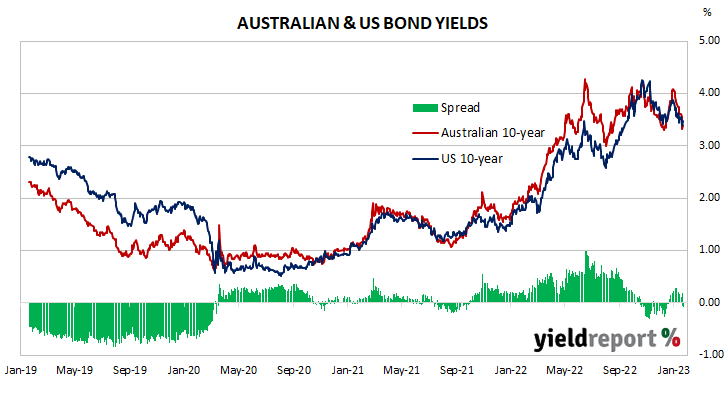

Summary: Bond yields lower in Australia; ACGB 10-year spread to US Treasury yield falls from 11bps to -8bps; 10-year bond yields down in US, up or steady in major European markets; AOFM issues $3 billion worth of notes.

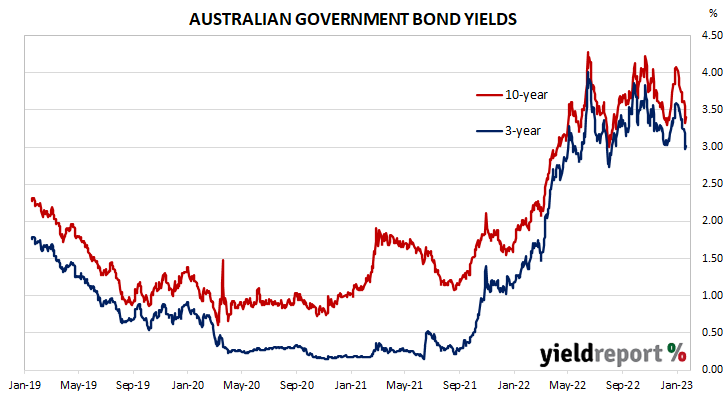

Locally, long-term ACGB yields fell in net terms over the week, aided by especially heavy falls on Thursday. By the end of the week, the 3-year ACGB yield had shed 23bps to 3.01%, the 10-year yield had lost 21bps to 3.40% while the 20-year yield finished 16bps lower at 3.81%. The spread between US and Australian 10-year Treasury bond yields tightened from +11bps to -8bps.

Over in the US, 10-year bond yields started its shortened week with a moderate rise which was immediately followed by a heavy fall midweek. Yields increased over the remainder of the week.

The first notable economic reports were not released until Wednesday when three reports came out.

December producer prices decreased by 0.5% over the month, a greater fall than that which had been generally expected. Prices rose by 6.2% over the year, down from 7.3% in the previous month.

December’s retail sales report indicated total sales fell by 1.1% over the month but still managed to be up 6.0% for the year. Lower fuel sales had the largest single effect on the total.

Industrial production numbers for December indicated US domestic output contracted by 0.7%, a larger contraction than expected. This latest reading implied an annual GDP growth rate of 2.6%.

The Atlanta Fed’s Nowcast model was updated on Friday. The December quarter GDP growth estimate was lowered to 3.5% annualised, or a 0.9% expansion over the quarter.

By this point, the US 2-year Treasury bond yield had lost 3bps to 4.19%, the 10-year yield had shed 2bps to 3.48% while the 30-year yield finished 4bps higher at 3.65%.

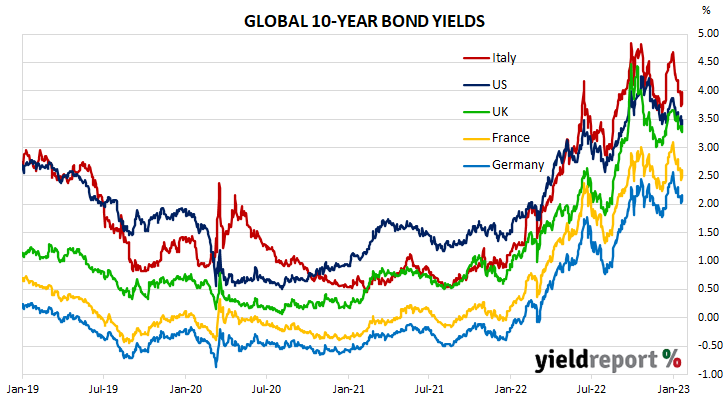

In major euro-zone markets, 10-year bond yields followed a vaguely similar path to their US counterpart.

