Summary: 10-year bond yields steady in Australia; ACGB 10-year spread to US Treasury yield falls from +1bp to -12bps; 10-year bond yields up in US, major European markets; $4 billion of bonds, notes issued by AOFM.

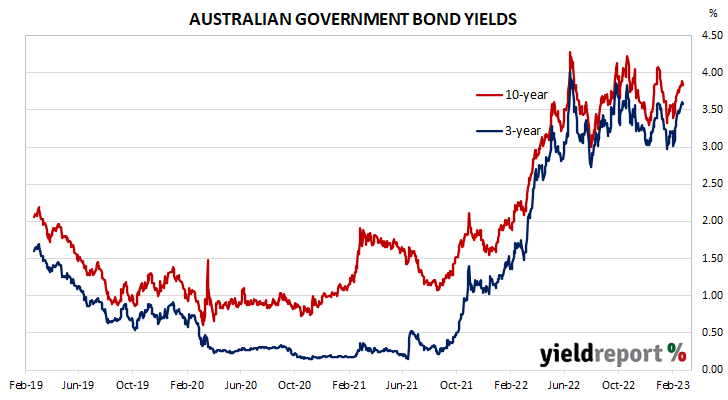

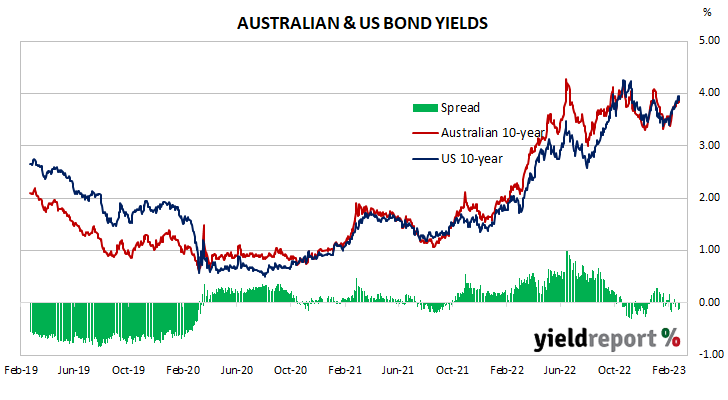

Locally, long-term ACGB yields essentially oscillated through the week. By the end of the week, the 3-year ACGB yield had gained 7bps to 3.58%, the 10-year yield had returned to its starting point at 3.83% while the 20-year yield finished 3bps lower at 4.16%. The spread between US and Australian 10-year Treasury bond yields “tightened” from +1bp to -12bps.

Over in the US, 10-year bond yields started its shortened week with a big jump. This was followed by couple of days of falls and a sizable rise at the end of the week.

S&P Global Market Intelligence’s latest flash reading of its composite index was released on Tuesday (US time), with the index rising from January’s final reading of 46.8 to 50.2. The manufacturing index increased from 46.9 to 47.8 and the services index added 3.7 points to 50.5. S&P Global’s Chris Williamson said, “Despite headwinds from higher interest rates and the cost of living squeeze, the business mood has brightened amid signs that inflation has peaked and recession risks have faded”

The minutes from the FOMC’s last meeting in February were released midweek. They indicated the pace of increases would slow but increases would still be appropriate.

At the end of the week, the latest report on personal consumption expenditures indicated core PCE price inflation had increased by 0.6% in January and by 4.7% on annual basis, up from 4.6% in December.

The Atlanta Fed’s Nowcast model was also updated. The March quarter GDP growth estimate was raised to 2.7% annualised, or a 0.7% expansion over the quarter.

By this point, the US 2-year Treasury bond yield had gained 17bps to 4.80%, the 10-year yield had added 13bps to 3.95% while the 30-year yield finished 6bps higher at 3.93%.

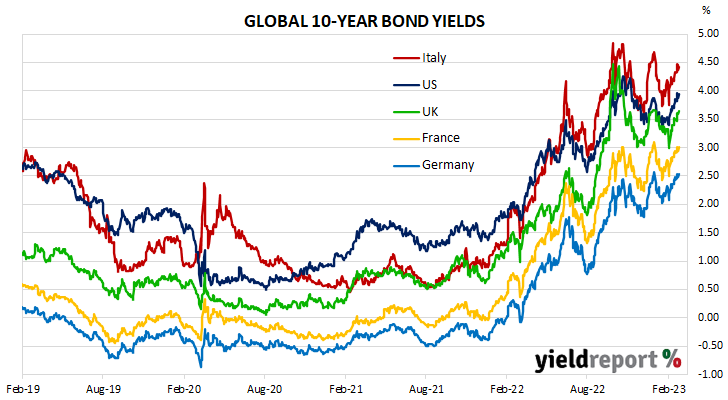

In major euro-zone markets, 10-year bond yields followed a similar path to their US counterpart.

The results of February’s consumer sentiment survey were released at the start of the week and they indicated euro-zone sentiment had improved for a fifth consecutive month. However, the index is still well below the long-term average.

