Summary: Bond yields higher in Australia; ACGB 10-year spread to US Treasury yield rises from -13bps to -2bps; 10-year bond yields up in US, major European markets; $3.5 billion of bonds, notes issued by AOFM.

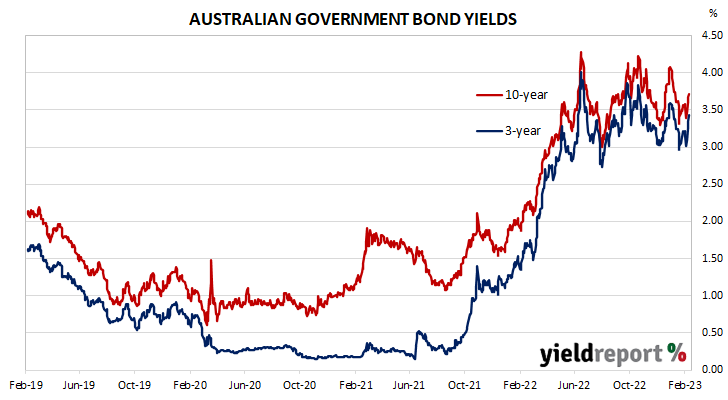

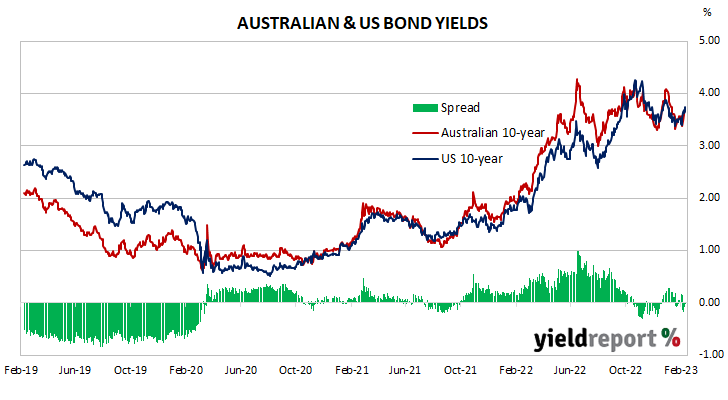

Locally, long-term ACGB yields rose consistently throughout the week, with a large increase on Tuesday following sizable offshore increases on Monday night. By the end of the week, the 3-year ACGB yield had gained 42bps to 3.43%, the 10-year yield had added 33bps to 3.72% while the 20-year yield finished 26bps higher at 4.08%. The spread between US and Australian 10-year Treasury bond yields “widened” from -13bps to -2bps.

Over in the US, 10-year bond yields started its week with a large rise which was followed by more rises over the week with the exception of a moderate midweek pullback.

The Atlanta Fed’s Nowcast model was updated on Wednesday. The March quarter GDP growth estimate was raised to 2.2% annualised, or a 0.5% expansion over the quarter.

One of the two major measures of US consumer sentiment, the University of Michigan’s Consumer sentiment index was published at the end of the week. The index increased for a third consecutive month but remains well below its long-term average.

By this point, the US 2-year Treasury bond yield had gained 21bps to 4.51%, the 10-year yield had added 22bps to 3.72% while the 30-year yield finished 20bps higher at 3.82%.

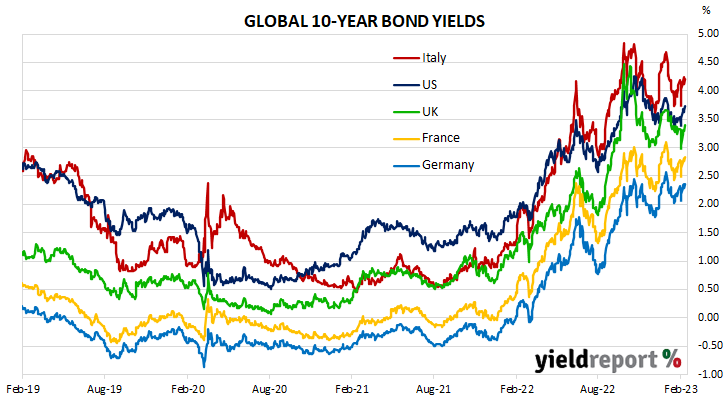

In major euro-zone markets, 10-year bond yields again followed a broadly similar path to their US counterpart.

