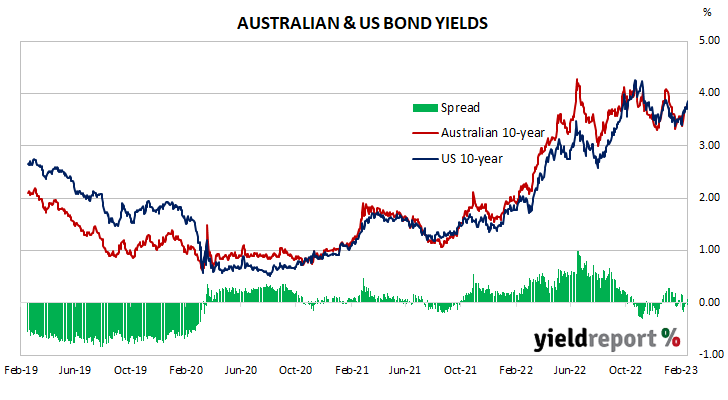

Summary: Bond yields higher in Australia; ACGB 10-year spread to US Treasury yield rises from -2bps to +1bp; 10-year bond yields up in US, major European markets; $3.65 billion of bonds, notes issued by AOFM.

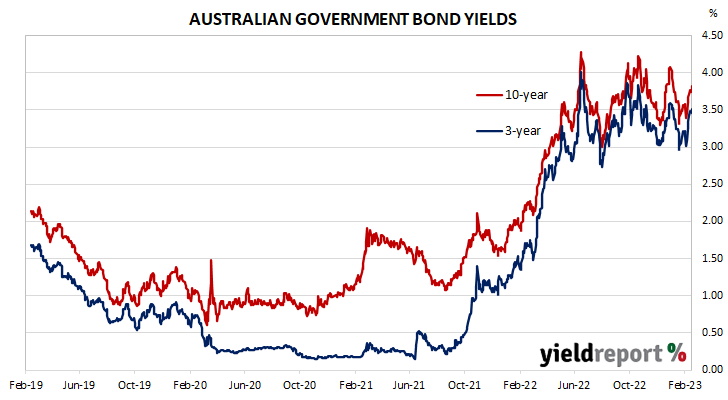

Locally, long-term ACGB yields rose through most of the week, with only a modest decline on Tuesday. By the end of the week, the 3-year ACGB yield had added 8bps to 3.51% while 10-year and 20-year yields both finished 11bps higher at 3.83% and 4.19% respectively. The spread between US and Australian 10-year Treasury bond yields “widened” from -2bps to +1bp.

Over in the US, 10-year bond yields started its week with a moderate fall. This was followed by several days of rises until the end of the week when yields fell moderately again.

January’s CPI report was released on Tuesday night (AEDT) and it produced a 0.5% increase, in line with expectations. The annual inflation rate slowed from 6.4% to 6.3% and the core inflation rate slowed from 5.7% to 5.5%.

Industrial production numbers and retail sales figures for January were both released the next day.

Industrial production remained steady, less than the expected 0.5% increase. This latest reading implied an annual GDP growth rate of 2.2%.

The retail sales report indicated total sales had jumped by 3.0% over the month, more than the expected 2.0% increase. Vehicle sales and takeaway food and beverage sales both had noticeable effects on the overall growth figure.

January producer price indices were released Thursday. Producer prices increased by 0.7% over the month and by 6.0% over the year.

The Atlanta Fed’s Nowcast model was also updated. The March quarter GDP growth estimate was raised to 2.5% annualised, or a 0.6% expansion over the quarter.

The Conference Board’s January reading of its Leading Index came out at the end of the week. The 0.3% fall met expectations.

By this point, the US 2-year Treasury bond yield had gained 12bps to 4.63%, the 10-year yield had added 8bps to 3.80% while the 30-year yield finished 5bps higher at 3.87%.

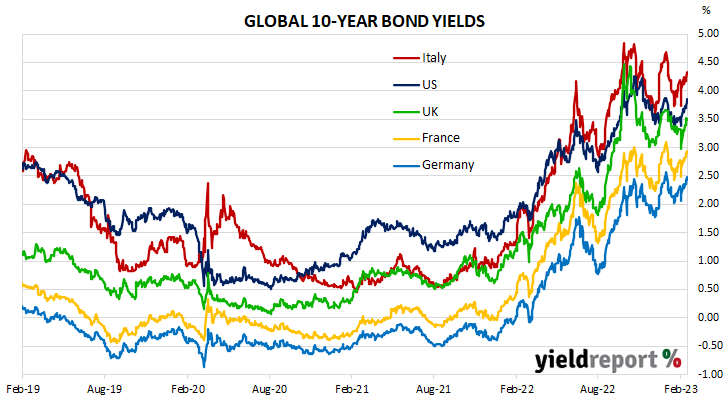

In major euro-zone markets, 10-year bond yields again followed a broadly similar path to their US counterpart except yields generally remained stable at the start of the week.