S&P Global Market Intelligence released its February flash PMI figures for the euro-zone some hours before the US figures on Tuesday. The preliminary reading of the composite index was 52.3, up from January’s final reading of 50.3. S&P Global’s Chris Williamson said, “Business activity across the eurozone grew much faster than expected in February, with growth hitting a nine-month high thanks to resurgent service sector activity and a recovering manufacturing economy.”

By the end of the week, German and French 10-year bond yields had both gained 10bps to 2.54% and 3.01% respectively. The Italian 10-year BTP yield increased by 12bps over the week to 4.43% while the British 10-year gilt yield finished 14bps higher at 3.65%.

The AOFM held two vanilla bond tenders during the week. $900 million of May 2034s and $600 million of November 20269 were priced at yields of 3.97% and 3.76% respectively. There were also three Treasury note tenders which raised a total of $2.5 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $52.75 billion. There are currently $830.85 billion of Treasury bonds and $38.386 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2023 when $34.20 billion worth of bonds are due. There are also $27.250 billion of short-term Treasury notes currently outstanding after $4 billion matured on Friday.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-23 | 5.5 | 34,200 | 3.52 | 0.02 | 0.36 | 3.53 | 3.50 |

| 21-Apr-24 | 2.75 | 35,900 | 3.73 | 0.10 | 0.70 | 3.76 | 3.68 |

| 21-Nov-24 | 0.25 | 41,300 | 3.61 | 0.06 | 0.63 | 3.64 | 3.59 |

| 21-Apr-25 | 3.25 | 41,500 | 3.56 | 0.07 | 0.63 | 3.59 | 3.53 |

| 21-Nov-25 | 0.25 | 38,700 | 3.55 | 0.08 | 0.58 | 3.58 | 3.52 |

| 21-Apr-26 | 4.25 | 38,600 | 3.56 | 0.07 | 0.57 | 3.59 | 3.53 |

| 21-Sep-26 | 0.5 | 37,300 | 3.60 | 0.07 | 0.57 | 3.63 | 3.57 |

| 21-Apr-27 | 4.75 | 36,700 | 3.61 | 0.07 | 0.57 | 3.64 | 3.58 |

| 21-Nov-27 | 2.75 | 31,400 | 3.62 | 0.05 | 0.55 | 3.66 | 3.60 |

| 21-May-28 | 2.25 | 30,200 | 3.64 | 0.05 | 0.54 | 3.68 | 3.61 |

| 21-Nov-28 | 2.75 | 34,100 | 3.66 | 0.04 | 0.52 | 3.70 | 3.64 |

| 21-Apr-29 | 3.25 | 35,000 | 3.68 | 0.04 | 0.51 | 3.73 | 3.66 |

| 21-Nov-29 | 2.75 | 34,700 | 3.72 | 0.03 | 0.49 | 3.77 | 3.69 |

| 21-May-30 | 2.5 | 37,100 | 3.74 | 0.03 | 0.48 | 3.79 | 3.72 |

| 21-Dec-30 | 1 | 38,700 | 3.77 | 0.02 | 0.46 | 3.83 | 3.75 |

| 21-Jun-31 | 1.5 | 38,100 | 3.79 | 0.01 | 0.45 | 3.85 | 3.77 |

| 21-Nov-31 | 1 | 21,000 | 3.81 | 0.01 | 0.44 | 3.87 | 3.79 |

| 21-May-32 | 1.25 | 39,300 | 3.81 | 0.01 | 0.43 | 3.87 | 3.80 |

| 21-Nov-32 | 1.75 | 27,800 | 3.83 | 0.01 | 0.43 | 3.89 | 3.81 |

| 21-Apr-33 | 4.5 | 23,600 | 3.82 | 0.01 | 0.43 | 3.88 | 3.81 |

| 21-Nov-33 | 3 | 20,400 | 3.85 | 0.00 | 0.43 | 3.92 | 3.84 |

| 21-May-34 | 3.75 | 15,600 | 3.87 | 0.00 | 3.87 | 3.94 | 3.86 |

| 21-Jun-35 | 2.75 | 9,550 | 3.96 | 0.00 | 0.42 | 4.02 | 3.95 |

| 21-Apr-37 | 3.75 | 12,300 | 4.04 | 0.00 | 0.40 | 4.10 | 4.03 |

| 21-Jun-39 | 3.25 | 10,300 | 4.11 | -0.02 | 0.38 | 4.17 | 4.11 |

| 21-May-41 | 2.75 | 13,800 | 4.16 | -0.02 | 0.36 | 4.22 | 4.16 |

| 21-Mar-47 | 3 | 13,900 | 4.19 | -0.03 | 0.34 | 4.25 | 4.19 |

| 21-Jun-51 | 1.75 | 19,000 | 4.14 | -0.03 | 0.33 | 4.20 | 4.14 |