar-47 | 3.00 | 14,200 | 4.70 | 0.20 | 0.11 | 4.70 | 4.54 |

| 21-Jun-51 | 1.75 | 19,600 | 4.71 | 0.21 | 0.11 | 4.71 | 4.56 |