There was little of note in terms of economic reports except for the latest industrial production figures released midweek. Output contracted by 1.1% in December, slightly better than expected but in contrast to November’s 1.4% rise.

By the end of the week, German and French 10-year bond yields had both gained 8bps to 2.44% and 2.91% respectively. The Italian 10-year BTP yield increased by 10bps over the week to 4.31% while the British 10-year gilt yield finished 12bps higher at 3.51%.

The AOFM held three vanilla bond tenders during the week as well as an index-linked bond (ILB) tender. $300 million of June 2051s, $700 million of April 2033s and $500 million of April 2026s were priced at yields of 4.18%, 3.81% and 3.46% respectively while $150 million of September 2030 ILBs were priced with a real yield of 1.01%. There were also three Treasury note tenders which raised a total of $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $51.25 billion. There are currently $829.35 billion of Treasury bonds and $38.386 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2023 when $34.20 billion worth of bonds are due. There are also $29.00 billion of short-term Treasury notes currently outstanding.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-23 | 5.5 | 34,200 | 3.51 | 0.00 | 0.29 | 3.53 | 3.51 |

| 21-Apr-24 | 2.75 | 35,900 | 3.63 | 0.06 | 0.44 | 3.63 | 3.59 |

| 21-Nov-24 | 0.25 | 41,300 | 3.55 | 0.10 | 0.38 | 3.55 | 3.49 |

| 21-Apr-25 | 3.25 | 41,500 | 3.49 | 0.09 | 0.34 | 3.49 | 3.43 |

| 21-Nov-25 | 0.25 | 38,700 | 3.48 | 0.08 | 0.29 | 3.48 | 3.43 |

| 21-Apr-26 | 4.25 | 38,600 | 3.49 | 0.08 | 0.28 | 3.49 | 3.44 |

| 21-Sep-26 | 0.5 | 37,300 | 3.52 | 0.08 | 0.27 | 3.52 | 3.47 |

| 21-Apr-27 | 4.75 | 36,700 | 3.54 | 0.08 | 0.27 | 3.54 | 3.49 |

| 21-Nov-27 | 2.75 | 31,400 | 3.57 | 0.09 | 0.26 | 3.57 | 3.52 |

| 21-May-28 | 2.25 | 30,200 | 3.59 | 0.09 | 0.25 | 3.59 | 3.54 |

| 21-Nov-28 | 2.75 | 34,100 | 3.61 | 0.09 | 0.24 | 3.61 | 3.56 |

| 21-Apr-29 | 3.25 | 35,000 | 3.64 | 0.09 | 0.24 | 3.64 | 3.58 |

| 21-Nov-29 | 2.75 | 34,100 | 3.69 | 0.10 | 0.24 | 3.69 | 3.62 |

| 21-May-30 | 2.5 | 37,100 | 3.72 | 0.10 | 0.23 | 3.72 | 3.64 |

| 21-Dec-30 | 1 | 38,700 | 3.76 | 0.10 | 0.22 | 3.76 | 3.68 |

| 21-Jun-31 | 1.5 | 38,100 | 3.78 | 0.11 | 0.23 | 3.78 | 3.70 |

| 21-Nov-31 | 1 | 21,000 | 3.80 | 0.11 | 0.23 | 3.80 | 3.72 |

| 21-May-32 | 1.25 | 39,300 | 3.81 | 0.11 | 0.23 | 3.81 | 3.73 |

| 21-Nov-32 | 1.75 | 27,800 | 3.82 | 0.11 | 0.23 | 3.82 | 3.74 |

| 21-Apr-33 | 4.5 | 23,600 | 3.82 | 0.11 | 0.23 | 3.82 | 3.74 |

| 21-Nov-33 | 3 | 20,400 | 3.85 | 0.11 | 0.22 | 3.85 | 3.77 |

| 21-May-34 | 3.75 | 14,700 | 3.87 | 0.11 | 3.87 | 3.87 | 3.79 |

| 21-Jun-35 | 2.75 | 9,550 | 3.96 | 0.11 | 0.22 | 3.96 | 3.87 |

| 21-Apr-37 | 3.75 | 12,300 | 4.04 | 0.10 | 0.21 | 4.04 | 3.95 |

| 21-Jun-39 | 3.25 | 10,300 | 4.13 | 0.10 | 0.21 | 4.13 | 4.03 |

| 21-May-41 | 2.75 | 13,800 | 4.18 | 0.11 | 0.21 | 4.18 | 4.07 |

| 21-Mar-47 | 3 | 13,900 | 4.22 | 0.11 | 0.23 | 4.22 | 4.10 |

| 21-Jun-51 | 1.75 | 19,000 | 4.18 | 0.11 | 0.25 | 4.18 | 4.06 |