By the end of the week, the German 10-year bund yield had added 17bps to 2.36% while the French 10-year OAT yield had gained 19bps to 2.83%. The Italian 10-year BTP yield increased by 18bps over the week to 4.21% while the British 10-year gilt yield finished 34bps higher at 3.39%.

The AOFM held two bond tenders during the week. $1 billion of November 2033s and $500 million of May 2028s were priced at yields of 3.69% and 3.52% respectively. There were also three Treasury note tenders which raised a total of $2 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $49.60 billion. There are currently $827.85 billion of Treasury bonds and $38.236 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2023 when $34.20 billion worth of bonds are due. There are also $27.00 billion of short-term Treasury notes currently outstanding after $6.50 billion matured on Friday.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-23 | 5.50 | 34,200 | 3.51 | 0.24 | 0.27 | 3.51 | 3.33 |

| 21-Apr-24 | 2.75 | 35,900 | 3.57 | 0.39 | 0.22 | 3.57 | 3.26 |

| 21-Nov-24 | 0.25 | 41,300 | 3.45 | 0.38 | 0.08 | 3.45 | 3.13 |

| 21-Apr-25 | 3.25 | 41,500 | 3.39 | 0.41 | 0.00 | 3.39 | 3.07 |

| 21-Nov-25 | 0.25 | 38,700 | 3.39 | 0.41 | -0.05 | 3.39 | 3.07 |

| 21-Apr-26 | 4.25 | 38,100 | 3.42 | 0.41 | -0.06 | 3.42 | 3.10 |

| 21-Sep-26 | 0.50 | 37,300 | 3.45 | 0.42 | -0.08 | 3.45 | 3.12 |

| 21-Apr-27 | 4.75 | 36,700 | 3.47 | 0.41 | -0.08 | 3.47 | 3.14 |

| 21-Nov-27 | 2.75 | 31,400 | 3.49 | 0.40 | -0.09 | 3.49 | 3.17 |

| 21-May-28 | 2.25 | 30,200 | 3.50 | 0.39 | -0.10 | 3.50 | 3.20 |

| 21-Nov-28 | 2.75 | 34,100 | 3.52 | 0.38 | -0.11 | 3.52 | 3.23 |

| 21-Apr-29 | 3.25 | 35,000 | 3.55 | 0.38 | -0.11 | 3.55 | 3.27 |

| 21-Nov-29 | 2.75 | 34,100 | 3.59 | 0.37 | -0.11 | 3.59 | 3.31 |

| 21-May-30 | 2.50 | 37,100 | 3.61 | 0.36 | -0.12 | 3.61 | 3.34 |

| 21-Dec-30 | 1.00 | 38,700 | 3.65 | 0.34 | -0.12 | 3.65 | 3.39 |

| 21-Jun-31 | 1.50 | 38,100 | 3.67 | 0.34 | -0.11 | 3.67 | 3.42 |

| 21-Nov-31 | 1.00 | 21,000 | 3.69 | 0.33 | -0.11 | 3.69 | 3.44 |

| 21-May-32 | 1.25 | 39,300 | 3.70 | 0.33 | -0.12 | 3.70 | 3.45 |

| 21-Nov-32 | 1.75 | 27,800 | 3.71 | 0.33 | -0.11 | 3.71 | 3.46 |

| 21-Apr-33 | 4.50 | 22,900 | 3.71 | 0.33 | -0.11 | 3.71 | 3.46 |

| 21-Nov-33 | 3.00 | 20,400 | 3.74 | 0.33 | -0.12 | 3.74 | 3.49 |

| 21-May-34 | 3.75 | 14,700 | 3.76 | 0.32 | -0.12 | 3.76 | 3.51 |

| 21-Jun-35 | 2.75 | 9,550 | 3.85 | 0.32 | -0.13 | 3.85 | 3.60 |

| 21-Apr-37 | 3.75 | 12,300 | 3.94 | 0.30 | -0.11 | 3.94 | 3.70 |

| 21-Jun-39 | 3.25 | 10,300 | 4.03 | 0.28 | -0.09 | 4.03 | 3.80 |

| 21-May-41 | 2.75 | 13,800 | 4.08 | 0.26 | -0.08 | 4.08 | 3.87 |

| 21-Mar-47 | 3.00 | 13,900 | 4.11 | 0.26 | -0.05 | 4.11 | 3.98 |

| 21-Jun-51 | 1.75 | 18,700 | 4.07 | 0.25 | -0.04 | 4.07 | 3.86 |