Summary: 10-year bond yield down in Australia; ACGB 10-year spread to US Treasury yield falls to +16bps; 10-year bond yields down in US, UK, major European markets; $2.85 billion of bonds, notes issued by AOFM.

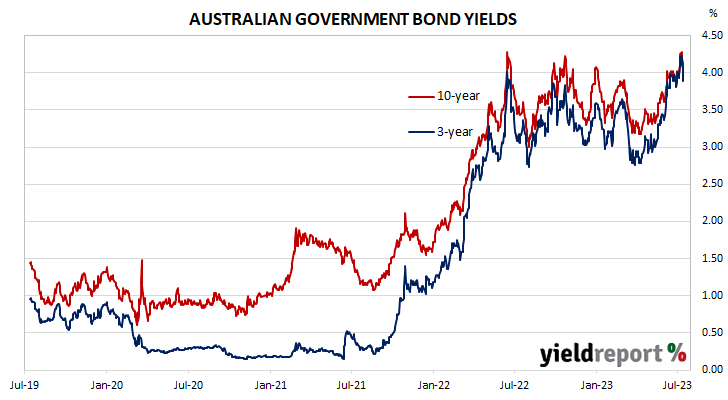

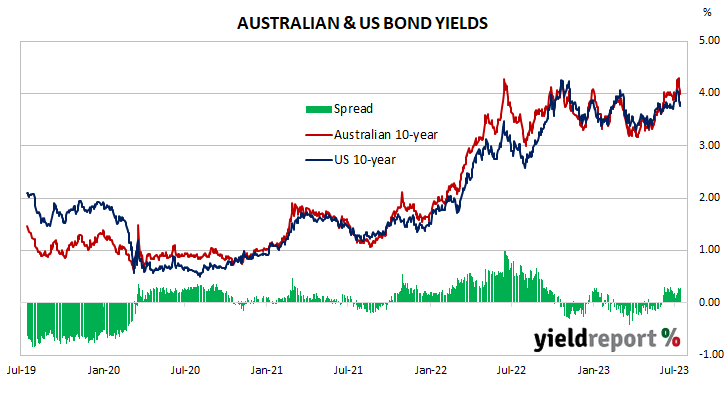

Locally, long-term ACGB yields increased modestly at the start of the week before dropping away over the remainder. By the end of it, the 3-year ACGB yield had shed 34bps to 3.89%, the 10-year yield had lost 27bps to 3.99% while the 20-year yield finished 17bps lower at 4.28%. The spread between US and Australian 10-year Treasury bond yields narrowed from 19bps to 16bps.

Over in the US, 10-year bond yields fell each day until the end of the week when they bounced moderately.

The Atlanta Fed’s Nowcast model was updated at the very start of the week. Its June quarter GDP growth estimate was raised from the previous week’s figure to 2.3% annualised, or a 0.6% expansion over the quarter.

June’s CPI report was released midweek and it produced a 0.2% increase, less than expected. The annual inflation rate slowed to 3.1% and the core inflation rate slowed to 4.9%.

June producer price indices (PPI) were released the next day. The index increased by just 0.1% over the month, less than expected, and the annual growth rate slowed to 0.2%.

At the end of the week, the University of Michigan’s Consumer sentiment index posted a large rise in July. However, it is still substantially below its long-term average.

By this point, the US 2-year Treasury bond yield had shed 21bps to 4.74%, the 10-year yield had lost 24bps to 3.83% while the 30-year yield finished 11bps lower at 3.93%.

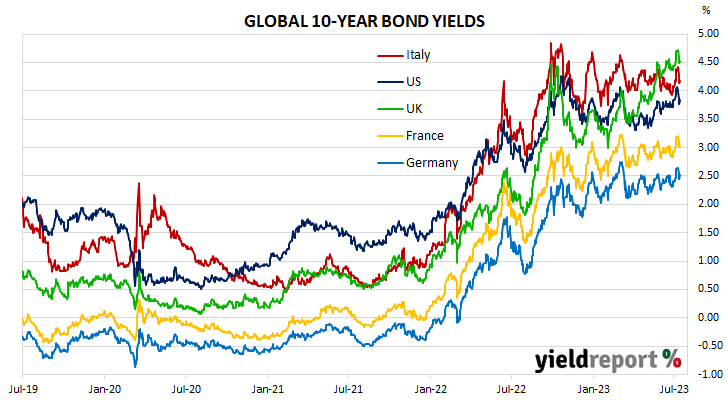

In major euro-zone markets, 10-year bond yields increased modestly for the first two days of the week before falling noticeably over the next two days. Yields then increased again on Friday.