On Tuesday night (AEDT), Germany’s ZEW January survey indicated its Economic Sentiment index had increased from December’s reading of -23.3 to +16.7. This is the first positive reading since February 2022. ZEW’s current conditions index rose modestly, from -61.4 to -58.6. “For the first time since February 2022…the indicator points to a noticeable improvement in the economic situation over the next six months.”

By the end of the week, the German 10-year bund yield had added 3bps to 2.17% while the French 10-year OAT yield had returned to its starting point at 2.61%. The Italian 10-year BTP yield slipped 1bp over the week to 3.97% while the British 10-year gilt yield finished unchanged at 3.37%.

The AOFM did not hold any bond tenders during the week. However, there were three Treasury note tenders which raised a total of $3.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $46.60 billion. There are currently $824.85 billion of Treasury bonds and $38.236 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2023 when $34.20 billion worth of bonds are due. There are also $34.50 billion of short-term Treasury notes currently outstanding.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-23 | 5.50 | 34,200 | 3.17 | -0.06 | 0.02 | 3.24 | 3.16 |

| 21-Apr-24 | 2.75 | 35,900 | 3.03 | -0.17 | -0.13 | 3.21 | 2.99 |

| 21-Nov-24 | 0.25 | 41,300 | 2.98 | -0.19 | -0.16 | 3.17 | 2.93 |

| 21-Apr-25 | 3.25 | 41,500 | 2.93 | -0.22 | -0.19 | 3.15 | 2.88 |

| 21-Nov-25 | 0.25 | 38,700 | 2.98 | -0.21 | -0.16 | 3.19 | 2.94 |

| 21-Apr-26 | 4.25 | 38,100 | 3.00 | -0.22 | -0.17 | 3.22 | 2.96 |

| 21-Sep-26 | 0.50 | 37,300 | 3.03 | -0.23 | -0.16 | 3.26 | 2.99 |

| 21-Apr-27 | 4.75 | 36,700 | 3.05 | -0.23 | -0.16 | 3.27 | 3.00 |

| 21-Nov-27 | 2.75 | 31,400 | 3.08 | -0.24 | -0.15 | 3.31 | 3.03 |

| 21-May-28 | 2.25 | 29,700 | 3.10 | -0.24 | -0.15 | 3.34 | 3.06 |

| 21-Nov-28 | 2.75 | 34,100 | 3.14 | -0.23 | -0.14 | 3.37 | 3.09 |

| 21-Apr-29 | 3.25 | 34,500 | 3.18 | -0.23 | -0.13 | 3.40 | 3.12 |

| 21-Nov-29 | 2.75 | 34,100 | 3.23 | -0.22 | -0.12 | 3.45 | 3.16 |

| 21-May-30 | 2.50 | 37,100 | 3.26 | -0.23 | -0.11 | 3.49 | 3.20 |

| 21-Dec-30 | 1.00 | 38,700 | 3.31 | -0.22 | -0.09 | 3.54 | 3.25 |

| 21-Jun-31 | 1.50 | 38,100 | 3.35 | -0.21 | -0.08 | 3.56 | 3.27 |

| 21-Nov-31 | 1.00 | 21,000 | 3.37 | -0.20 | -0.07 | 3.58 | 3.30 |

| 21-May-32 | 1.25 | 39,300 | 3.38 | -0.20 | -0.06 | 3.59 | 3.31 |

| 21-Nov-32 | 1.75 | 27,800 | 3.39 | -0.20 | -0.06 | 3.60 | 3.32 |

| 21-Apr-33 | 4.50 | 22,900 | 3.39 | -0.20 | -0.06 | 3.60 | 3.32 |

| 21-Nov-33 | 3.00 | 19,400 | 3.43 | -0.20 | -0.06 | 3.64 | 3.35 |

| 21-Jun-35 | 2.75 | 9,550 | 3.53 | -0.21 | -0.07 | 3.75 | 3.46 |

| 21-Apr-37 | 3.75 | 12,300 | 3.64 | -0.19 | -0.05 | 3.84 | 3.56 |

| 21-Jun-39 | 3.25 | 10,300 | 3.74 | -0.18 | -0.02 | 3.93 | 3.66 |

| 21-May-41 | 2.75 | 13,500 | 3.81 | -0.17 | 0.00 | 3.99 | 3.73 |

| 21-Mar-47 | 3.00 | 13,900 | 3.85 | -0.14 | 0.02 | 4.01 | 3.78 |

| 21-Jun-51 | 1.75 | 18,700 | 3.81 | -0.12 | 0.03 | 3.95 | 3.74 |