Germany’s ZEW July survey was published on Tuesday. It indicated its Economic Sentiment index had fallen from June’s reading of -8.5 to -14.7. ZEW’s current conditions index also deteriorated, from -56.5 to -59.5. ZEW President Achim Wambach said, ”The industrial sectors are likely to bear the brunt of the anticipated economic downturn…”

The euro-zone’s May industrial production figures were released a couple of days later. Output expanded by 0.2% over the month, slightly less than expected.

By the end of the week, the German 10-year bond yield had lost 12bps to 2.51% and the French 10-year OAT yield had shed 15bps to 3.03%. The Italian 10-year BTP yield fell 18bps over the week to 4.17% while the British 10-year gilt yield finished 17bps lower at 4.52%.

The AOFM held one vanilla bond tender and one index-linked bond (ILB) tender this week; $700 million of May 2028s were priced at a yield of 4.07% and $150 million of November 2032s were priced at a real yield of 1.79%. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2023/2024 financial year (not taking into account buy-backs or short-term Treasury note tenders) is $1.55 billion. There are currently $825.25 billion of Treasury bonds and $39.586 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2024 when $35.90 billion worth of bonds are due. There are also $28.00 billion of short-term Treasury notes outstanding.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-24 | 2.75 | 35,900 | 4.22 | -0.23 | 0.00 | 4.41 | 4.22 |

| 21-Nov-24 | 0.25 | 41,300 | 4.16 | -0.30 | 0.05 | 4.43 | 4.16 |

| 21-Apr-25 | 3.25 | 41,500 | 4.06 | -0.35 | 0.06 | 4.38 | 4.06 |

| 21-Nov-25 | 0.25 | 39,200 | 3.97 | -0.34 | 0.09 | 4.28 | 3.97 |

| 21-Apr-26 | 4.25 | 39,600 | 3.92 | -0.33 | 0.10 | 4.23 | 3.92 |

| 21-Sep-26 | 0.50 | 37,800 | 3.90 | -0.33 | 0.09 | 4.21 | 3.90 |

| 21-Apr-27 | 4.75 | 36,700 | 3.88 | -0.33 | 0.08 | 4.19 | 3.88 |

| 21-Nov-27 | 2.75 | 31,400 | 3.87 | -0.32 | 0.07 | 4.18 | 3.87 |

| 21-May-28 | 2.25 | 30,900 | 3.87 | -0.32 | 0.07 | 4.18 | 3.87 |

| 21-Nov-28 | 2.75 | 34,100 | 3.87 | -0.31 | 0.07 | 4.19 | 3.87 |

| 21-Apr-29 | 3.25 | 36,600 | 3.89 | -0.32 | 0.06 | 4.21 | 3.89 |

| 21-Nov-29 | 2.75 | 34,700 | 3.90 | -0.31 | 0.06 | 4.22 | 3.90 |

| 21-May-30 | 2.50 | 37,100 | 3.92 | -0.30 | 0.05 | 4.24 | 3.92 |

| 21-Dec-30 | 1.00 | 38,700 | 3.94 | -0.29 | 0.05 | 4.25 | 3.94 |

| 21-Jun-31 | 1.50 | 38,100 | 3.96 | -0.28 | 0.04 | 4.26 | 3.96 |

| 21-Nov-31 | 1.00 | 21,000 | 3.97 | -0.27 | 0.04 | 4.27 | 3.97 |

| 21-May-32 | 1.25 | 39,300 | 3.98 | -0.27 | 0.04 | 4.28 | 3.98 |

| 21-Nov-32 | 1.75 | 29,000 | 3.99 | -0.26 | 0.04 | 4.28 | 3.99 |

| 21-Apr-33 | 4.50 | 24,400 | 3.99 | -0.26 | 0.04 | 4.28 | 3.99 |

| 21-Nov-33 | 3.00 | 21,800 | 3.99 | -0.26 | 0.03 | 4.29 | 3.99 |

| 21-May-34 | 3.75 | 18,100 | 4.00 | -0.26 | 0.02 | 4.29 | 4.00 |

| 21-Dec-34 | 3.50 | 15,500 | 4.02 | -0.27 | 0.01 | 4.31 | 4.02 |

| 21-Jun-35 | 2.75 | 11,550 | 4.04 | -0.26 | 0.01 | 4.33 | 4.04 |

| 21-Apr-37 | 3.75 | 12,300 | 4.12 | -0.25 | 0.00 | 4.40 | 4.12 |

| 21-Jun-39 | 3.25 | 10,300 | 4.22 | -0.21 | 0.00 | 4.46 | 4.22 |

| 21-May-41 | 2.75 | 13,800 | 4.27 | -0.19 | 0.00 | 4.50 | 4.27 |

| 21-Mar-47 | 3.00 | 14,200 | 4.30 | -0.19 | -0.01 | 4.51 | 4.30 |

| 21-Jun-51 | 1.75 | 19,600 | 4.29 | -0.19 | -0.02 | 4.50 | 4.29 |